A strong U.S. dollar and inflation concerns continue to weigh on Bitcoin. While today's U.S. CPI release had little immediate impact on BTC, the recent string of stronger-than-expected labor market data has further pressured sentiment across the cryptocurrency market.

After falling by roughly 50% from its record highs reached in autumn 2025, Bitcoin now appears undervalued according to several key on-chain metrics, including those tracked by Grayscale. Although valuations have not yet reached the deeply discounted levels seen at previous cycle bottoms, there is no guarantee that this cycle will replicate past bear markets one-for-one.

Inflation and regulatory challenges in the U.S.

The regulatory outlook in the United States appears to have deteriorated in recent weeks. Progress on the CLARITY Act, a key piece of legislation for the crypto industry, has slowed, raising doubts about the implementation of a more crypto-friendly regulatory framework.

Uncertainty surrounding the bill could intensify ahead of congressional midterm elections, as Democrats and Republicans continue to hold different views on digital assets. A potential Democratic victory in the midterms could be perceived by parts of the crypto market as a less favorable outcome.

Galaxy Digital recently lowered the probability of the CLARITY Act being passed from 75% to 60%, citing the limited number of Senate working days remaining this year and ongoing controversies surrounding the legislation.

However, the greatest risk to Bitcoin currently appears to be inflation rather than regulation. Persistently elevated inflation does not necessarily increase the likelihood of interest rate hikes, but it significantly reduces the Federal Reserve's room to begin monetary easing. At the beginning of the year, many investors viewed rate cuts as almost inevitable.

The sharp repricing of those expectations has fueled Bitcoin's decline. If tensions in the Middle East persist, elevated oil prices could continue to weigh on risk assets throughout the third and fourth quarters. On the other hand, a peace agreement with Iran could act as a positive catalyst for Bitcoin and broader market sentiment, potentially marking a turning point in momentum.

Bitcoin looks cheap, but could it get cheaper?

During previous cycle bottoms, Bitcoin experienced significantly deeper declines, creating even more attractive opportunities according to on-chain valuation metrics. As a result, the current environment does not yet represent the kind of textbook capitulation phase that has historically marked major market bottoms.

The pandemic-driven sell-off and the collapse of FTX in late 2022 offered much clearer valuation opportunities. At the same time, it is difficult to ignore the fact that investors consistently expected even deeper declines during those periods as well.

While the current market environment does not resemble a classic capitulation event, there is no guarantee that the bottom of this bear market must be formed during a period of extreme panic. Although such an outcome remains possible, there is no certainty that it will ultimately be required to end the ongoing downtrend.

One reason is that Bitcoin's bull market between 2024 and 2026 delivered a relatively smaller gain compared with the bull cycles of 2017 and 2021. Consequently, the current correction may also prove shallower.

In addition, despite the severe sell-off—particularly across altcoins—the industry does not currently appear vulnerable to the type of "black swan" events seen during the collapse of Terra/Luna and FTX in 2022. Much of the excess leverage and risk was flushed out of the market several years ago, leaving the ecosystem in arguably healthier condition today.

Strategy continues to accumulate Bitcoin aggressively, but the company maintains sufficient operating liquidity and is not expected to face significant debt repayment obligations until 2028 and 2029. If Strategy were eventually forced to sell Bitcoin and trigger another major market decline, it would imply the longest bear market in crypto history and effectively break the traditional four-year halving cycle.

Meanwhile, spot Bitcoin ETFs, which did not exist in previous cycles, may help cushion downside pressure. Net ETF flows have remained strongly positive since launch, providing a structural source of demand.

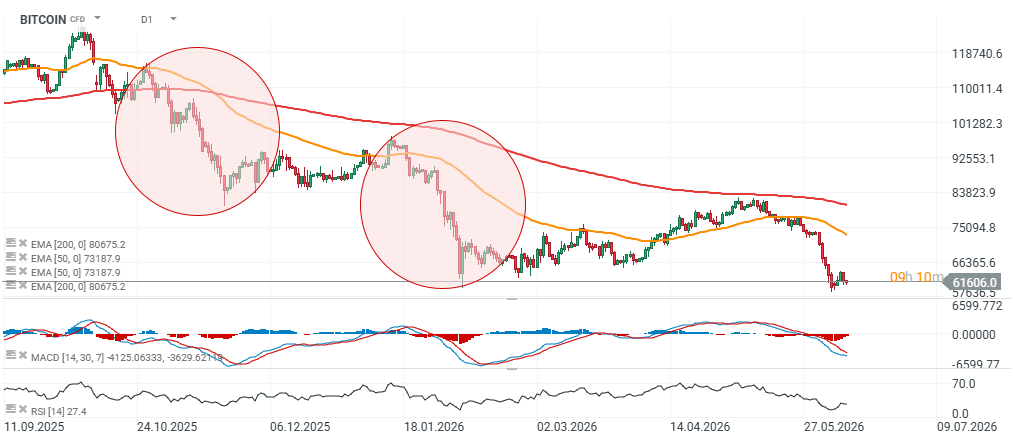

Bitcoin technical outlook (D1)

From a technical perspective, Bitcoin has now experienced its third major downward impulse since autumn 2025. The previous two sell-offs were similar in magnitude. If history were to repeat itself, the next significant support zone could emerge around $55,000.

Source: xStation5

Eryk Szmyd Financial Markets Analyst, XTB

Bitcoin Climbs Above $66,000 as ETF Flows Recover but Glassnode Warns of Higher Volatility

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

Silver breaks above $59 and attracts capital again. Gold remains in the shadow of its younger sibling

Chart of the day 🔼Nasdaq gains 1.2% as semiconductors rebound (21.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.