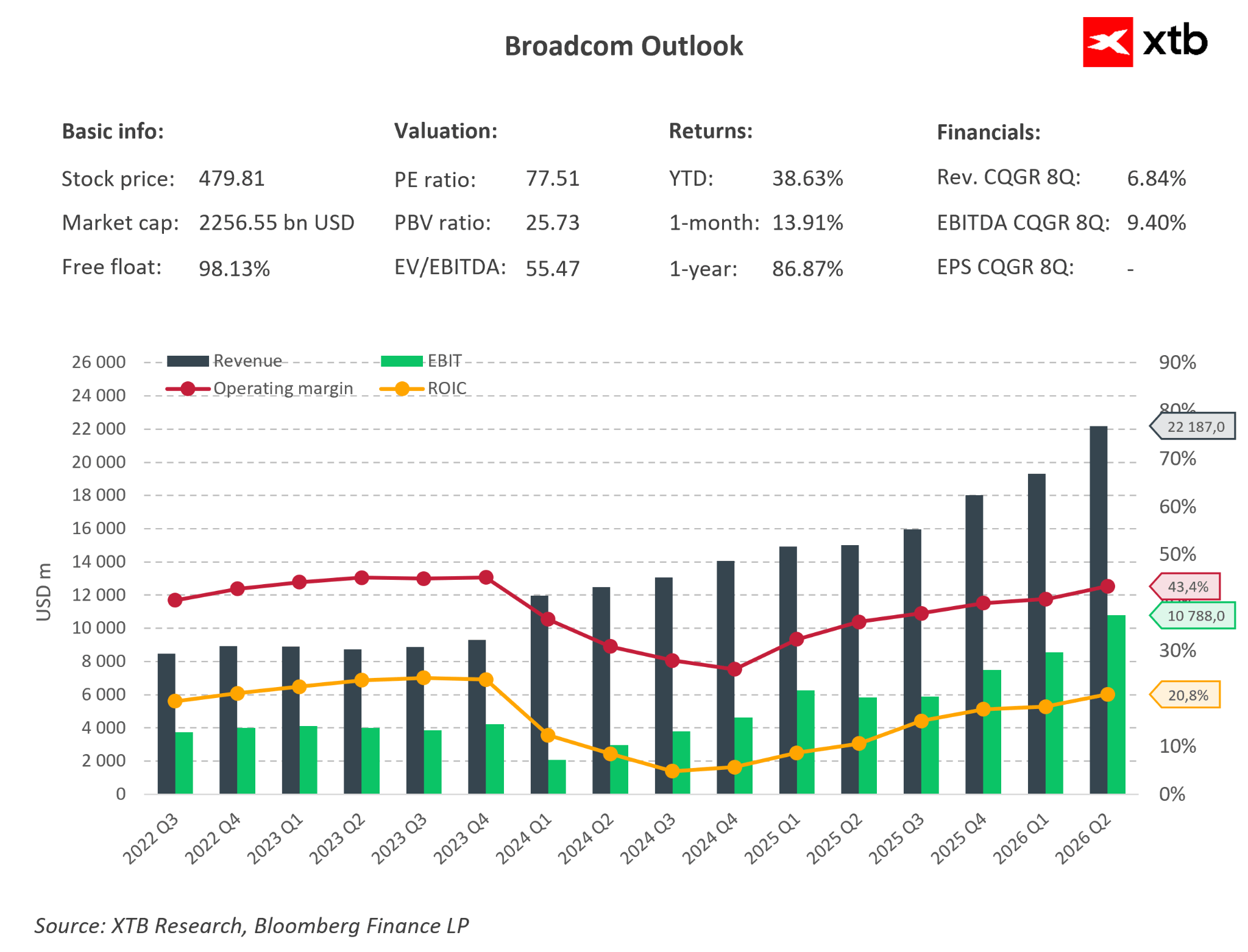

Strong financial results driven by AI

Broadcom reported very strong results for the second quarter of fiscal 2026, confirming that it remains one of the main beneficiaries of the boom in AI infrastructure. The company’s revenue rose 48% y/y to USD 22.19 billion, slightly above consensus, while adjusted EPS came in at USD 2.44 versus expectations of USD 2.40.

