Why Meta’s Q4 2025 Results Matter

Meta Platforms enters the Q4 2025 earnings season as one of the most profitable yet fastest-growing technology companies in the world. Following deep cost restructuring in previous years and a clear return to strong revenue growth, the company is once again in the spotlight for investors. Today’s results will test whether Meta can maintain exceptionally high profitability while significantly ramping up investments related to artificial intelligence.

The market expects not only solid numbers but, more importantly, confirmation that the company’s aggressive investment strategy in AI and computing infrastructure strengthens its long-term potential without undermining its ability to generate robust cash flows.

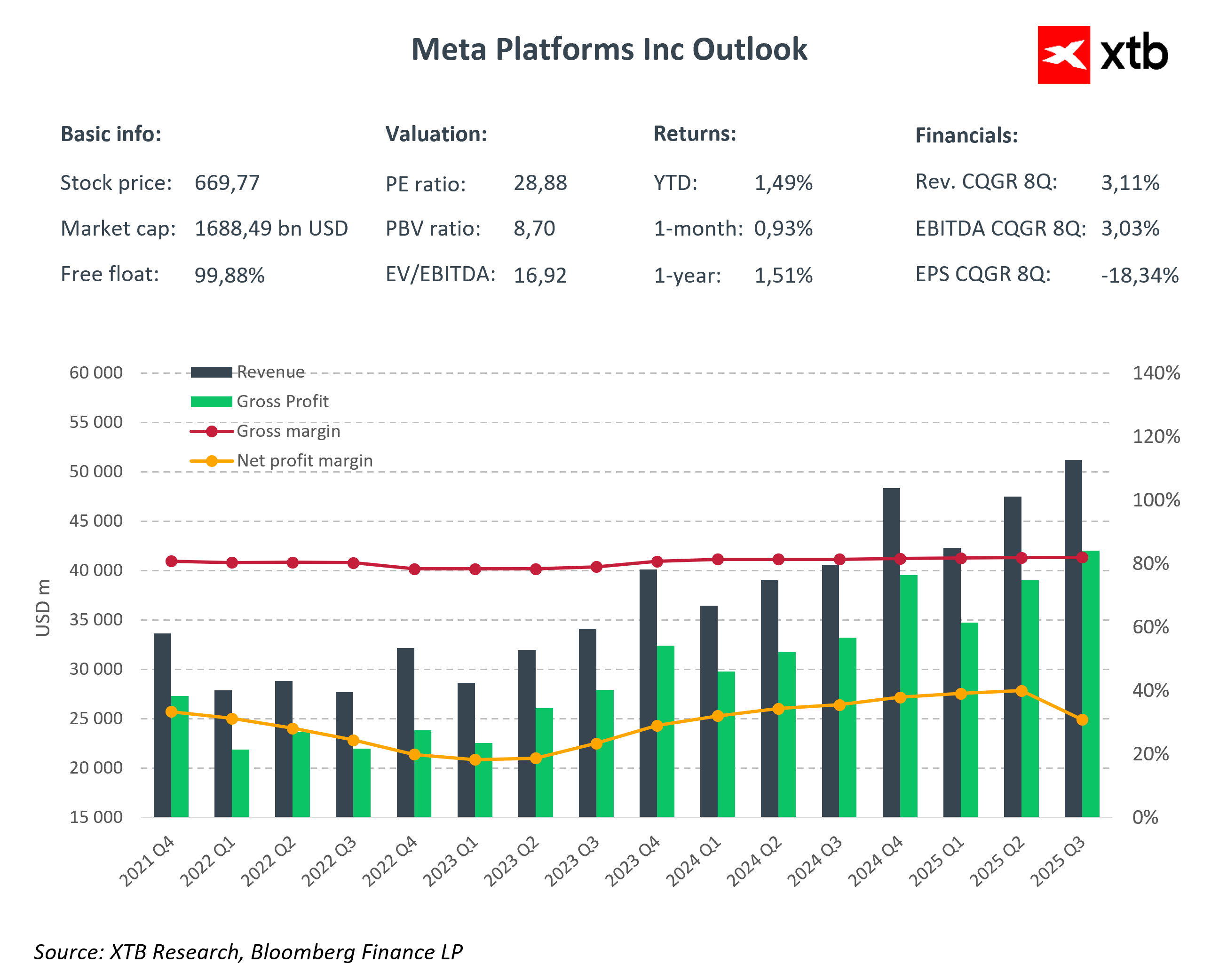

Market Consensus

-

Total Revenue: $58.40 billion

-

Net Income: $26.53 billion

-

EPS: $10.16

-

Gross Margin: 81.0%

-

Net Margin: 45.4%

-

EBITDA: $29.96 billion

-

CapEx: $21.97 billion

For investors, the key focus remains the growth structure. Meta is still largely an advertising-driven business, so the market will analyze whether revenue growth stems from genuine improvements in monetization efficiency and algorithms, rather than merely benefiting from a favorable macroeconomic environment.

Advertising and Algorithms – The Core of the Business Model

Digital advertising remains the absolute foundation of Meta’s results. Platforms like Facebook, Instagram, and WhatsApp provide the company with global reach, data scale, and precise targeting capabilities, resulting in some of the highest margins in the tech sector. The application of artificial intelligence in content recommendation systems and campaign optimization enhances ad effectiveness and increases return on investment for advertisers.

