Summary:

- China promised massive agricultural purchases

- US can struggle to produce enough of soybeans

- Could this be the chance for depressed corn?

Can China live up to the promise?

The main point of the trade deal is a massive increase of the Chinese imports from US with focus on agricultural goods. It’s supposed to rise by $200 bn over two years which means that by the end of 2021 it would more than double. It’d be a gross understatement to say it’s ambitious. US share in the Chinese imports hovered in a close range around 8% before the Trade War started and then dipped to some 6.5%. Recovering the lost ground is one thing but the deal would require this share to grow above 12% within two years.

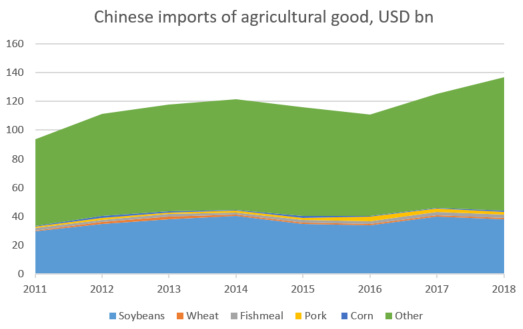

Beyond soybeans, Chinese imports of agricultural goods is very fragmented. Source: Bloomberg, XTB Research

Beyond soybeans, Chinese imports of agricultural goods is very fragmented. Source: Bloomberg, XTB Research

The main focus is imports of agricultural goods that stood around $20 bn a year before the TradeWar erupted and decimated it. China has promised to import around $40 bn a year with intention to add another $5 bn if possible. But is $40 bn even technically possible? Let’s have a look. China is buying agricultural goods worth around $120bn a year so it looks like there’s plenty of space. However, US exports in this area has been dominated by soybeans (at around 55-60% rate). At present prices China is importing soybeans worth around $33 bn a year and the US is responsible for just 15% of that amount (because of tariffs), down from a standard of 45-50%. Let’s assume that China imports as much as 65% (higher number is implausible because of harvest season overlap with that in South America) of their purchases to the US and that leads to 20% price increase. That results in less than $26bn of imports and if other goods made up for the 40% of the total imports, the total would be close to $43bn. So technically the promise is deliverable but only under the most optimistic assumptions: 1) China forcing firms to buy more expensive soybeans from the US 2) imports leading to a major price rally in soybeans 3) significant increase in imports of other goods which is very fragmented and could be hard to stimulate (beef is the second largest good at around $1bn annually amid meat crisis in China). Even if China cleared all those hurdles and delivered such a massive increase in demand, would the US output adjust?

Can the US produce enough soybeans?

The 2019 season was hit by both Trade Wars and weather but the next season should bring an improvement. Assuming a return to average acreage and yields from previous years output should total about 115MT and exports 55MT. If China were to buy the amounts we pointed out above at prices 20% higher than today, exports to China ALONE would need to stand at 59MT. Using average price from 2016 (a year of record China soybean imports from US) that amount would need to rise to 66MT. Given domestic consumption of about 60MT that would already be above the capacity and there’s still exports to other countries that hovers around 20MT.

Impact on SOYBEAN, CORN

Soybean prices have bounced back sharply recently in response to the phase-one trade deal struck between Washington and Beijing. We think that the ongoing rally could continue once the US exports a huge amount of grains to China in the coming quarters. In theory, a move through the highs from 2018 could occur. Source: xStation5

Soybean prices have bounced back sharply recently in response to the phase-one trade deal struck between Washington and Beijing. We think that the ongoing rally could continue once the US exports a huge amount of grains to China in the coming quarters. In theory, a move through the highs from 2018 could occur. Source: xStation5

As far as corn prices are concerned, we have not seen any major price moves of late. However, in this case we also see some upside should China start buying ethanol from the US. Under these circumstances (the most bullish case in our view) we estimate that US corn stocks could depleted as much as 30%. If so, corn could also see increased buyers’ interest. Source: xStation5

As far as corn prices are concerned, we have not seen any major price moves of late. However, in this case we also see some upside should China start buying ethanol from the US. Under these circumstances (the most bullish case in our view) we estimate that US corn stocks could depleted as much as 30%. If so, corn could also see increased buyers’ interest. Source: xStation5

Oil price surge on US/Iran

Iran Breaks Ceasefire🚨Indices Under Pressure

US100 gains 1% before Nvidia earnings📈

Will Powell remain hawkish❓

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.