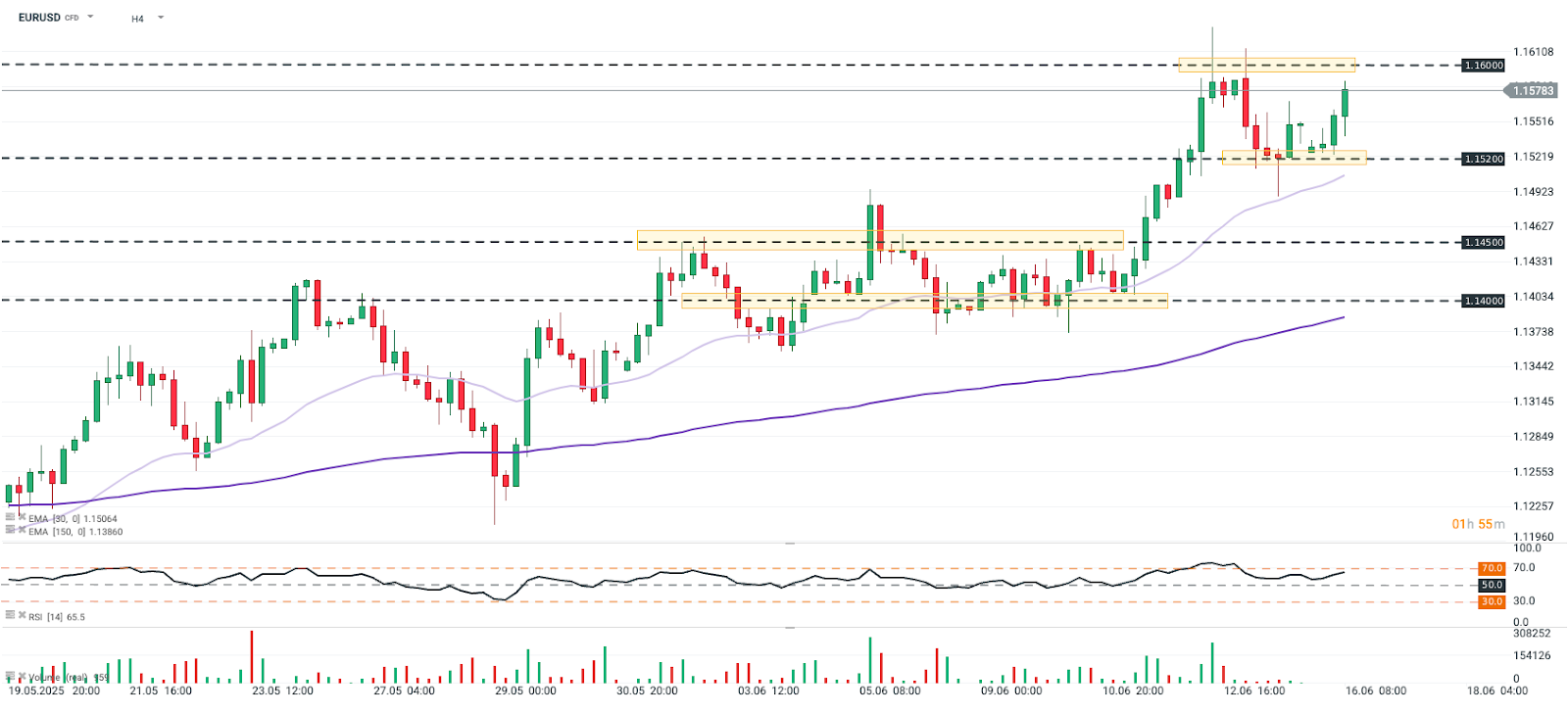

EURUSD reapproaches key resistance near 1.16 despite speculated options market correction and higher U.S. interest rates. However, the European Central Bank (ECB) has indicated that a strong euro is not a concern, and new geopolitical fundamentals may point to a continuation of the bullish sentiment toward the world’s second most traded currency.

Source: xStation5

ECB vs. the Risk Balance

The escalation of conflict in the Middle East is forcing the European Central Bank (ECB) to revisit its economic outlook. Since the beginning of the year, Eurozone policymakers have been more worried about deflation than inflation, which in some economies has dropped below target primarily due to falling energy prices. Current upward pressure on oil prices and uncertainty around supply chains could support higher global energy prices while also posing a risk to European industrial output.

In light of these emerging risks, ECB members are calling for greater flexibility. Bundesbank President Joachim Nagel emphasized today that, with such rapidly changing conditions, it is unwise to get used to the "mission accomplished" on inflation. Meanwhile, according to Luis de Guindos, the inflation risk balance in the Eurozone remains broadly even, although in the medium term, tariff-related issues could weigh on both economic growth and inflation. De Guindos also stated that an exchange rate around 1.15 is not problematic for monetary policy and that he does not expect the euro to appreciate sharply in the near term.

