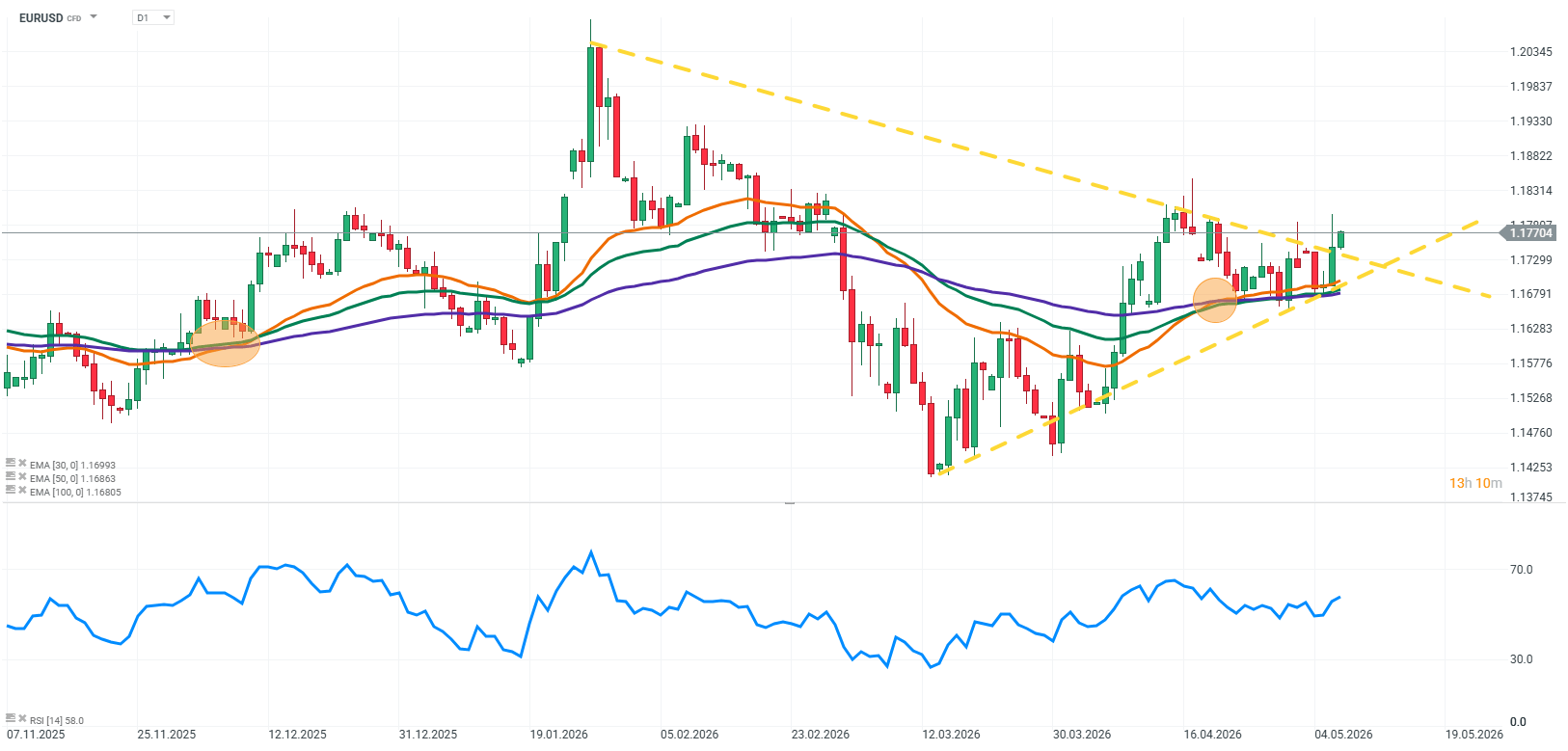

In today’s session, EUR/USD is strengthening around the 1.17 area, but the move is not driven by a single dominant factor. Instead, it reflects a combination of several parallel impulses, including unchanged policy rates from both the Fed and the ECB, improving sentiment linked to potential de-escalation of tensions around Iran, and stronger-than-expected German industrial data. It is important to stress that the current appreciation looks more like a repricing of expectations than a durable shift in underlying fundamentals.

Source: xStation5

What is shaping EUR/USD price action?

Fed on hold, but the market is already pricing rate cuts

The Federal Reserve kept interest rates unchanged, while signalling a gradual slowdown in economic momentum and increasing sensitivity in the labour market. At the same time, inflation in the US is still not fully under control, particularly in services and core inflation, where price pressures remain persistent. Despite this, markets are increasingly pricing in future rate cuts, not as a response to rapidly falling inflation, but rather as a reaction to a potential weakening in economic activity. This scenario reduces the attractiveness of the US dollar and gradually supports EUR/USD through expectations of a narrowing interest rate differential.

The ECB remains cautious, with no automatic path to hikes

The European Central Bank also left rates unchanged, maintaining a cautious and data-dependent communication stance. While some forecasts still allow for further tightening, the dominant view remains one of stabilisation and inflation-driven decisions rather than an aggressive hiking cycle. At the same time, improving real economy data, especially from Germany, is limiting earlier expectations of a deeper slowdown in the euro area, supporting the single currency through the activity channel rather than monetary policy expectations alone.

Geopolitics and hopes for an Iran agreement

Reports of potential de-escalation in tensions surrounding Iran are improving global risk sentiment. A decline in the geopolitical risk premium reduces demand for the US dollar as a traditional safe-haven currency, while benefiting risk-sensitive assets such as the euro. In addition, a potential easing of tensions in the Middle East lowers pressure on energy prices, which in the medium term could reduce inflationary pressures and strengthen expectations of a more accommodative Fed stance.

Germany surprises to the upside, lifting European sentiment

Stronger-than-expected German industrial data is an important element of today’s market picture. Against the backdrop of earlier concerns about stagnation in Europe, this release is helping stabilise perceptions of the euro area. As a result, the euro is increasingly seen not only through the lens of cyclical weakness, but also as a relatively stable alternative to the US dollar, particularly in an environment of shifting monetary policy expectations.

What else is influencing the market in the background

Beyond central bank decisions and macroeconomic data, the key driver remains the pace of change in market expectations regarding future Fed and ECB policy. The market is currently in a repricing phase rather than a full economic cycle shift. This makes EUR/USD particularly sensitive to incoming data and central bank communication that could either confirm or challenge the scenario of faster US easing combined with relatively stable policy in Europe. In such an environment, even moderately positive European data can support the euro in the short term, but the sustainability of the trend will ultimately depend on whether the Fed actually moves towards more decisive monetary easing.

Economic Calendar: JOLTS Report and Key U.S. Data Take Center Stage

Morning Wrap: Wall Street Returns to the Offensive as Palantir Fuels AI Optimism

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.