- Global investor sentiment has climbed to its highest level since February.

- 83% of investors do not expect the Federal Reserve to raise interest rates before the U.S. midterm elections in November.

- Fund managers have lowered their year-end 2026 oil price forecast to $71 per barrel, down from $86 in June.

- Global investor sentiment has climbed to its highest level since February.

- 83% of investors do not expect the Federal Reserve to raise interest rates before the U.S. midterm elections in November.

- Fund managers have lowered their year-end 2026 oil price forecast to $71 per barrel, down from $86 in June.

The latest Bank of America Global Fund Manager Survey (BofA FMS) suggests institutional investors remain increasingly optimistic about technology stocks and the broader market outlook. At the same time, respondents see little chance of further Federal Reserve tightening before the U.S. midterm elections. The survey also indicates that a sustained rebound in oil prices back above $90 per barrel would come as a significant negative surprise for investors.

Key summary from the survey

- Global investor sentiment climbed to its highest level since February. Fund managers have become more optimistic about the economic outlook, AI-related capital spending, and the prospect of a more accommodative Federal Reserve.

- Cash allocations fell to 3.6% from 4.1% in June. According to Bank of America's methodology, such a low cash balance triggers a contrarian sell signal, suggesting investor optimism may have become excessive and that there is less room for additional risk-taking.

- A record 54% of respondents expect a "no landing" scenario for the global economy, meaning economic growth remains resilient without a meaningful slowdown. Only 2% anticipate a hard landing.

- Fund managers increased their allocation to U.S. equities to the highest overweight level since December 2024, reflecting growing confidence that U.S. stocks will continue to outperform global markets.

- Long positions in global semiconductor stocks were once again identified as the world's most crowded trade, cited by 82% of respondents for the third consecutive month. Although some investors trimmed technology exposure in July, none reported holding net short positions in the sector.

- A majority (61%) believe hyperscalers will not reduce capital expenditures this year, compared with 28% expecting spending cuts. This supports the view that investment in AI infrastructure, data centers, and advanced semiconductors is likely to remain elevated.

- The risk of an AI bubble was identified as the largest tail risk facing financial markets, with 45% of respondents highlighting it as their primary concern. This suggests investors remain highly optimistic about AI while simultaneously acknowledging growing valuation risks.

- Around 83% of respondents do not expect the Federal Reserve to raise interest rates before the U.S. midterm elections, reinforcing expectations for a more supportive monetary environment for risk assets.

- Fund managers also lowered their year-end 2026 oil price forecast to $71 per barrel, down from $86 in June. This indicates investors expect weaker inflationary pressure from energy markets than they did just one month ago.

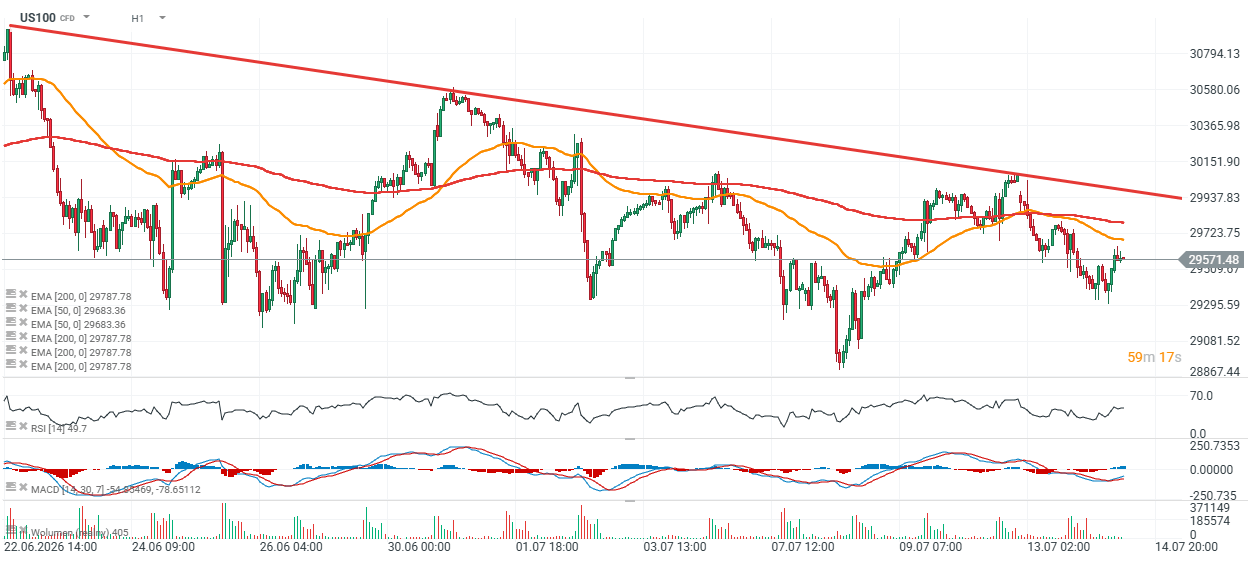

US100 chart (H1)

Looking at the US100 since June 2026, every test of the upper boundary of the prevailing trend channel has been followed by a strong rejection and a meaningful downside move. If history repeats itself, another rejection from current levels could increase the probability of a pullback toward the 29,000-point area.

Source: xStation5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Wheat extends correction, falls to its lowest level since July 10 🚩 Drought, El Niño and the Black Sea in focus

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.