New Fundamentals on the Horizon

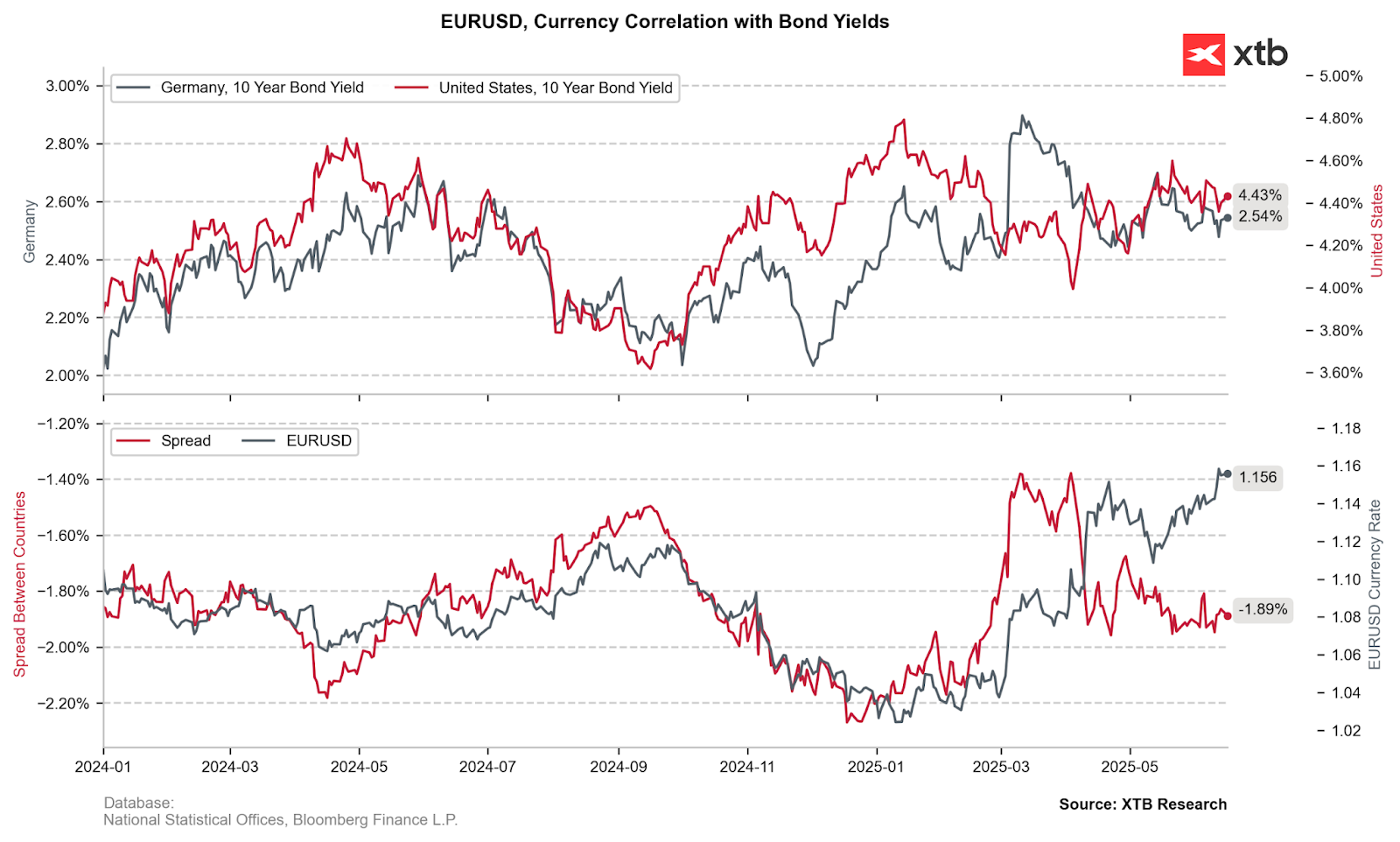

The yield spread between German and U.S. 10-year bonds remains steady despite the recent rise in EUR/USD. While monetary factors might suggest that the euro is overvalued, a closer look at other fundamentals offers the world’s second-largest currency some room for further appreciation. Recent geopolitical turbulence has increased capital flows into safe-haven currencies, with the euro benefiting from controlled inflation, prospects of economic recovery, and institutional stability.

Moreover, the market may overreact to any dovish signals from Jerome Powell following Wednesday’s interest rate decision. Even though no rate cut is expected at the upcoming meeting, the Federal Reserve is under pressure to lay its cards on the table and address lower-than-expected inflation and the mixed signals from the labor market. A relatively dovish dot plot could therefore push the yield spread back toward current highs in EUR/USD.

Source: XTB Research

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Tensions around Iran weigh on markets!

US Open: Alphabet and Tesla Weigh on Wall Street, While Oil Prices Renew Investor Concerns

Wheat climbs to the highest level since May 2024 🚜 Black Sea export risks fuel rally

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.