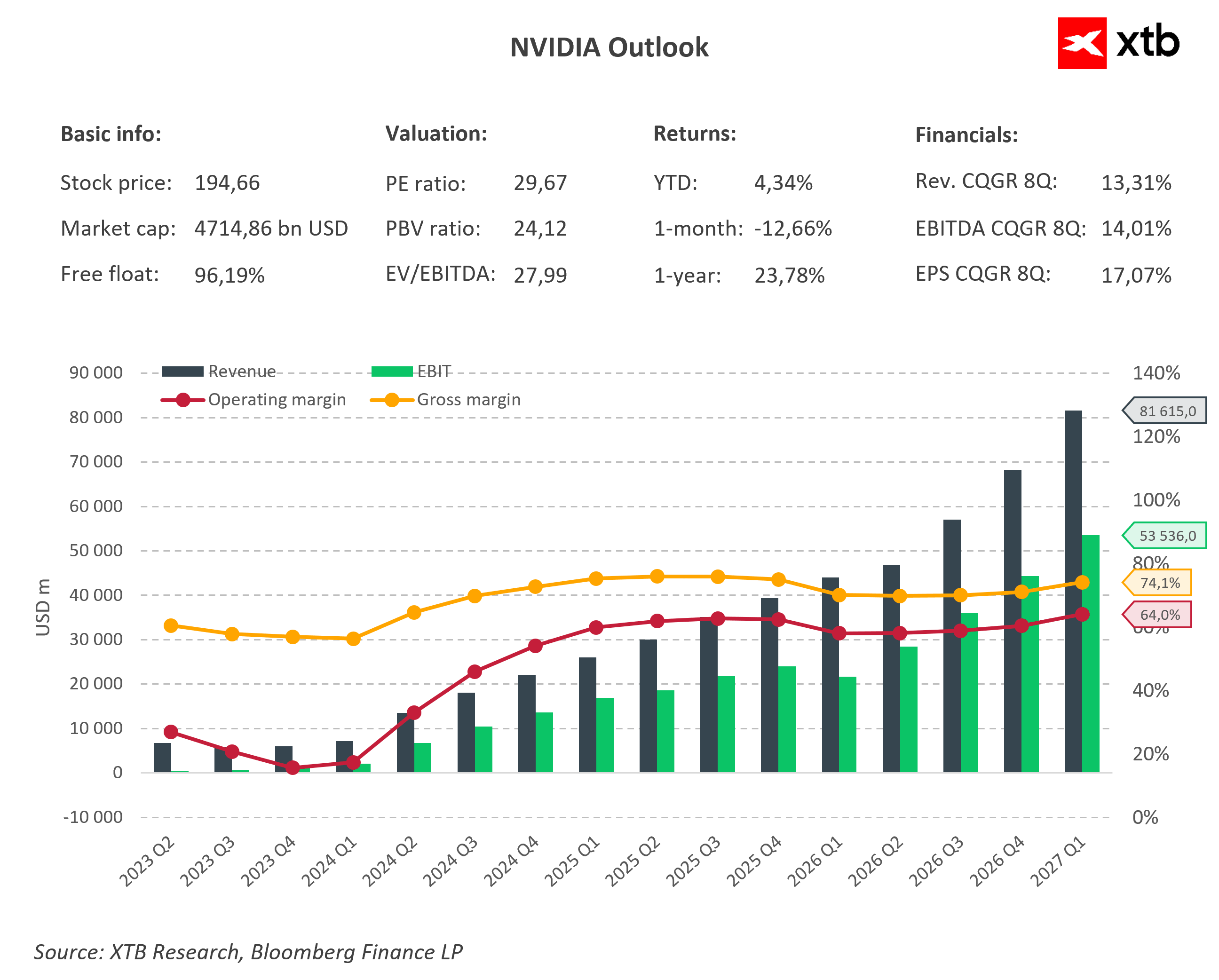

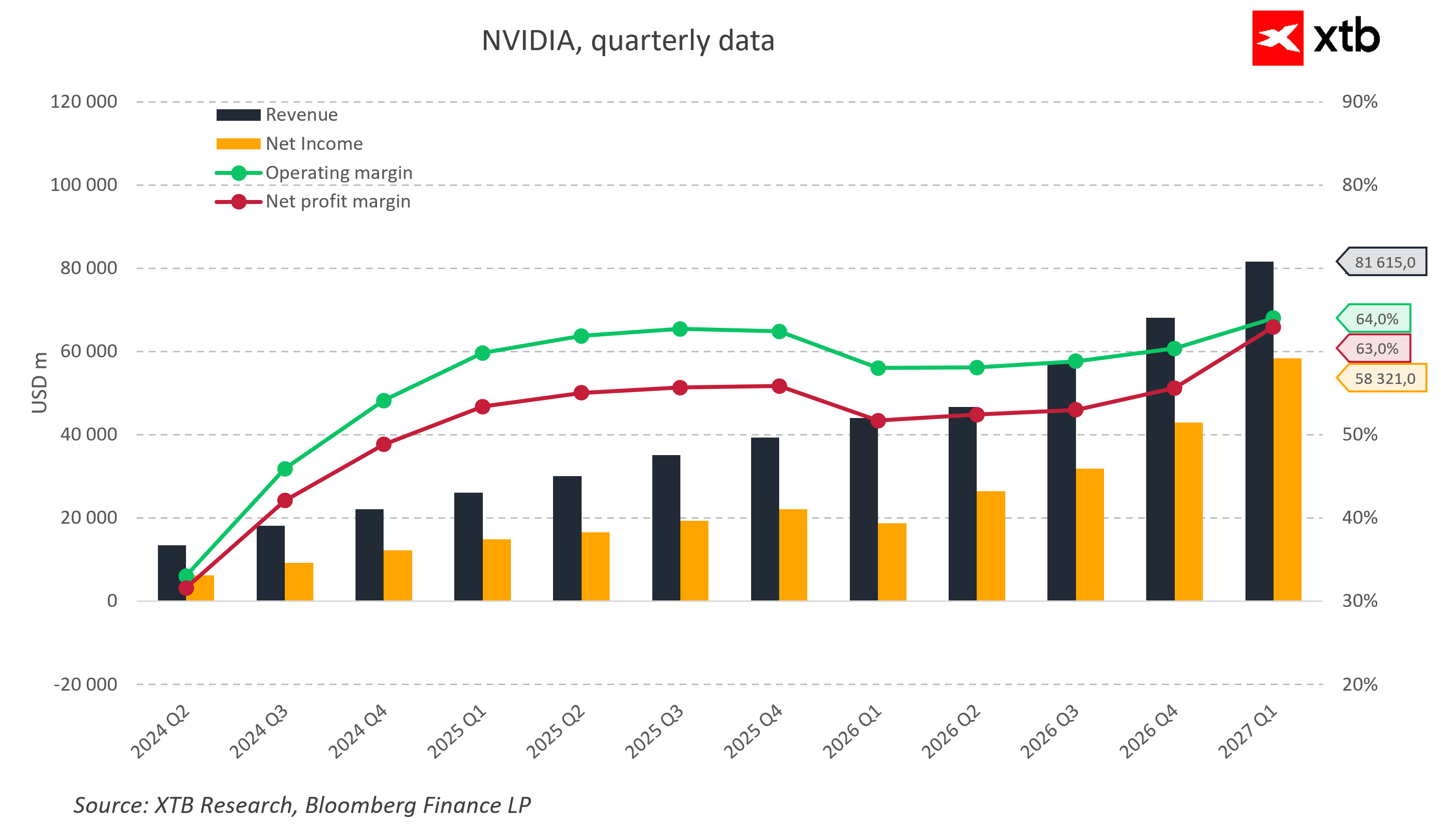

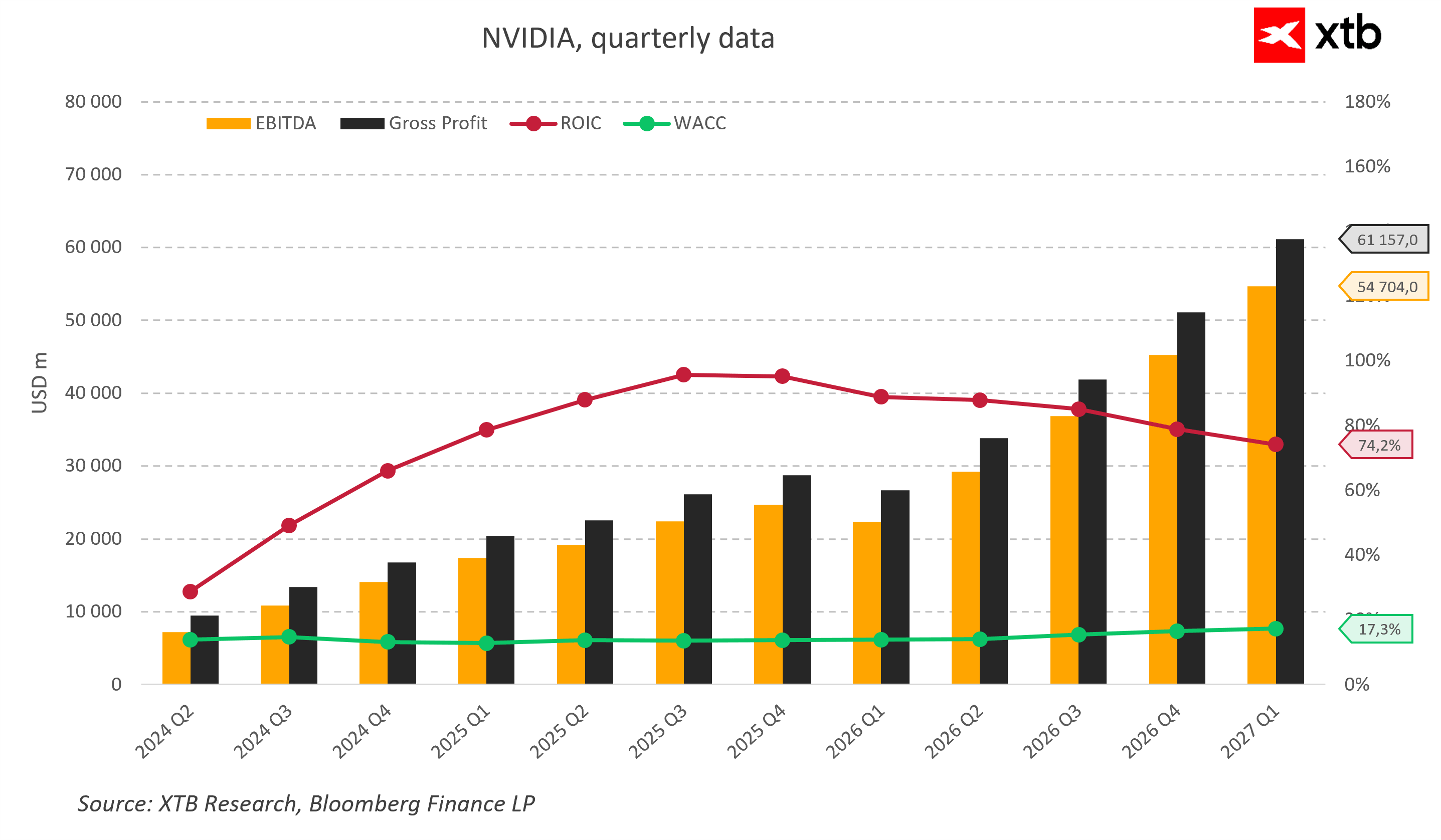

Recent reports of delays in Nvidia’s next-generation AI infrastructure, including systems based on the Vera Rubin platform, are causing a noticeable shift in the narrative around the company. Until recently, the market was focused almost exclusively on the scale of demand for AI infrastructure and Nvidia’s ability to meet it. Today, however, an increasingly important question is the pace of execution of this cycle and its actual operational efficiency.

On one hand, production delays in the most advanced systems can be seen as natural friction within an extremely complex supply chain. The technological scale of the current investment cycle is unprecedented, and each step toward higher performance requires increasingly sophisticated manufacturing and integration processes. From this perspective, delays do not change the underlying trend but merely stretch it over time.

On the other hand, the market is beginning to pay closer attention to whether the pace of infrastructure build-out is starting to outstrip the pace of its real-world utilization. In this context, signals from major hyperscalers, including Meta, are particularly important, as they are reportedly exploring the