- Meta Compute could become a new revenue stream for Meta Platforms, much like AWS eventually became Amazon's most important business.

- The sell-off in memory stocks may be overdone, as successful AI compute leasing could actually improve the economics of further investments in GPUs, HBM memory, and data centers.

- If Meta proves that AI infrastructure can generate meaningful cash flow, current valuations of the largest hyperscalers may prove too conservative.

- Meta Compute could become a new revenue stream for Meta Platforms, much like AWS eventually became Amazon's most important business.

- The sell-off in memory stocks may be overdone, as successful AI compute leasing could actually improve the economics of further investments in GPUs, HBM memory, and data centers.

- If Meta proves that AI infrastructure can generate meaningful cash flow, current valuations of the largest hyperscalers may prove too conservative.

Meta Platforms has been investing tens of billions of dollars in artificial intelligence for years, yet the market has largely viewed these expenditures as a cost. The announcement of Meta Compute—the commercialization of its own AI infrastructure—could be the first sign that the era of massive AI spending is beginning to transition into a phase of monetization. As a result, investors rushed to sell data center memory stocks, assuming that Meta has excess computing capacity. This may be an overly simplistic interpretation. While weak execution of Meta's new business could become a warning sign, its success could prove to be one of the most bullish developments for the entire AI industry.

- Meta Compute could create a new, high-margin revenue stream for Meta by leasing computing capacity and AI models.

- According to Morgan Stanley, leasing 250 MW of computing capacity could increase Meta's earnings per share by around USD 3 in 2028, while a 1 GW scenario could boost EPS by as much as USD 11.9—roughly equivalent to 50% of the company's projected 2025 annual earnings.

- If AI infrastructure begins generating meaningful cash flow, current valuations of the world's largest hyperscalers may prove far too conservative.

Did the market jump to the wrong conclusion?

The strongest market reaction following reports about Meta Compute was a sell-off in companies supplying memory used in AI data centers. Investors concluded that if Meta plans to lease out its own computing capacity, it probably has more GPU infrastructure than it currently needs, implying lower future demand for HBM memory, DDR5 modules and enterprise SSDs.

That scenario is certainly possible, but it is far from the only explanation. Meta may simply be looking to improve utilization rates of infrastructure that was built for the long-term expansion of its AI ecosystem. In other words, the company may be trying to increase the return on investments it has already made rather than reduce future investments.

The market moved remarkably quickly from news about a new business model to the conclusion that the AI industry faces structural GPU oversupply. History suggests the opposite is often true—once infrastructure starts generating revenue, companies typically invest even more aggressively rather than slowing down capital spending.

The enormous potential of Meta Compute

Perhaps the most interesting aspect comes from Morgan Stanley's estimates regarding the potential financial impact of Meta Compute. The bank believes Meta could commercialize part of its AI infrastructure by leasing computing capacity to third-party customers without necessarily building a full-scale competitor to AWS or Microsoft Azure.

According to Morgan Stanley, leasing roughly 250 MW of computing capacity for one year at approximately USD 40 per watt could increase Meta's 2028 earnings per share by around USD 3. Under a more optimistic scenario involving the commercialization of approximately 1 GW, the potential impact rises to nearly USD 12 per share, equivalent to almost one-third of the company's projected annual earnings.

Naturally, this does not mean such a scenario will materialize. However, it clearly illustrates the magnitude of the operating leverage embedded in AI infrastructure and suggests the market may still be significantly underestimating the monetization opportunity.

Success of Meta Compute does not necessarily mean trouble for the memory industry

Today's investor concerns are focused primarily on future demand for HBM memory, DDR5 modules and other components used in AI data centers. If Meta increases utilization of its existing GPU clusters, part of the market automatically assumes that future hardware orders will decline.

However, this ignores the most important variable in the equation—the return on investment. If leasing computing capacity proves profitable, every additional AI cluster becomes economically more attractive. Higher revenue generated by each deployed GPU means faster payback periods and stronger incentives to continue expanding infrastructure.