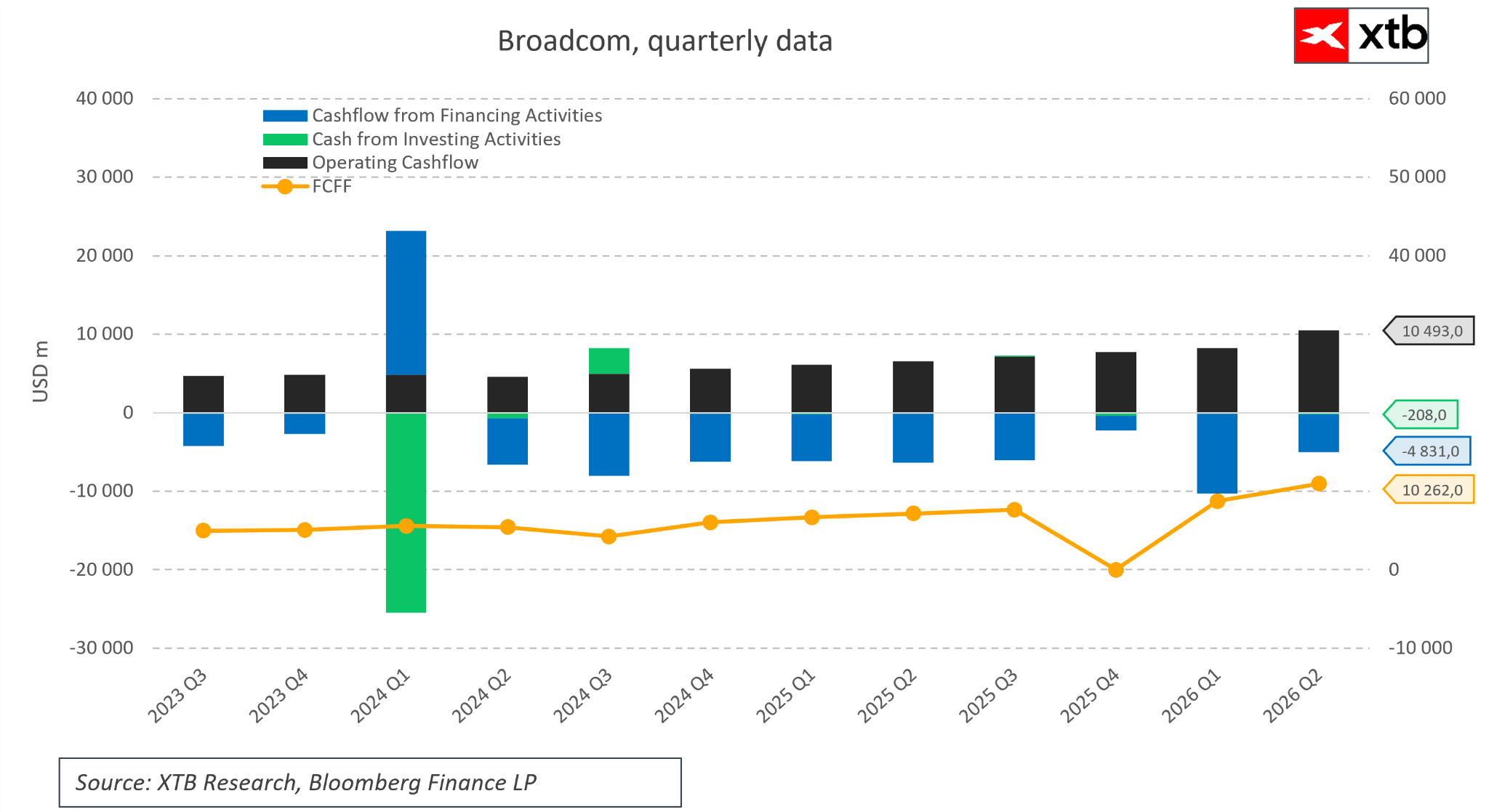

The cash flow side looked particularly strong: free cash flow increased 60% y/y to USD 10.26 billion, equivalent to as much as 46% of revenue. The key growth driver was the semiconductor segment, where revenue rose 79% y/y to USD 15.0 billion, including AI chip sales, which increased 143% y/y to a record USD 10.8 billion. The weaker point in the report was the infrastructure software segment, which grew 9% y/y to USD 7.18 billion, but came in slightly below unofficial, elevated market expectations.

