The Persian Gulf states are accelerating the construction of pipelines and ports and are outdoing one another with new ideas for bypassing the Strait of Hormuz. The projects are technically and financially feasible, but they will not solve the current crisis.

Even if work started immediately, a meaningful increase in alternative export capacity would likely come in 2027, while a more thorough reconfiguration of the regional system would take until the end of the decade.

While oil and other fuels can benefit from existing and future alternative routes, Qatari LNG remains cut off from markets, and prospects for alternative export corridors are limited.

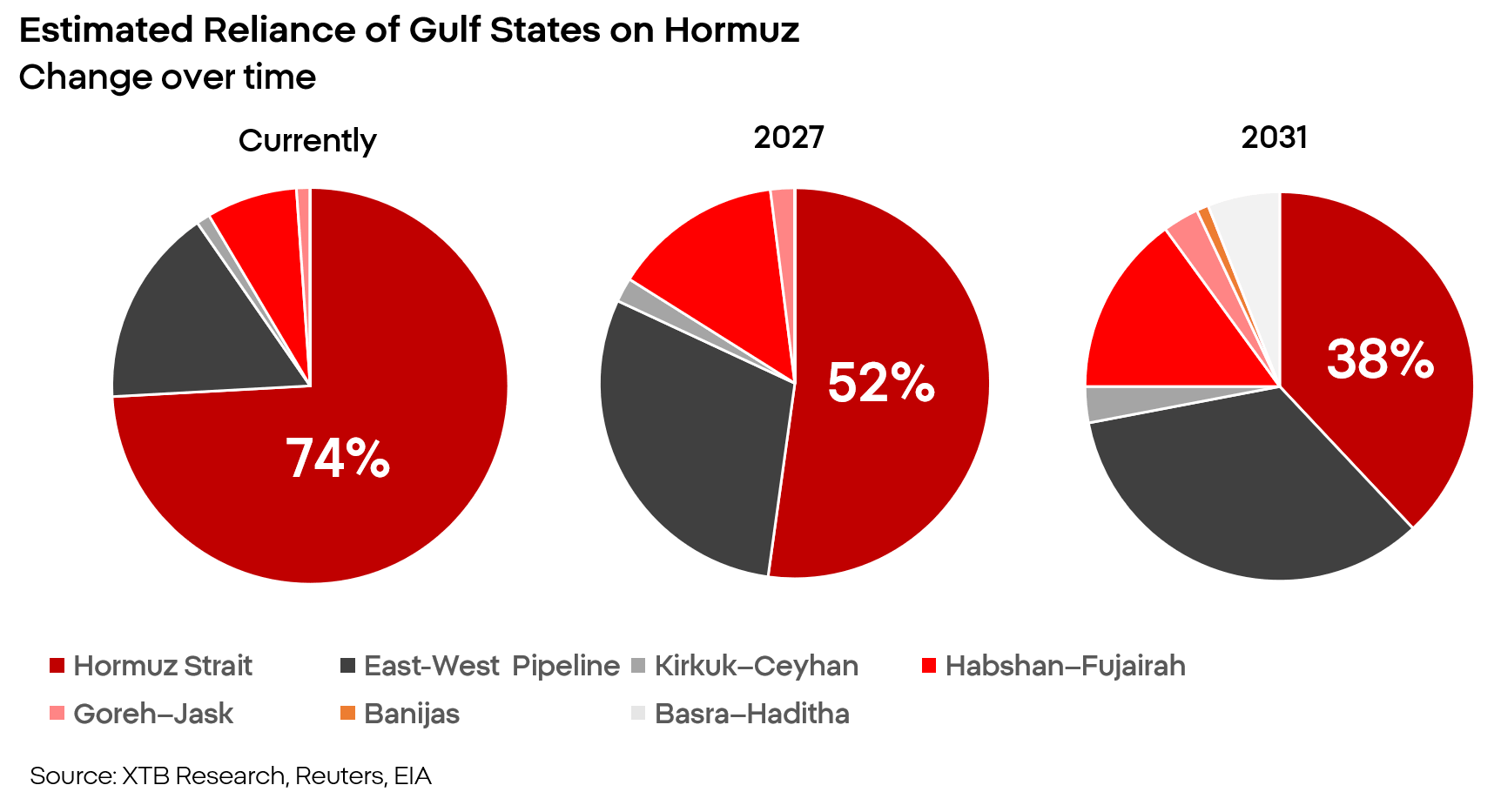

At present, only Saudi Arabia and the United Arab Emirates have large, operational export routes that bypass Hormuz. Their combined capacity is about 6 to 7 million barrels per day. This helps ease the supply shock but does not solve the problem.

