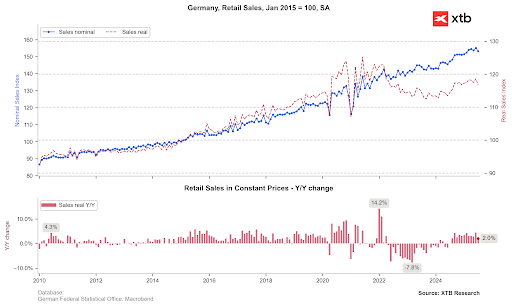

EURUSD began today's session with a degree of weakness, following the release of poor German retail sales data and lower producer inflation (or rather, deflation). German retail sales fell by 1.5% month-on-month and rose by only 2.0% year-on-year, a significant slowdown from the nearly 5% growth seen in June. Such weak data undermines the narrative of a robust European consumer.

Additionally, data from France and Spain was released. French inflation remains extremely low at 0.9% year-on-year, although it did see a monthly increase of 0.4%. In Spain, CPI inflation remains elevated at 2.7% year-on-year but failed to rise as expected to 2.8%.

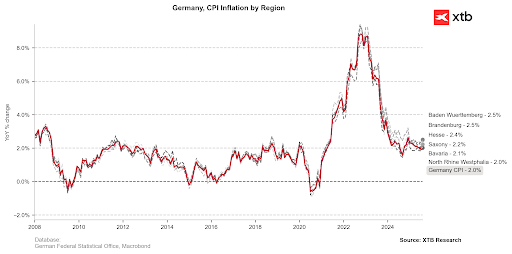

However, we have seen a significant surprise from individual German states, where data has come in notably above expectations, suggesting a considerable rebound in August's CPI inflation. These figures will be released in the early afternoon. For instance, inflation in Brandenburg rose to 2.5% year-on-year from a previous reading of 2.2%. Almost all states saw inflation come in higher than previous levels, though there were virtually no month-on-month changes after the last strong rebound.

Expectations for German inflation point to a rebound to 2.1% year-on-year from 2.0%, with a month-on-month reading of 0.0%. However, there is room for an upside surprise, which should reinforce the ECB's stance to hold interest rates at its upcoming meetings.

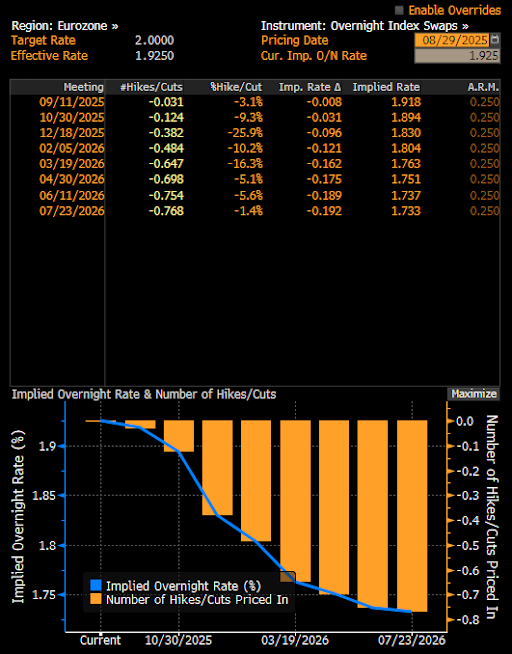

Expectations indicate an almost zero probability of a rate change at the September meeting. For December, the market is pricing in just under a 40% probability. Source: Bloomberg Finance LP, XTB

EURUSD has recovered almost all of its morning weakness thanks to the higher data from the German states. It is worth noting that the pair has reacted to the 1.1600 level four times in recent weeks. Nonetheless, at 1:30 PM BST today, we will see the US PCE inflation data, which could set a new tone for the pair. If inflation proves to be higher than expected, it could temper the strong market expectations (85%) for a Fed rate cut in September. Conversely, if it turns out that tariffs do not have as much of an impact on consumer prices as some Fed members have suggested, confidence in a September move could increase. This might encourage the pair to re-test the 1.17 level, which marks the upper boundary of the descending trend channel.

Wheat climbs to the highest level since May 2024 🚜 Black Sea export risks fuel rally

Oil rises over 3% 🛢️

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Morning Wrap: A New Threat of Conflict in the Middle East 🚨 (23.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.