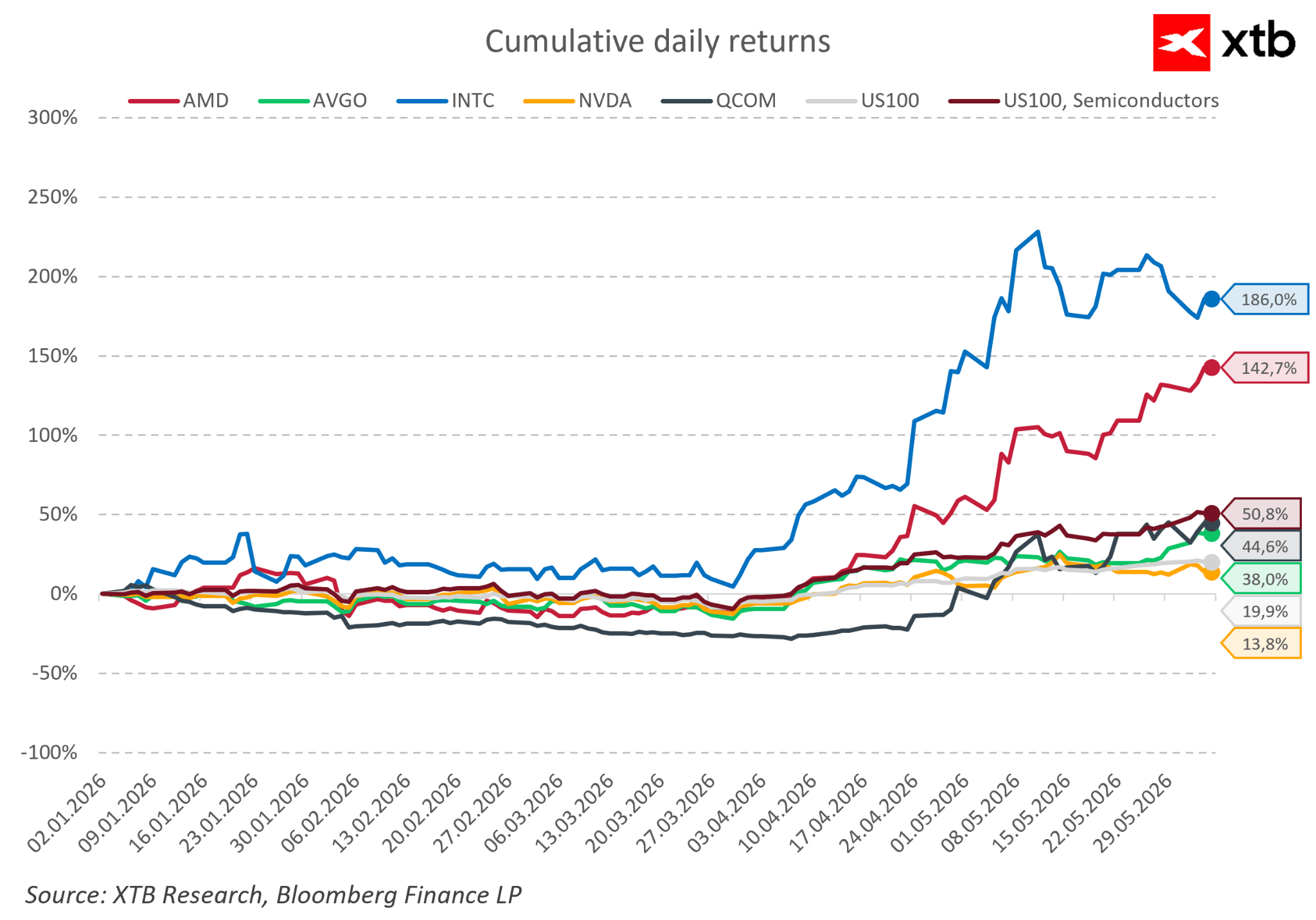

Broadcom compared with competitors

Compared with major semiconductor companies, Broadcom looks solid, although it is not the leader in year-to-date returns. Since the beginning of the year, AVGO shares have gained around 38%, although this figure does not yet include the nearly 13% decline in after-hours trading following the quarterly results. For comparison, the US100 has risen by around 20%.