Even with a complete closure of the Strait of Hormuz, alternative routes remain that, with varying effectiveness, can move roughly 40% of exports from the Persian Gulf. In practical terms, that means that of the roughly 20 to 30% of global fuel or fertilizer supply previously provided by Gulf countries, only about 15% has disappeared from the market. This is still unfavorable, but not as critical as it might seem.

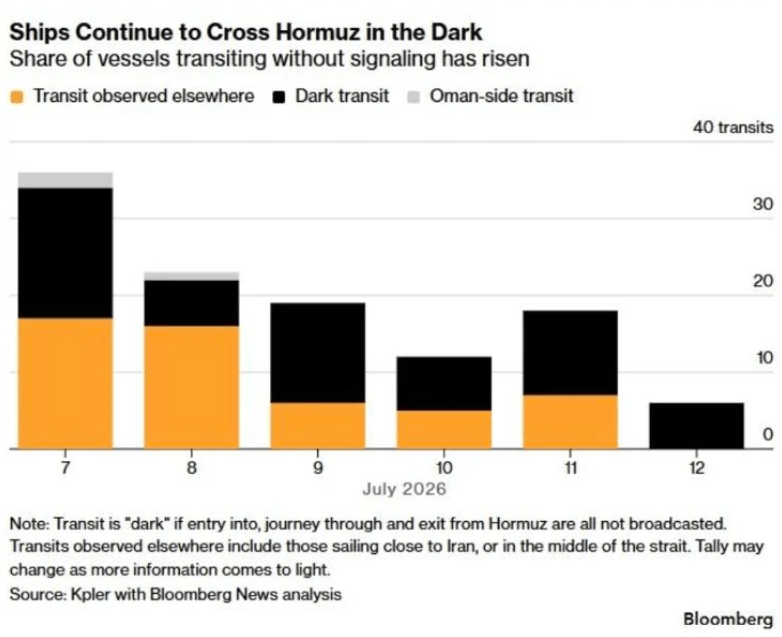

It is also worth adding that the Strait of Hormuz is never “fully” closed. Iranian methods of attacking ships remain very crude, which, combined with exploding freight rates, means some captains choose to break the blockade and risk coming under fire.

However, a scenario of a prolonged war with Iran is becoming increasingly likely. If it materializes, the Persian Gulf countries cannot afford to rely on risky maritime maneuvers and overburdened alternative routes.

What is needed are huge, expensive, ambitious projects capable of truly shifting the regional balance of power, and quickly. The Persian Gulf may be one of the places where such projects have the best chance of succeeding.

