Key highlights:

- peak rally at 600% (from <100 USD to >700 USD)

- decline of over 70% in two days after the peak

- one-day short seller profits: appx. $2.8 billion

- short interest reaching ~64% of free float

- implied volatility on options: 235%

The starting point: limited supply and mounting pressure on shorts

The story began with a very specific market structure. Avis Budget combined high short interest with a very limited free float. In practice, this meant a large number of investors were positioned for declines, while the actual supply of shares available for purchase remained constrained. This imbalance created ideal conditions for a sharp upward move. Even moderate demand could trigger outsized price reactions due to structurally limited supply.

Ownership concentration as a key catalyst

A critical factor behind the move was the company’s ownership structure. Two hedge funds controlled more than 70% of the shares combined, significantly restricting the free float. In such conditions, relatively small changes in demand can translate into disproportionately large price swings. An additional catalyst came from Pentwater Capital disclosing a large position, which the market interpreted as a signal of institutional backing.

The short squeeze: a self-reinforcing mechanism

As the stock price rose, a classic short squeeze dynamic took hold. Investors betting on declines were forced to close positions, buying back shares at increasingly higher prices. Each forced buyback generated additional demand, further pushing the price higher. At the peak, short interest climbed to around 64% of the free float, amplifying the effect. The takeaway is straightforward: the price surged not because of improving fundamentals, but because the market structure forced participants to buy.

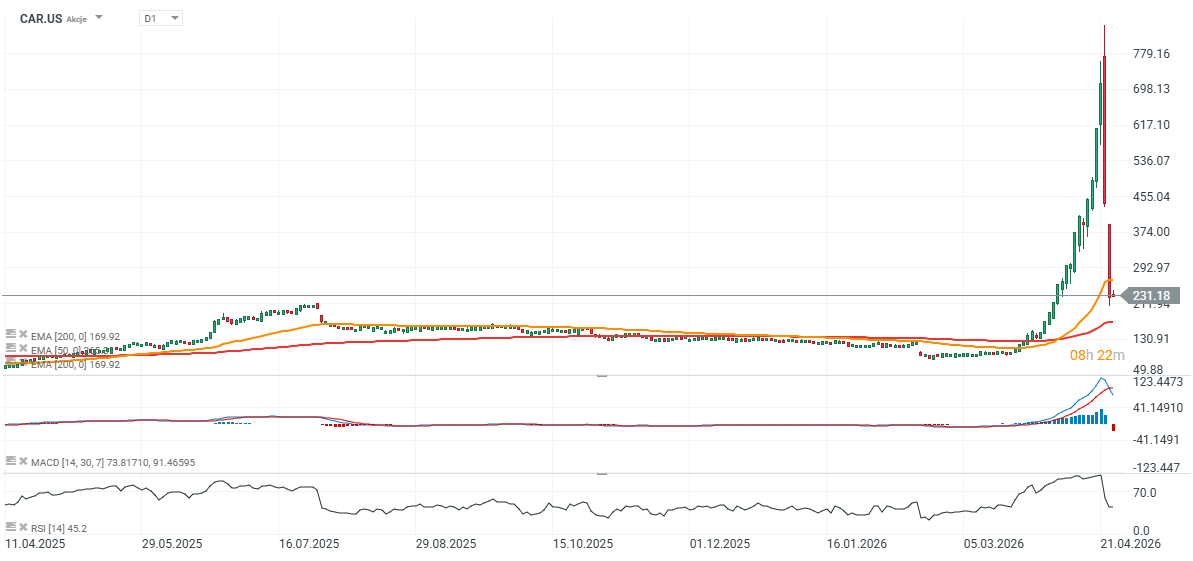

CAR.US (D1 interval)

Source: xStation5

Turning point: the absence of new capital

The reversal began once that mechanism lost momentum. Pressure on short sellers started to ease, while fresh capital inflows failed to materialize. That was enough to break the trend. After peaking above 713 USD, the stock dropped 40% in a single session, followed by further declines in subsequent days. In total, the stock lost more than 70% in a very short period - a typical end to an exhausted short squeeze.

Role reversal: short sellers regain control

The sharp correction completely flipped the market dynamic. Investors who had previously been under pressure began generating profits.

According to S3 Partners, the sell-off produced around $2.8 billion in gains for short sellers in a single day, nearly offsetting earlier losses. At the same time, rising short interest suggests the market quickly returned to positioning for further downside.

Fundamentals in the background: a typical “meme stock” profile

The price action was not supported by improving financial performance. The company has posted net losses in recent years, indicating that the rally was largely disconnected from fundamentals.

This places Avis Budget within the broader “meme stock” category, where price movements are driven primarily by:

- market narrative

- retail investor activity

- market mechanics (short interest, liquidity), rather than earnings

Options activity and volatility: fuel for speculation

Derivatives activity reached levels typical of extreme speculative episodes. Options volume exceeded 200,000 contracts per day, while implied volatility surged to 235%. In response, brokers introduced 100% margin requirements, meaning positions had to be fully cash-funded - a measure reserved for periods of extreme market instability.

Following the surge and subsequent collapse, the market has begun shifting back toward a more fundamentals-driven valuation. This is also reflected in analyst sentiment, which has become increasingly cautious. The episode follows a familiar pattern seen in cases like GameStop or Hertz:

- high short interest

- limited share supply

- influx of speculative capital

- short squeeze

- exhaustion of demand and sharp correction

At present, uncertainty around the stock remains extremely high, and while a near-term rebound cannot be ruled out, the path forward is far less clear than during the peak of the rally.

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

General Motors shares down despite solid earnings report 🚩

TSMC Raises AI Chip Prices. Is the Bill for the Artificial Intelligence Boom Starting to Grow?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.