-

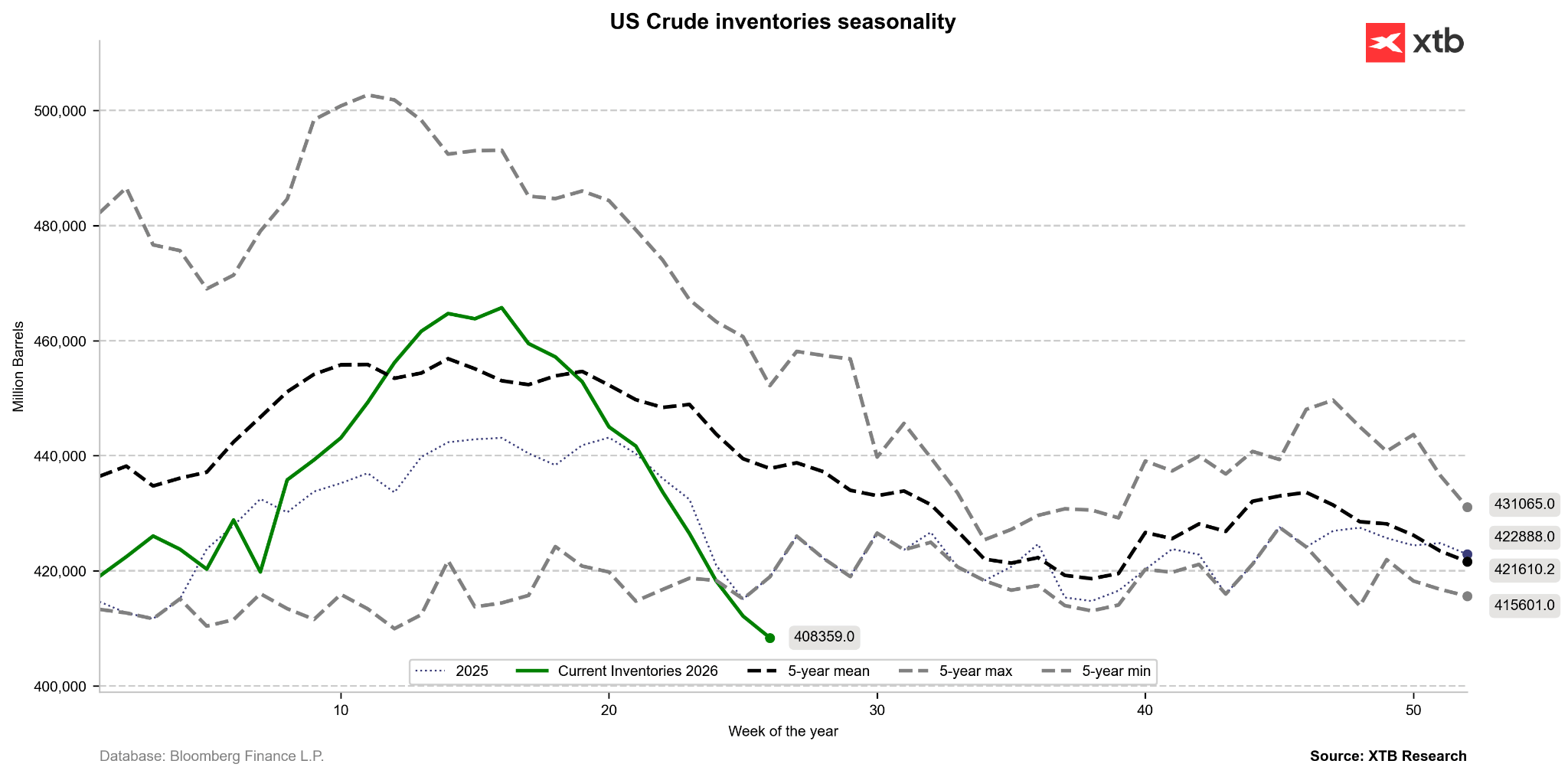

Crude Oil Inventories: Decrease by 3.775 million barrels. This result is slightly better than the assumed 4 million barrels, but better than the previous week, when inventories fell by almost 6.1 million barrels. Total inventory stands currently at 408.359 million barrels (a decline of 0.92%).

-

Gasoline Inventories: Decrease by 2.33 million barrels (a decline of 1.08%). A decline of 0.9 million barrels was expected, and previously we had an increase of 2.06 million barrels.

-

Distillate Inventories: Increase by 2.48 million barrels (an increase of 2.34%). A decline of 0.8 million barrels was expected, with a previous increase of 3.06 million barrels.

-

Cushing Hub Inventories: Increase by 709 thousand barrels (to the level of 19.666 million barrels). This mitigates recent concerns that inventories at the hub would fall to a critical level.

-

Refinery Utilization: Increase of 0.50% week-over-week.