The UAE closest to a real breakthrough

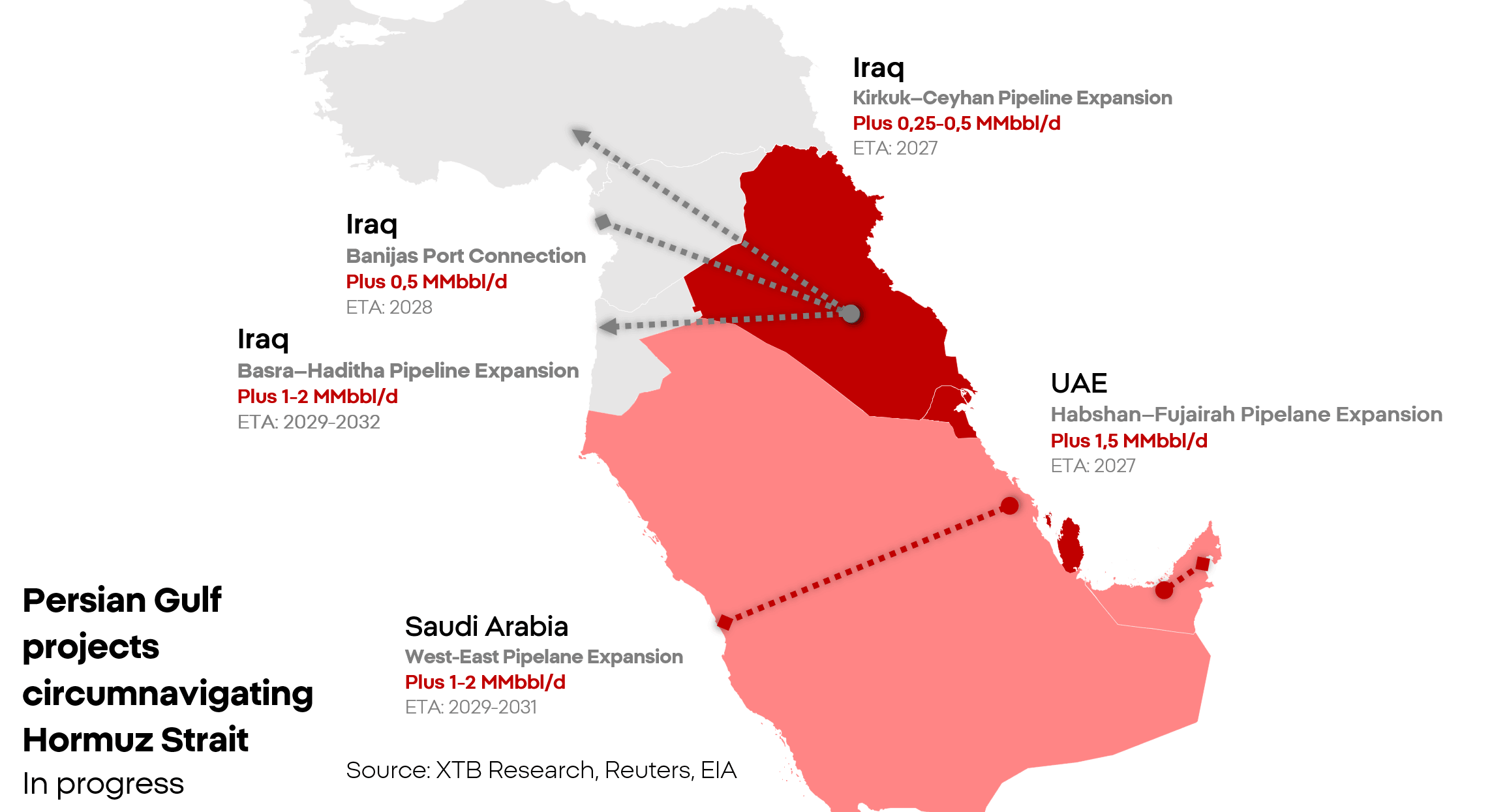

The most advanced project is being carried out by the United Arab Emirates. The existing Habshan–Fujairah pipeline can transport around 1.5 to 2 million barrels per day from oil fields to a port located outside the strait. A second line now under construction is intended to nearly double that throughput. In May, ADNOC reported that the investment was “around 50%” complete. Full operation is planned as early as 2027.

This is the most straightforward and easiest of the projects proposed in the region. An additional roughly 1.5 million barrels per day is a lot and would materially improve the supply situation, but the port remains within range of Iranian missiles and drones, which could affect throughput in the future.

