Ams OSRAM may be associated by most investors with selling light bulbs. However, recent events and changes at the company are forcing the market to look at it differently. The company has real potential to become another bottleneck for the AI industry.

The situation at ams OSRAM is complex. On one hand, it has technology, experience, a broad portfolio, and extremely interesting growth options. On the other hand, it remains a company coming out of a difficult restructuring, with high debt, net losses, and a range of risks to its strategy.

Yet the opportunities in front of the company and the potential upside in valuation are so impressive that it is hard to ignore.

What does ams OSRAM actually do?

AMS OSRAM is a European manufacturer of optical and sensor solutions. Its products go to, among others, the automotive sector, consumer electronics, industry, and medical applications. The most important new thread, however, concerns AI data centers.

Company is undergoing a gradual transformation toward a model more focused on Digital Photonics (DP), meaning the use of light to transmit and process information.

This is a market with enormous potential. It may turn out to be a dead end, or the foundation of another technological revolution. The company is not entering new areas without experience. Its technological base includes more than 12,000 patents.

A breakthrough hire

The core of the investment thesis is the application of digital photonics in AI.

In large AI systems, the problem is no longer only the number of GPU chips. An increasingly important constraint is how fast and how energy efficiently data can be moved between them. Traditional cable connections have limitations: the larger the compute cluster and the longer the distance, the greater the energy losses, the more heat, and the higher the complexity of the entire system. This is important and promising

in the context of historical precedents. Revolutions and breakthrough inventions were not based on single discoveries, but on a series of innovative mechanisms and methods combined into one system.

That is why the industry has started looking for other solutions, including optical ones. Instead of transmitting signals electrically, part of the communication can be done using light. This can potentially reduce energy consumption and improve throughput.

A piece of news from the last few days that turns speculative investment theses into a new business model being built before our eyes is the transfer of one of Nvidia Networking’s managers to ams OSRAM. Hiring elite personnel from the very forefront of the AI and semiconductor revolution does not guarantee success, but it clearly brings it closer.

A bright future (?)

Based on current data, investment banks estimate DP-AI revenue at around EUR 200 million per year around 2030. These are meaningful amounts, but today the company’s revenue is EUR 3 billion, so institutional enthusiasm is currently limited. What could change that?

To answer this question, you have to look inside the data centers being built around the world:

- First, compute centers are evolving toward ever larger numbers of specialized GPUs per AI cluster. More GPUs mean the need for more switches and cables. That means latency, throughput problems, and energy loss through excessive heat generation, which then has to be removed. Photonics can reduce two cost factors at once while improving performance.

- These are not speculations. Nvidia itself, in its research articles, indicates that proper use of existing solutions can reduce energy consumption by 350% versus traditional switches. In addition, billions of switches, cables, and sockets mean billions of opportunities for mechanical failures. Light-based solutions remove most materials and moving parts from the infrastructure.

- Moreover, research also shows that the compute power of AI infrastructure increased by 300% in two years. At the current growth rate, which is expected to rise, we can quickly find ourselves in a situation where HBM memory becomes a bottleneck, because in that industry throughput increased by “only” around 150% over the same period. At that point, photonics stops being a curiosity and becomes a necessity.

Beyond a completely new market driven by potential bottlenecks, the company has a number of “old” and more down to earth businesses. One of them is VR/AR glasses, where the company is also an important player. Jefferies estimates the company could supply components worth more than EUR 50 per device, and with an assumed volume of about 5 million units in 2028, this could mean around EUR 375 million in revenue.

