ARM Holdings (ARM.US) published fiscal-Q4 2024 earnings report yesterday after close of the market session. While results for the January-March 2024 quarter were better-than-expected, fiscal-2025 guidance offered by the company has been seen as somewhat disappointing. This has triggered a post-earnings share price drop in the after-hours trading yesterday, and stock continues to trade around 8% lower in premarket today.

As we have already said in the opening paragraph, fiscal-Q4 2024 results from ARM Holdings were not bad. In fact, they were better-than-expected. Revenue grew more than expected, driven by significant beat in License revenue. ARM said that licensing business revenue performed well due to multiple high-value license agreements for AI chips being signed. Cost of revenue was higher-than-expected, but it was mostly due to higher-than-expected revenues. Gross margin came more or less in-line with expectations. However, other profit measures, including operating income, EBITDA and net income, beat expectations significantly.

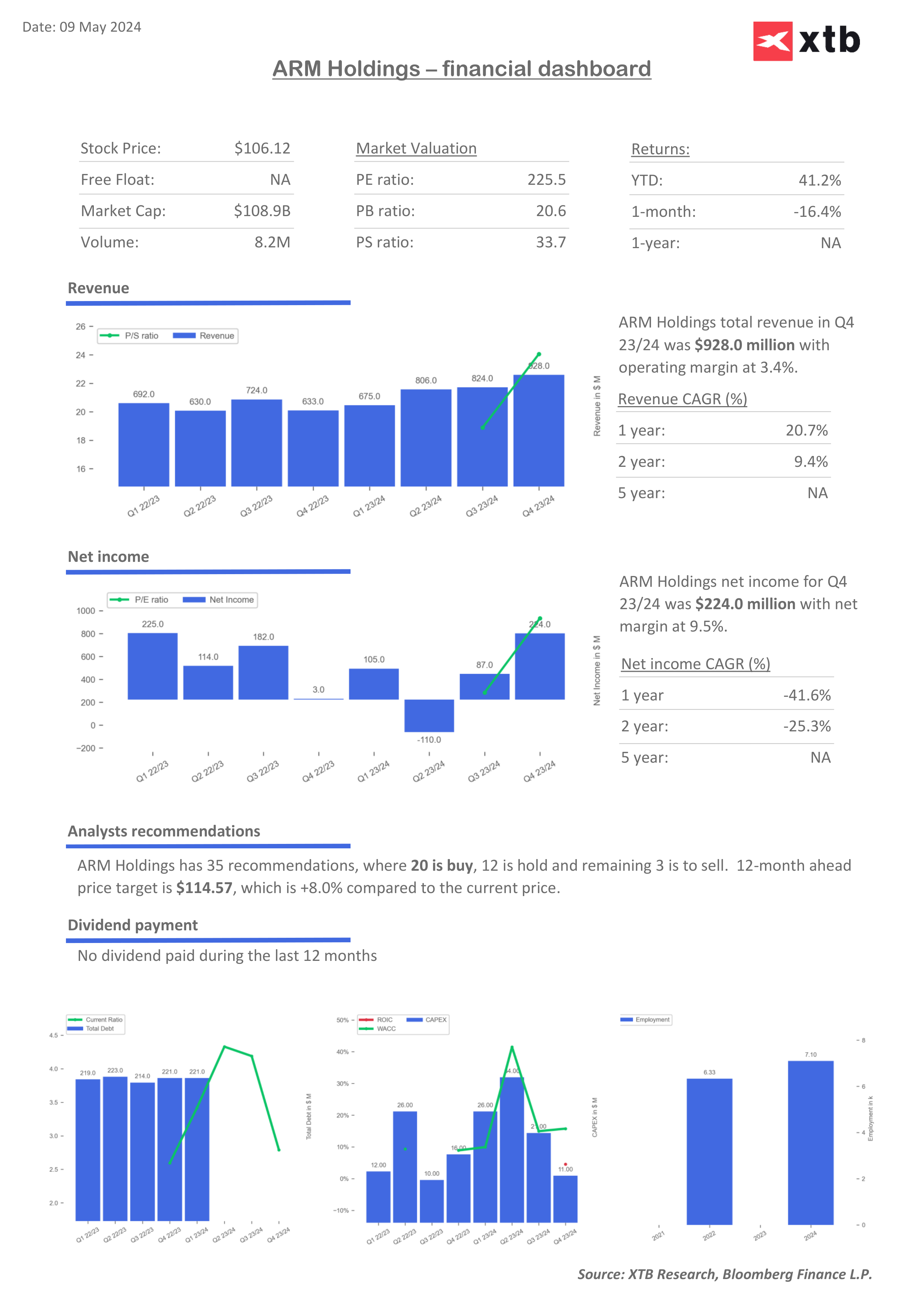

Fiscal-Q4 2024 results

- Revenue: $928 million vs $880.4 million expected (+47% YoY)

- Royalty: $514 million vs $504.2 million expected (+37% YoY)

- License and other: $414 million vs $376 million expected (+60% YoY)

- Cost of revenue: $41 million vs $37 million expected

- Gross profit: $887 million vs $840 million expected

- Gross margin: 95.6% vs 95.7% expected

- Adjusted operating expenses: $511 million vs $490 million expected

- Adjusted operating income: $391 million vs $356 million expected

- Adjusted operating margin: 42.1% vs 40.5% expected

- Adjusted EBITDA: $429 million vs $397 million expected

- Adjusted EBITDA margin: 46.2% vs 45.1% expected

- Adjusted net income: $376 million vs $321 million expected

- Adjusted net margin: 40.5% vs 36.5% expected

- Adjusted EPS: $0.36 vs $0.30 expected

In spite of those better-than-expected results, company's share price dropped in the afterhours trading as guidance offered was seen as disappointing. While fiscal-Q1 2025 forecast (calendar April - June 2024) was better-than-expected with revenue and EPS guidance midpoints exceeding analysts' expectations, a full-year fiscal-2025 guidance disappointed. Full-year revenue guidance midpoint of $3.95 billion was lower than expected, while operating expenses guidance was higher than expected. ARM has a very high valuation - higher P/S ratio than any of the Nasdaq-100 stocks - so the company needed to provide a very outlook not to disappoint investors. However, it looks like it failed to do so.

Fiscal-Q1 2025 guidance

- Revenue: $875-925 million vs $868 million expected

- Adjusted operating expenses: 'about $475 million' vs $478 million expected

- Adjusted EPS: $0.32-0.36 vs $0.31 expected

Full-year fiscal-2025

- Revenue: $3.80-4.10 billion vs $4.01 billion expected

- Adjusted operating expenses: 'about $2.05 billion' vs $2.01 billion expected

- Adjusted EPS: $1.45-1.65 vs $1.53 expected

ARM Holdings (ARM.US) trades 8-9% lower in premarket, following release of fiscal-Q4 2024 earnings report that included disappointed forecasts. Stock is currently trading at around $96.70 in premarket, the lowest level since May 2, 2024. A near-term support zone can be found in the $95 area. Source: xStation5

ARM Holdings (ARM.US) trades 8-9% lower in premarket, following release of fiscal-Q4 2024 earnings report that included disappointed forecasts. Stock is currently trading at around $96.70 in premarket, the lowest level since May 2, 2024. A near-term support zone can be found in the $95 area. Source: xStation5

Daily Summary: A sell-off with a spin-off

US OPEN: The market extends losses as investor concerns grow

Market Wrap: European indices decline amid US - Iran tensions📉 Semiconductors under pressure

Netflix disappoints Wall Street 🚩 Stock drops 9% after disappointing outlook

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.