Paradoxically, successful execution of Meta Compute could ultimately support long-term demand for GPUs, AI accelerators and advanced memory rather than weaken it. The key question is not whether Meta currently has spare capacity, but whether it can successfully attract enough customers to monetize those resources.

The biggest threat may not be chipmakers

Companies whose business model relies almost entirely on renting GPU capacity appear considerably more vulnerable. Businesses such as CoreWeave and Nebius have built their strategy around supplying computing power to enterprises developing AI applications.

If Meta, Microsoft, Google and Amazon begin offering similar services at scale, the competitive advantage of these specialized providers could quickly erode. The world's largest hyperscalers benefit from significantly lower funding costs, global infrastructure, integrated software ecosystems and established enterprise customer relationships.

In practice, Meta Compute may not represent a threat to the AI industry itself, but rather the beginning of consolidation within the GPU cloud market. Specialized operators could face the greatest competitive pressure, while Meta's new business could eventually become a major profit engine. Such a scenario would also be highly bullish for Wall Street as a whole.

druga

AI is consuming enormous amounts of capital, but the market may be too short-sighted

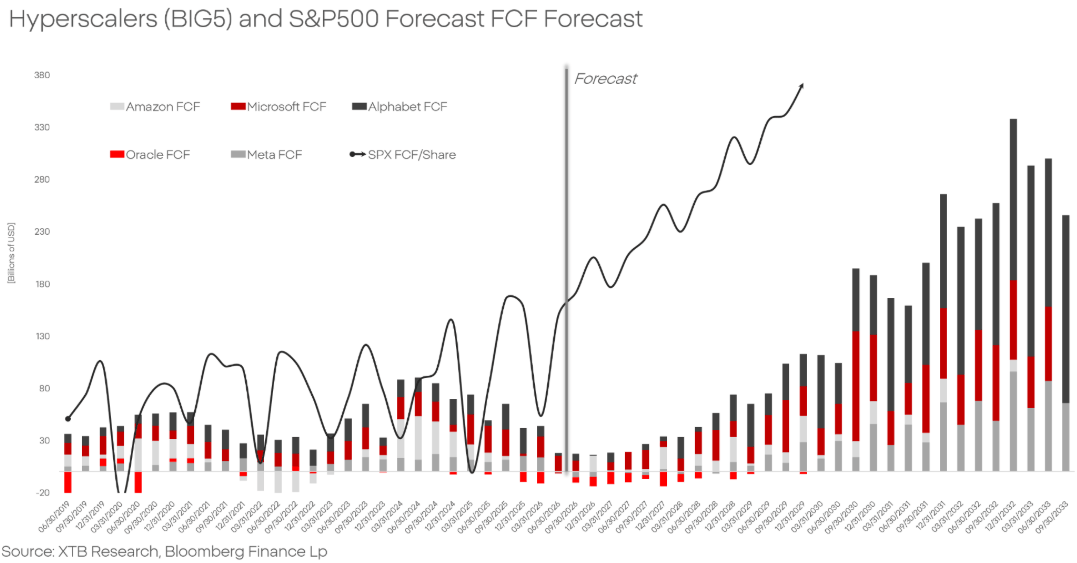

According to estimates, the world's largest hyperscalers are expected to invest approximately USD 750 billion in AI infrastructure during 2026. For many investors, these expenditures are seen primarily as a drag on free cash flow and a source of uncertainty regarding future returns.

History tells a different story. Every major technology platform—from cloud computing to the internet and mobile communications—went through a phase of exceptionally high capital expenditure before entering a period of rapid monetization. Massive investment comes first; meaningful cash flow follows later.

If Meta Compute succeeds, it could become one of the first clear signs that the AI industry is moving beyond the infrastructure buildout phase and into the cash generation phase. From an investment perspective, that would be far more significant than another record quarter of AI capital spending.

It is also worth noting that assuming the world's largest technology companies are collectively investing trillions of dollars only to ultimately destroy shareholder value seems rather naive. While investors currently focus almost exclusively on costs, Big Tech's long-term objective may be to capture an increasingly larger share of profits generated across dozens of industries through AI agents, proprietary models and lower inference costs.