The balance sheet weighs on the growth thesis

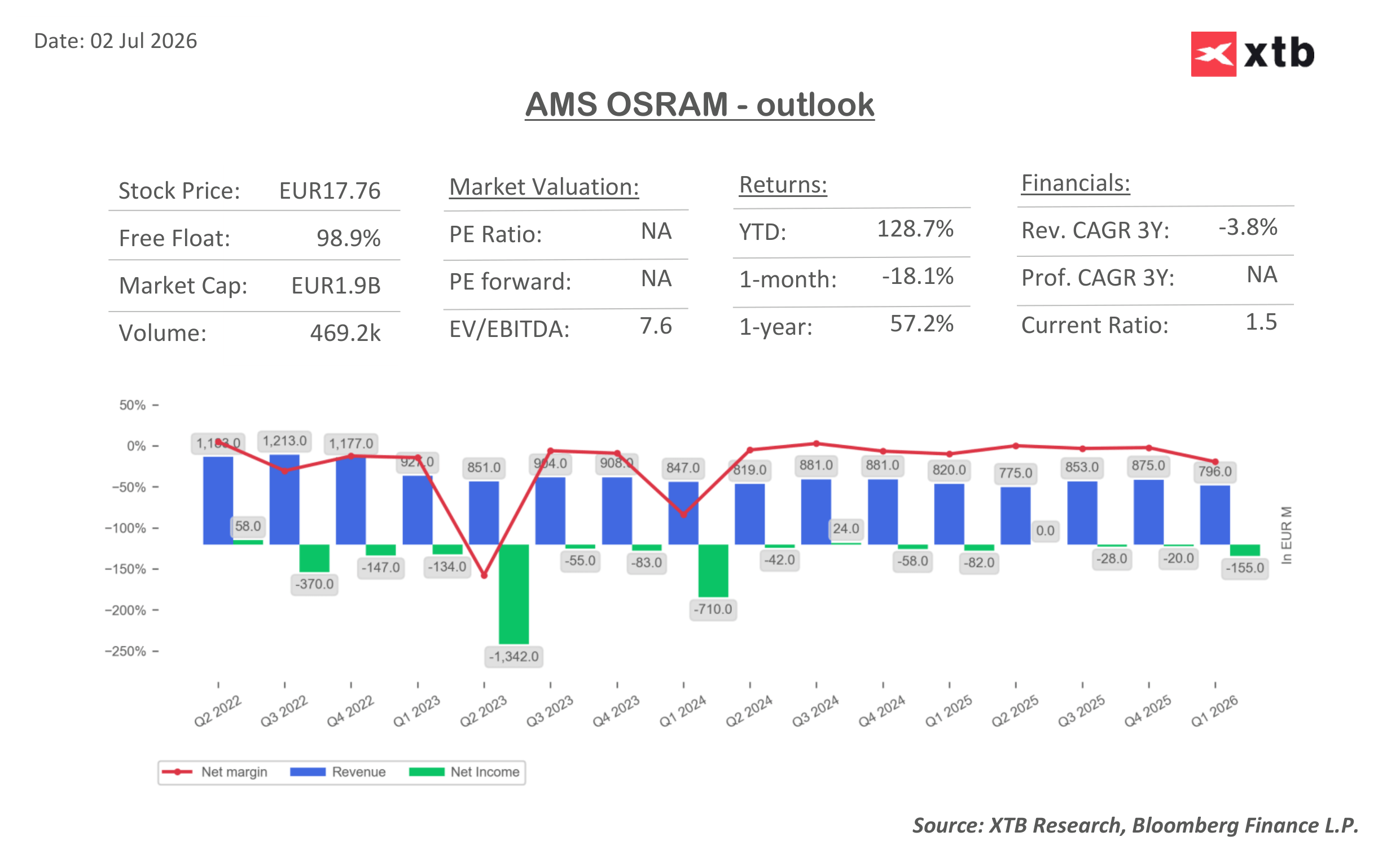

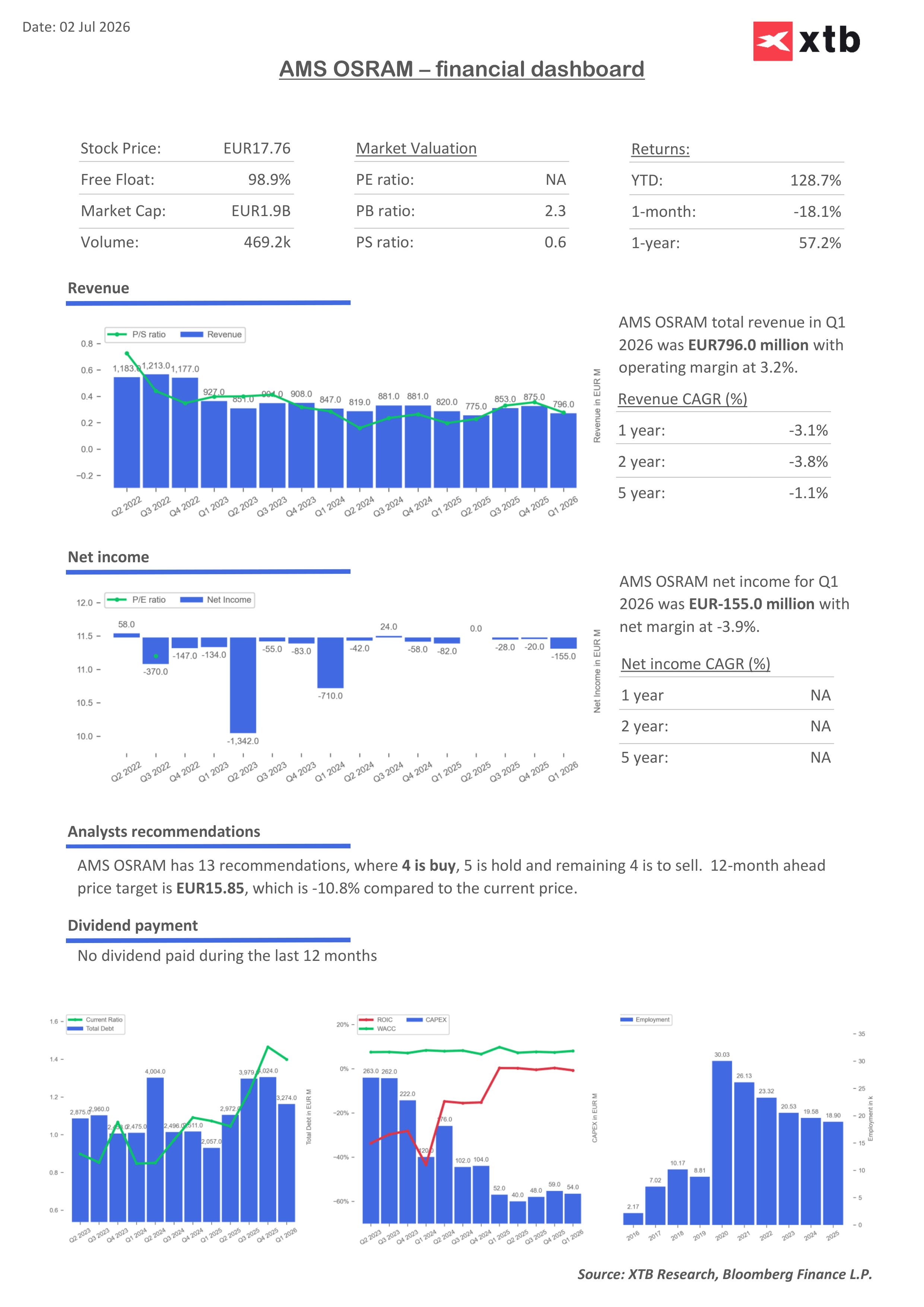

The biggest problem for ams OSRAM is not a lack of technology, but finances. The company still reports net losses, and according to the report in Q1 2026 the net loss was about EUR 154 million. Analysts expect earnings per share to remain negative throughout 2026, with positive results expected only in 2027.

That means the market is buying mainly the future today, not the present. This is a risk, but it also implies a huge discount to profits, which may realistically never appear or may turn out to be much lower.

Revenues are large and EBITDA remains positive, but net income and free cash flow are weak. The report also points to high financial leverage, with EBITDA leverage according to Fitch at 6.3x at the end of 2025.

These numbers cool the growth narrative. The company may have attractive technology, but if the transformation takes longer and cash flows remain weak, financial risk will constantly limit its room to operate.

Mitigation measures

AMS OSRAM is trying to improve the situation through restructuring and asset sales. The “Simplify” program is expected to deliver around EUR 200 million in annual savings by 2028, and divestments are expected to generate about EUR 670 million in proceeds. According to the report, this is intended to support debt reduction and the path to positive free cash flow in 2027.

This is an important piece of the puzzle. If the savings, asset sales, and an improvement in the automotive cycle coincide with the first signals of commercialization in AI photonics or AR, ams OSRAM may start to look like a company after a successful restructuring. If, however, any of these elements fails, the market may quickly return to questioning the company’s future.