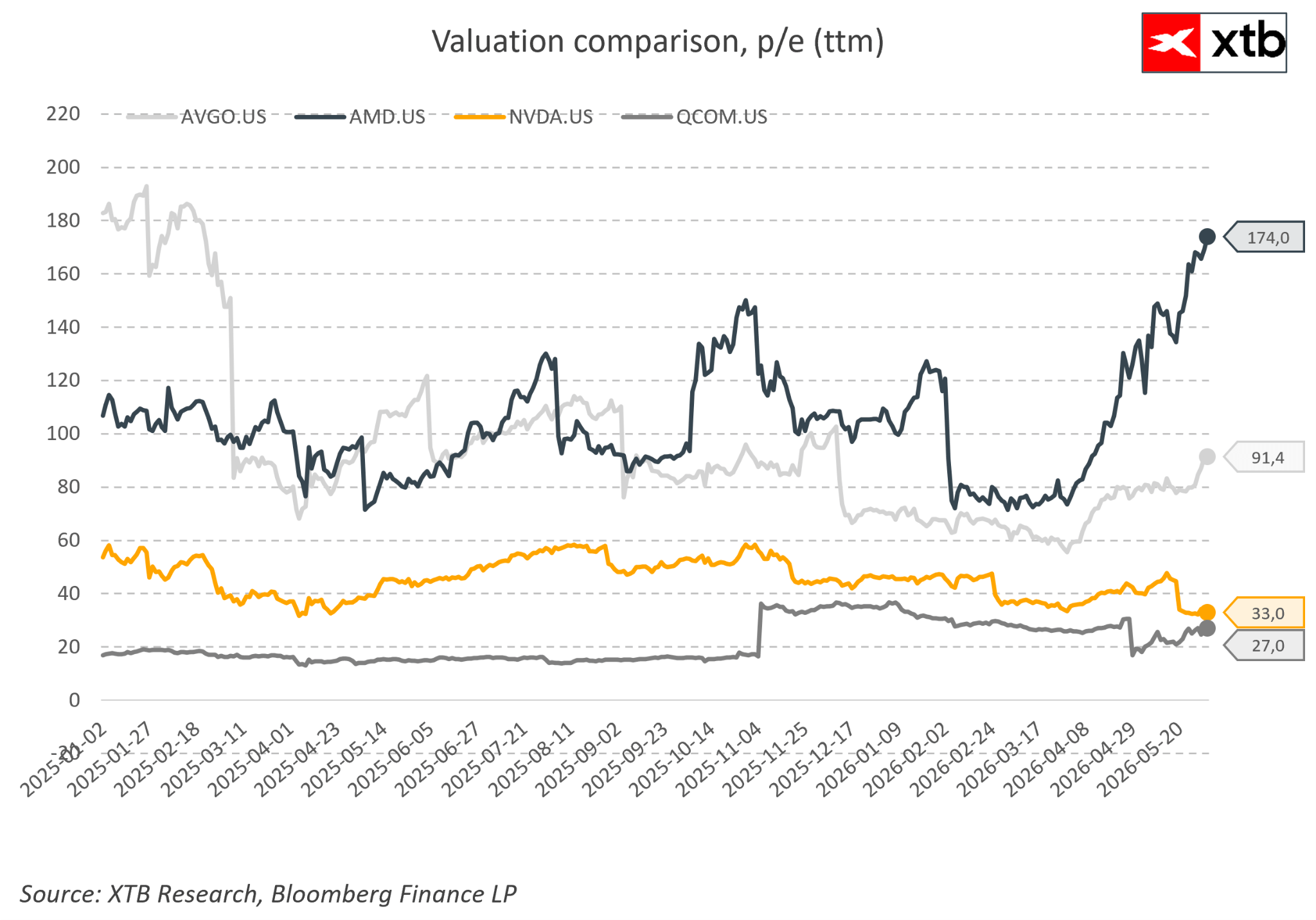

Broadcom’s valuation remains demanding

Broadcom trades at a clear premium to some of its competitors — AVGO’s TTM P/E ratio stands at around 91x, significantly higher than in the case of Nvidia and Qualcomm. AMD is the exception here. This is an important context for the reaction after the results: even a very strong financial report and high guidance may not be enough if the market had already priced in a very optimistic scenario beforehand.

Management highlights record demand for AI chips

Management’s commentary was clearly optimistic, especially in the area of AI. CEO Hock Tan emphasized very strong demand for custom AI chips. New AI chip orders in the quarter exceeded USD 30 billion, significantly above the actual sales delivered during the period. Management also pointed to the high value of shipments and production capacity secured through 2028. Broadcom confirmed strategic relationships with the largest technology clients, including Google, Anthropic, OpenAI and Meta, as well as its participation in the AI XPV platform, which aims to finance and deploy large-scale computing capacity for AI laboratories.

An important part of the message was also the emphasis that Broadcom does not intend to compete in the ready-made server rack segment, but instead focuses on the most specialized and margin-rich part of the value chain: ASICs, XPUs and networking solutions.

The outlook remains strong, but the valuation leaves no room for error

The outlook presented by the company remains very strong, although the market reaction showed that expectations for Broadcom were already extremely high. For the third quarter of FY2026, the company forecasts revenue of around USD 29.4 billion, above the previous consensus, with an adjusted operating margin of around 67%. Key assumptions include:

- around USD 20.5 billion in semiconductor revenue,

- around USD 16.0 billion in AI semiconductor revenue, representing growth of more than 200% y/y,

- around USD 8.9 billion in infrastructure software revenue,

- maintaining the annual AI chip revenue forecast for FY2026 at USD 56 billion and the target of exceeding USD 100 billion in FY2027.

Despite the very strong results, Broadcom shares fell almost 13% in after-hours trading, which can be interpreted more as the result of profit-taking and overly high expectations than a deterioration in the company’s fundamentals. The market reacted negatively, among other things, to the slight disappointment in the software segment, the lack of an upgrade to the long-term AI forecast for FY2027, and the clear reduction in share buybacks compared with the previous quarter.

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Hormuz Deal Moves Closer

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.