potential commercialization of unused computing capacity. Such a move, even if marginal, suggests that the system may be experiencing periodic oversupply relative to current demand for AI computation.

In the short term, this creates a mixed picture for Nvidia. Delays in deliveries of next-generation systems may raise concerns about the continuity of revenue growth in the most advanced product segment, which is also the one responsible for the highest margins and strongest growth dynamics. At the same time, supply constraints continue to support pricing power, as hyperscaler demand remains very strong and far from saturation.

In the medium term, the key question is whether these developments represent only a temporary effect of production complexity or the first signal of a phase in which the AI market begins to shift from rapid expansion toward a more selective investment approach. Previous technology cycles have shown that even within strong structural uptrends, there are periods when investment outpaces the real ability to monetize it, leading to natural phases of cooling in spending momentum.

In the long term, however, the picture remains more stable. Demand for computing power driven by the development of large language models, agent-based systems, and business process automation continues to point to a structural increase in demand. Even if the pace of investment temporarily levels out, it does not change the fact that AI infrastructure, including next-generation platforms such as Rubin, remains one of the key pillars of the technological transformation of this decade.

At the same time, increasing importance is being placed on how efficiently existing infrastructure is being utilized. Emerging signals regarding the potential sale of unused computing capacity by some major players, including Meta, may indicate that the market is entering a more advanced stage of resource optimization. This would imply a shift in focus from pure capacity expansion toward monetization and better alignment with actual demand.

In this environment, Nvidia remains at the center of a paradoxical situation. On one hand, it continues to benefit from one of the strongest structural growth trends in the entire artificial intelligence ecosystem. On the other hand, it is becoming increasingly clear that this growth path will not be linear, and its pace will depend more heavily on the synchronization between infrastructure expansion and its actual utilization. It is this balance, rather than demand alone, that is increasingly shaping the narrative around the company.

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.