Forecasts suggest that after this period of record AI investment, the largest hyperscalers could begin generating rapidly accelerating free cash flow (FCF) from 2028 onward. This would mark a transition from a phase of heavy capital investment to one focused on monetizing AI infrastructure and expanding profitability. If these projections prove correct, today's AI spending could become the foundation for the next decade of cash flow growth.

Source: XTB Research, Bloomberg Finance L.P.

Are hyperscaler valuations too conservative?

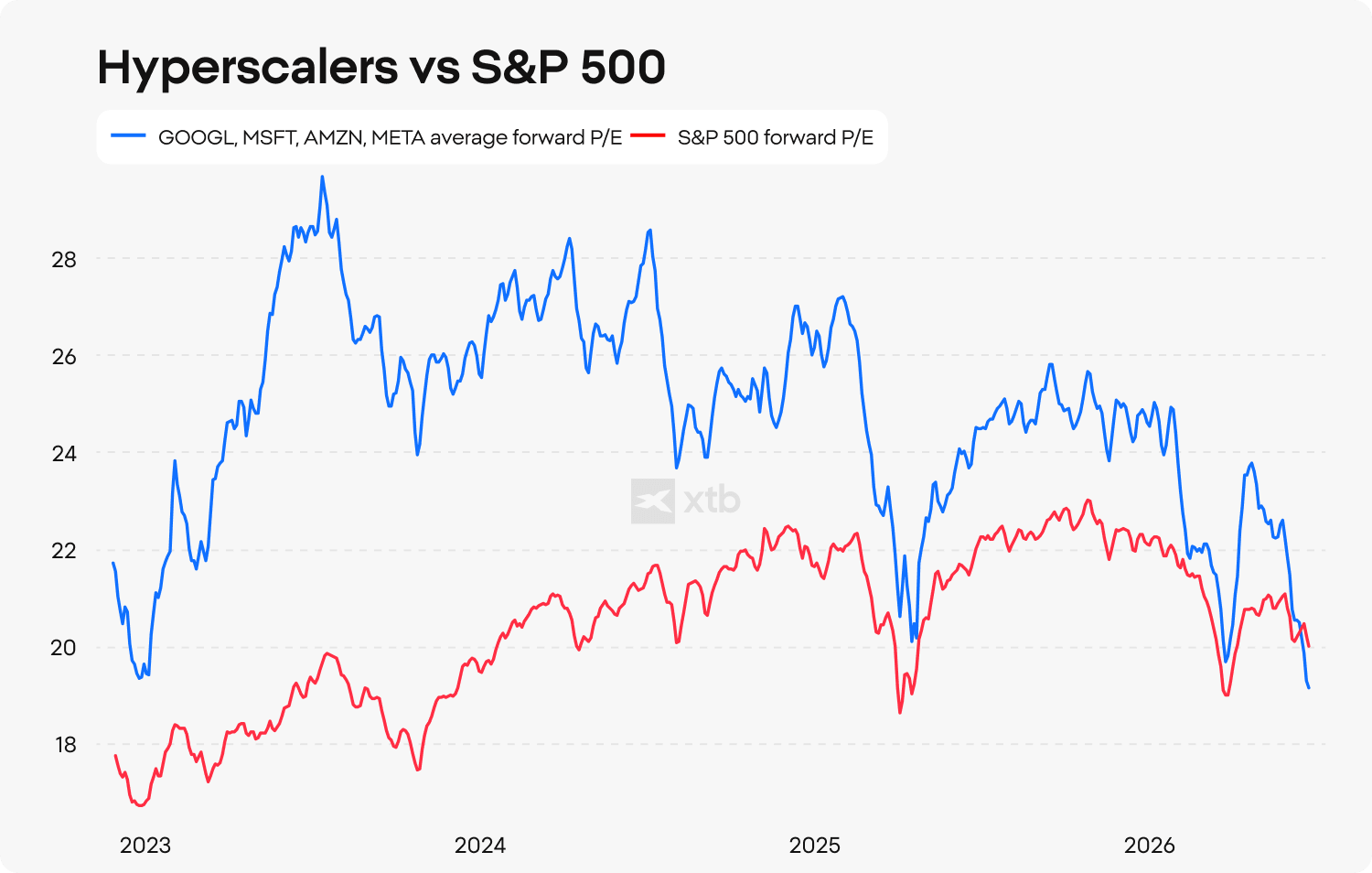

Despite record AI investments, the world's largest technology companies continue to trade at relatively attractive valuations compared with the broader market. The average 12-month forward price-to-earnings ratio for leading hyperscalers has fallen to its lowest relative level versus the S&P 500 since ChatGPT was launched, suggesting investors have become increasingly cautious about the sector's future earnings potential.

The market remains focused primarily on the cost of building AI infrastructure while paying far less attention to the revenue opportunities associated with AI models, AI agents and computing capacity services. In my opinion, this shift in narrative—from spending to monetization—could become one of the defining investment themes of the coming years.