The development of generative AI tools also supports user engagement and improves monetization across existing platforms. Rapid, direct monetization of AI is one of Meta’s key competitive advantages among Big Tech peers.

AI and CapEx – A Conscious Scaling Strategy

Meta is significantly increasing capital expenditures, focusing on expanding data centers, computing infrastructure, and its own AI models. High CapEx is part of a deliberate strategy aimed at securing long-term competitive advantages and supporting increasingly sophisticated AI applications.

The company clearly communicates that the priority is scale and quality of infrastructure, even at the cost of short-term pressure on Free Cash Flow. Investors will, however, assess whether the pace of investment aligns with revenue growth and whether AI investments are beginning to deliver increasingly tangible financial returns.

Profitability and Operational Discipline

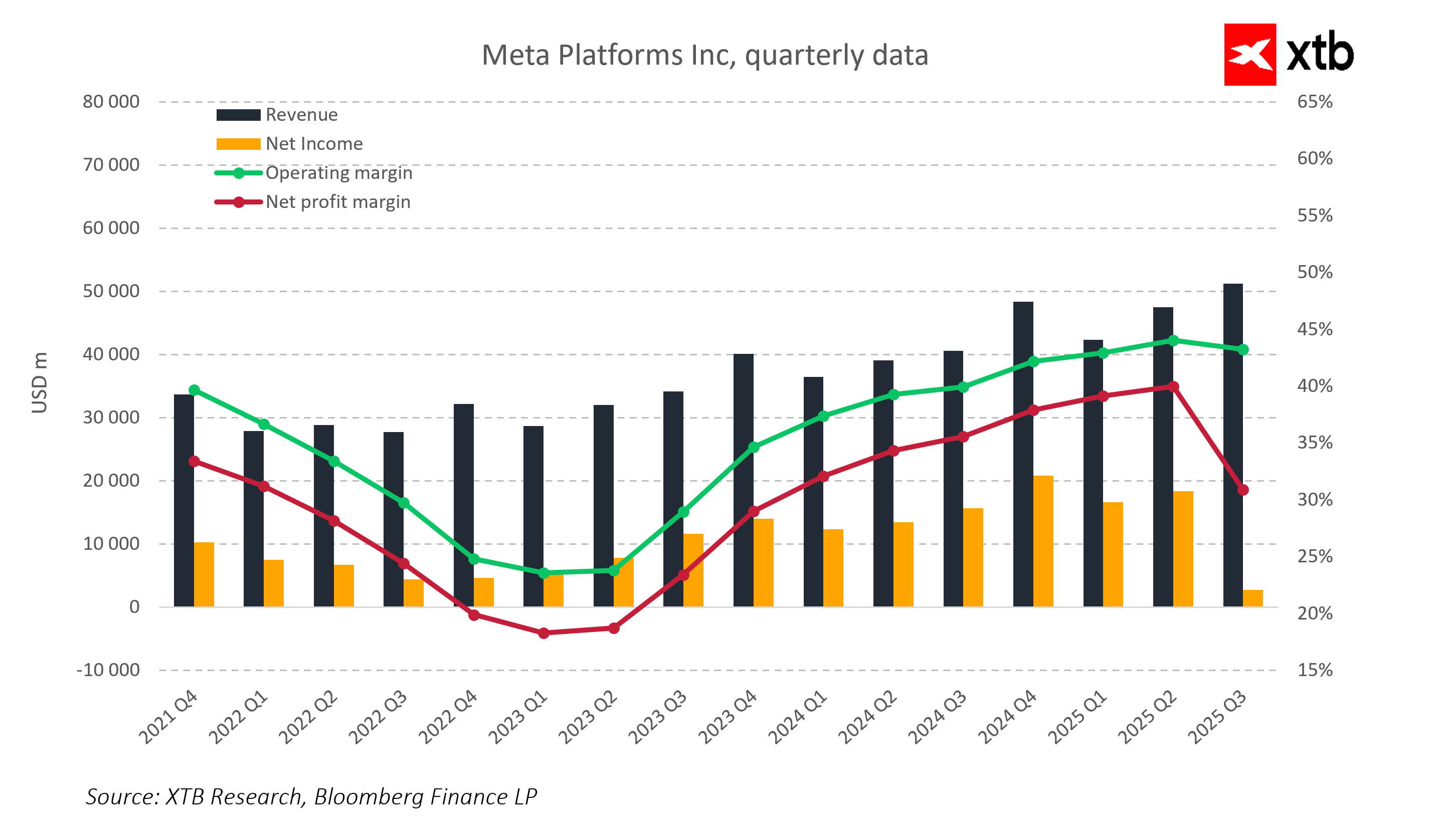

Despite aggressive investment, Meta remains one of the most profitable technology companies globally. Gross and net margins remain exceptionally high, reflecting the effectiveness of prior restructuring actions and the strength of its advertising model. The combination of high operating profitability and intensive investment positions Meta as a company with significant potential for further value expansion.

Key Takeaways

Meta is currently in a phase where it combines dynamic revenue growth, exceptional profitability, and aggressive AI investments. The central question is not whether the company can grow, but whether it can maintain balance between investment scale and its ability to continue monetizing its user base and AI technologies.

If Meta demonstrates that rising CapEx effectively translates into advertising revenue growth while maintaining high margins, the company could remain one of the most attractive players in the global technology sector. In this scenario, Q4 2025 results could confirm that the current strategy is not only working but also laying solid foundations for further value expansion in the coming years.

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.