-

US Crude Imports: Decrease by 291 thousand barrels per day (bpd) to the level of 5.279 million bpd.

Commentary on the data

Today's EIA report has a rather positive impact on prices, however, we are currently still observing declines in the oil market, due to continued positive sentiment regarding the opening of the Strait of Hormuz. What is worth noting in the report?

- Strong demand and pressure on crude oil inventory decline: A key point of the report is the continued decline in crude oil inventories (-3.775 million barrels). This decline was stimulated by two factors: an increase in activity of US refineries (an increase in utilization of 0.50%) and a lower inflow of raw material from abroad (imports fell by almost 300 thousand barrels per day). The main burden of the declines was taken by the Gulf Coast region, which is the heart of the American refining industry.

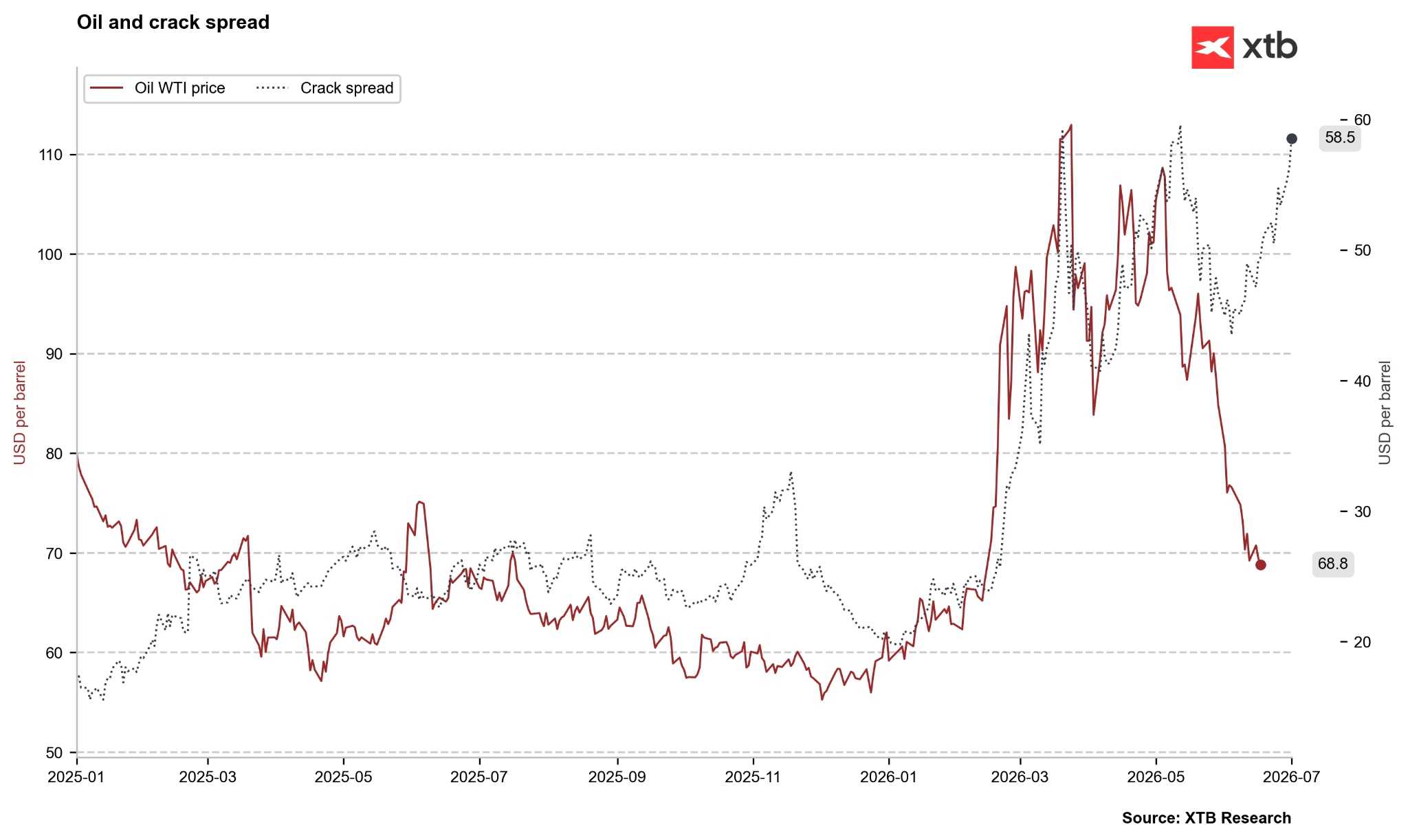

- Fuel market (Gasoline vs. Distillates): A very positive signal for consumer demand is the solid decline in gasoline inventories (by 2.33 million barrels), which suggests a strong travel season. On the other hand, market optimism is being hampered by an unexpectedly large increase in distillate inventories (diesel, heating oil) by nearly 2.5 million barrels, which may indicate a slight slowdown in the industrial or heavy transport sector. It is worth noting that crack spreads in the market remain at a high level.

