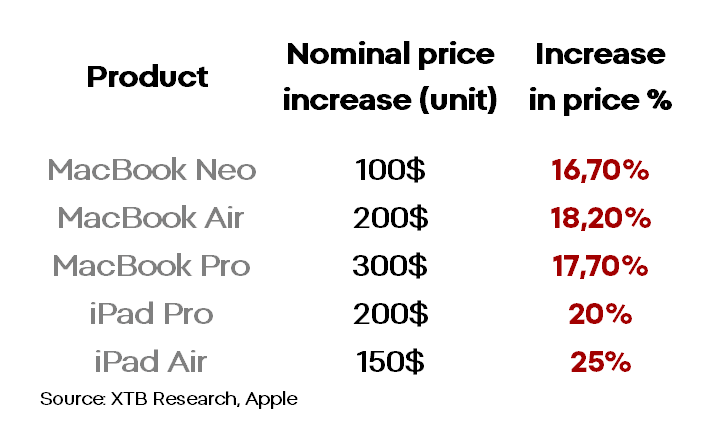

Apple, a manufacturer and distributor (mainly) of iPhones and Mac computers, announced significant price increases for its products on Thursday - price rises reaching several dozen percent.

The market reacted negatively, with the company’s shares down more than 5%.

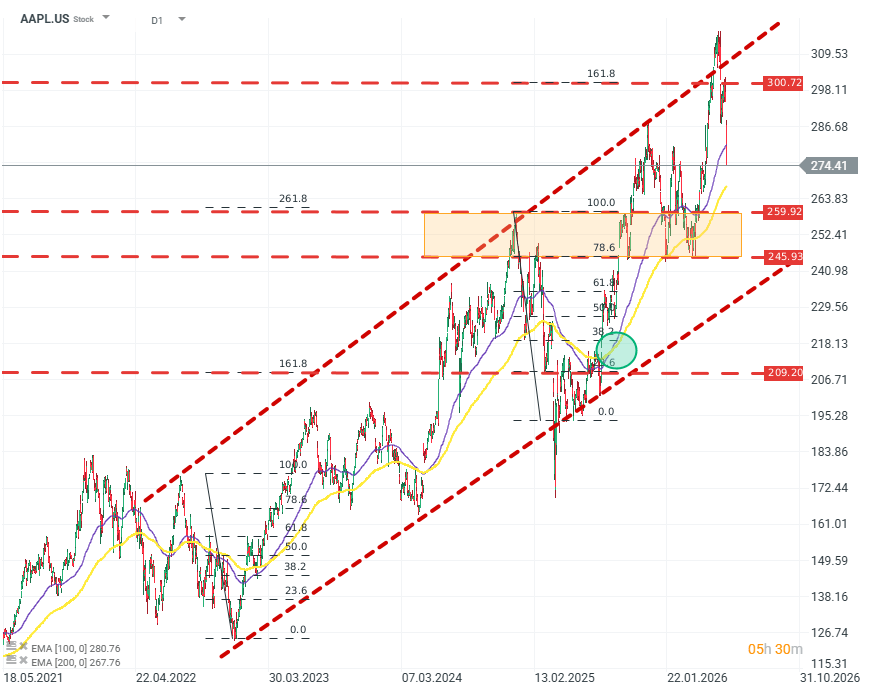

APLE.US (D1)

The company’s valuation remains in a long-term, expanding uptrend. FIBO projections indicate a strong resistance zone between $260–240. This zone will coincide with the (potential) lower boundary of the rising channel—which means that deepening the downward correction will become an increasingly bigger challenge for sellers. It is also worth noting the EMA100 crossing above the EMA200 from below, which can be interpreted as a strong bullish signal. Source: xStation5

In a standard market context, raising prices in this way would signal the company’s confidence in demand for its products, and investors would have flowed into the stock on expectations of higher margins.

In this particular case, however, the company clearly states that the price hikes are the result of rising RAM memory prices. Computers and phones must compete for memory supply with data centers and the enormous budgets of the largest AI-related corporations.

As a result, the market does not see margin expansion, only a desperate attempt to defend margins. A defense that, it should be noted, may not be effective. Why?

Based on rough estimates and independent analyses, the cost of RAM in Apple products is around a dozen or so percent of total production costs; however, this share increases as a given machine’s configuration becomes more advanced.

At the same time, over the past year, memory prices in the segment in which Apple operates have risen by about 150–200%. Price increases of around 20%, with a cost share in the neighborhood of 10–20%, mean that the current hikes can only offset the increase in costs, with no hope of margin expansion and with expected pressure on sales growth.

It should also be remembered that there is no sign of an end to this “cycle” in the forecasts or results of companies in the memory or semiconductor sectors. In the worst case, this may be only the first of many price increases.

These events and their implications may partially be one of the bearish factors for the broader market. Investors must, should, and will increasingly begin to price in supply chains stretched to the limit and rising electronic component costs across the entire market, not just for selected companies.

Such speculation could spill over, for example, into the valuations of Take-Two, which is rising on expectations surrounding GTA VI. Component shortages and higher prices may discourage or prevent many consumers from trying Rockstar’s new release.

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.