The UAE is also planning a pipeline for gasoline, diesel, and jet fuel, as well as port expansion on the east coast. The authorities are fairly confident and are already talking about reducing dependence on Hormuz to zero. These ambitions should not be misunderstood: bypassing the Strait of Hormuz in Middle Eastern conditions is feasible and economically viable, and the only open question is the time horizon. Cutting off dependence on the Strait of Hormuz for the UAE is a matter of years, not quarters.

East-West

Saudi Arabia has the East-West pipeline linking eastern oil fields with the port of Yanbu on the Red Sea. It is the most important alternative to Hormuz, with nominal capacity around 7 million barrels per day, though in practice it is about 4 to 5 million.

Riyadh is considering increasing the system’s capacity by 1 to 2 million barrels per day. However, this is a project on a different scale. The East-West pipeline is well over a thousand kilometers long and runs through the middle of the Arabian Desert, one of the most inhospitable regions on Earth. A realistic timeline for completing capacity expansion in this direction is between 2029 and 2031.

This route is not free of kinetic risk either. In neighboring Yemen, the Houthis operate and, in cooperation with Iran, seek to threaten commercial shipping through the Red Sea and the Gulf of Aden. The Houthi threat is significant, but still an order of magnitude smaller than that posed by Iran. Given Iran’s blockade, the group may face growing difficulties in sustaining operations.

The difficult situation of Iraq and Kuwait

Where discomfort turns into outright desperation is Iraq and Kuwait. Kuwait has no independent export route that bypasses Hormuz. During the blockade, the country cut production to domestic-market needs and terminated contracts, invoking a force majeure clause.

Iraq is in a better position because it has some alternatives, but none can quickly replace the ports in Basra. The Kirkuk–Ceyhan pipeline to Turkey has a nominal capacity close to 1.5 million barrels per day, but actual utilization remains low. Technical and political issues stand in the way.

Iraq exports about 50,000 barrels per day by road transport. This is a lifeline for the state budget, but the volume is microscopic at the scale of the market. The country has begun construction of the Basra–Haditha trunk line with a designed capacity of 2.5 million barrels. However, Haditha lies deep inland. Full export would require further connection to Turkey, Syria, or Jordan.

The real market impact of this investment is therefore possible no earlier than around 2029, with a fuller effect only in 2030 to 2032.

Qatar without alternatives

Qatar’s situation is the most difficult. Qatar chose an ambitious strategy of specializing in natural gas exports to secure a better market position and higher margins. Until the outbreak of the war between the US and Iran, this strategy worked very well. Now, however, it is becoming a massive burden.

A gas pipeline to the Red Sea, Oman, or Fujairah would not be enough to replace current terminals. On the new coastline, gas processing and liquefaction facilities would need to be built, along with cryogenic storage tanks and a terminal for specialized vessels. This kind of investment would be far more expensive and time-consuming than standard infrastructure. At present, all initiatives remain at the planning stage.

Balance

- By the end of 2026, capacity increases, even in the best-case scenario, will be negligible.

- In the second half of 2027, additional capacity could be higher by about 1.5 to 3 million barrels per day.

- A true “revolution” may only come in the 2028 to 2030 window, with a realistic increase in non-Hormuz capacity of 6 million barrels per day.

The Gulf states’ messaging therefore indicates genuine concern, which in itself can be treated as a sign that the campaign in Iran is not close to ending.

Pressure is not evenly distributed:

- Saudi Arabia and the UAE are pursuing a long-term strategy of resilience against Iranian attacks.

- Qatar is still analyzing its options.

- Kuwait and Iraq, meanwhile, are fighting for survival.

Kamil Szczepański

Financial Market Analyst at XTB

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

BREAKING: BoE Keeps Rates Unchanged

🛢️Further escalation and tense situation do not drive oil further

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.