- Cushing Hub: A slight bearish factor is also the increase in inventories at the key Cushing settlement hub by 709 thousand barrels, which shows that the physical availability of oil at the WTI futures delivery point has improved slightly.

Inventories continue a deep pullback. We are also observing a further decline in SPR. Source: Bloomberg Finance LP, XTB

Inventories continue a deep pullback. We are also observing a further decline in SPR. Source: Bloomberg Finance LP, XTB

The Crack Spread is already reaching recent local highs, which may suggest high demand for fuel or a shortage. Such large divergences are extremely rare. Source: Bloomberg Finance LP, XTB

The Crack Spread is already reaching recent local highs, which may suggest high demand for fuel or a shortage. Such large divergences are extremely rare. Source: Bloomberg Finance LP, XTB

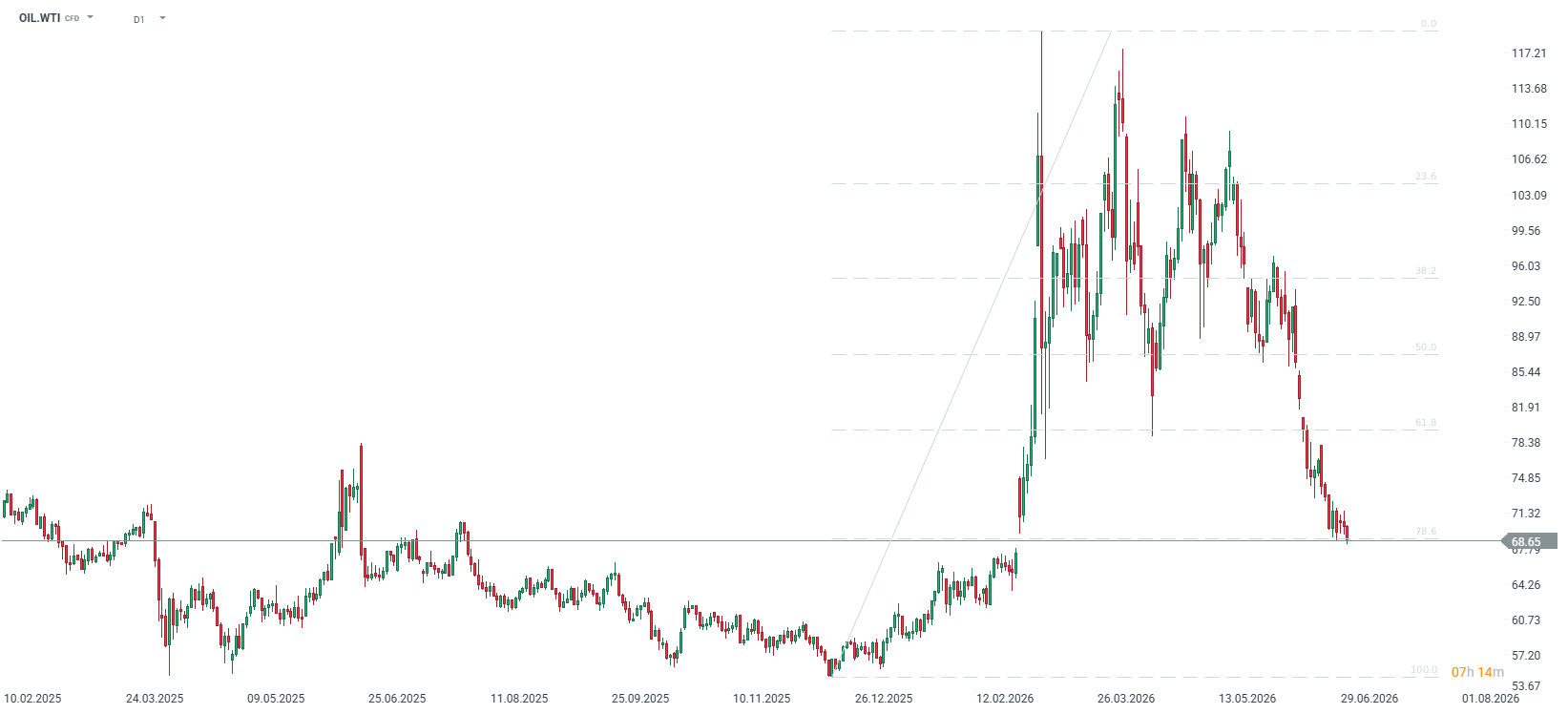

WTI crude oil is falling today to a new low since the beginning of the war, finding itself just 1.5% above the February close. Source: xStation5

WTI crude oil is falling today to a new low since the beginning of the war, finding itself just 1.5% above the February close. Source: xStation5

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.