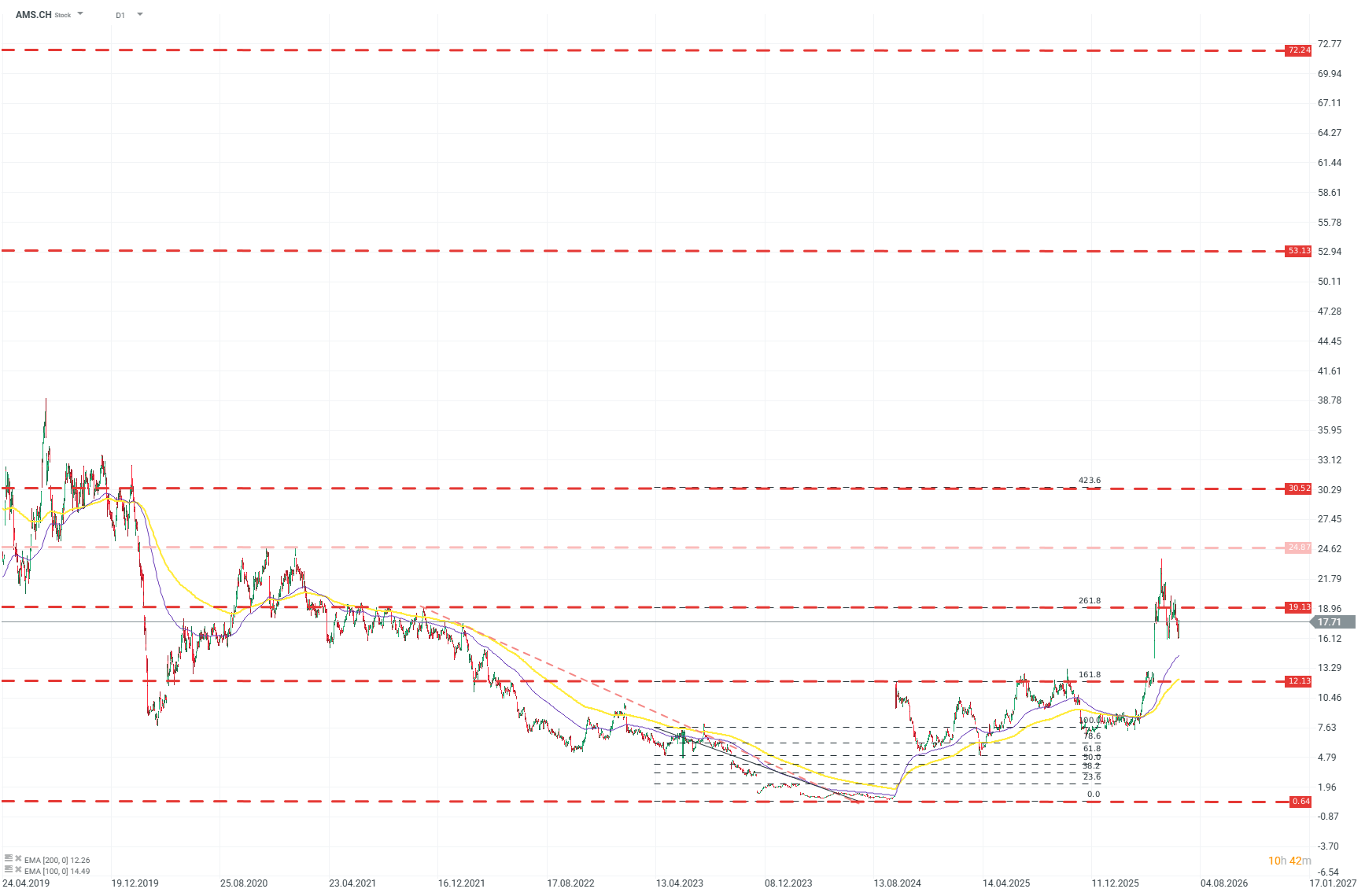

AMS.CH (D1)

Company has already seen substatincial growth from its bottom, of aprox. 2000%, with over 100% growth in last 3 months. Despite that, company has still a long way to recover its pre-2022 valuations. Source: xStation5

Kamil Szczepański

Financial Markets Analyst, XTB

All or nothing: ServiceNow earnings preview

Did SaaS lost too much? Morgan Stanley says yes.

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.