My conclusion remains straightforward. If Meta proves it can successfully monetize its AI infrastructure, it would represent a bullish signal not only for the company itself but for the entire artificial intelligence investment theme. Under such a scenario, today's valuations of Meta Platforms and other leading hyperscalers could prove significantly too low from a long-term perspective.

Source: XTB Research

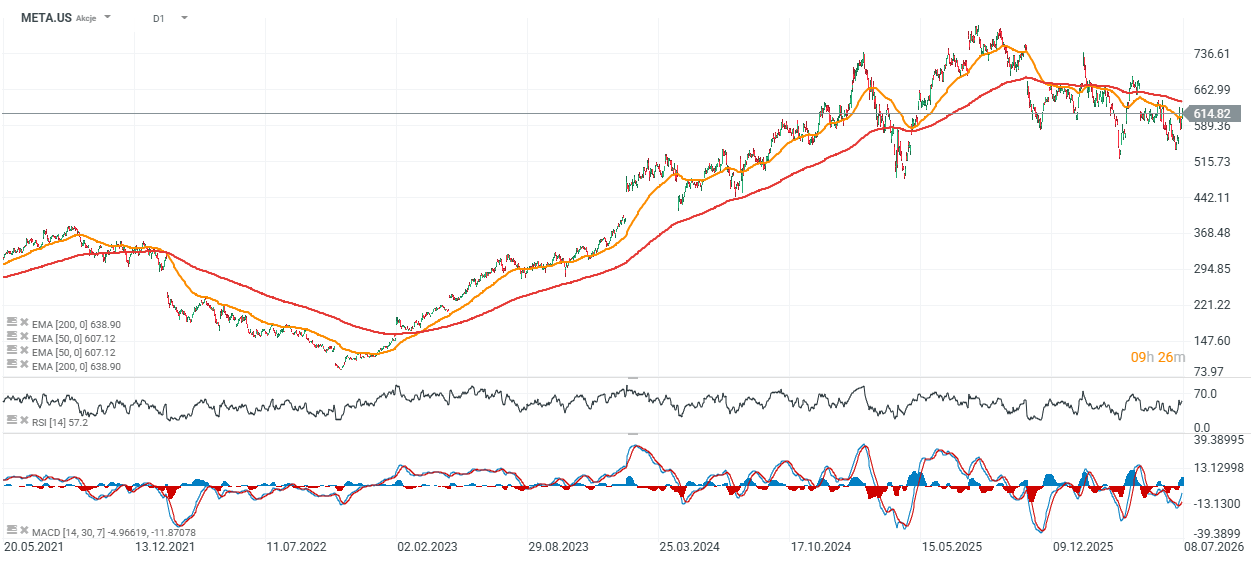

Meta Platforms stock (Daily chart)

Meta shares are currently trading slightly below the 200-day exponential moving average (EMA200), represented by the red line on the chart. This suggests the stock may be approaching a classic "make-or-break" moment: either buyers regain control and the long-term uptrend resumes, or selling pressure intensifies, potentially pushing the shares back toward the USD 500 area, where the last major support zone emerged.

Source: xStation 5

Eryk Szmyd Financial Market Analyst, XTB

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.