Key highlights

- Goldman Sachs reaffirmed its forecast for gold to reach $4,900 per ounce by the end of 2026, citing both structural and cyclical factors that continue to support the market.

- The bank sees central bank buying, particularly from emerging markets, as the key long-term driver. Reserve diversification accelerated after Russia's foreign reserves were frozen in 2022 and continues to provide a strong source of demand.

- Goldman Sachs also pointed to the latest World Gold Council survey, which found that 45% of central banks plan to increase their gold holdings over the next 12 months—the highest reading since the survey began.

- In the short term, however, gold continues to face headwinds from the Federal Reserve's hawkish stance. Markets have once again started pricing in the possibility of U.S. rate hikes, weighing on demand for gold-backed ETFs.

- Higher bond yields and persistently elevated inflation expectations have improved the relative attractiveness of yield-bearing assets, leading some capital to rotate away from precious metals.

- Goldman Sachs does not share the market's expectation of further monetary tightening. Its economists expect the Fed to leave interest rates unchanged this year and delay the start of the easing cycle until the second half of next year.

- Such a scenario would likely support a gradual recovery in ETF positioning, which has historically strengthened when investors expect lower real interest rates.

- Over the medium and long term, Goldman Sachs believes the balance of risks remains skewed to the upside. In addition to central bank purchases, the bank highlights growing concerns over fiscal sustainability in developed economies, which could encourage greater private-sector demand for gold.

- Goldman Sachs argues that gold's current weakness is primarily the result of temporary macroeconomic headwinds. If the Fed proves less hawkish than markets currently expect and central banks maintain their strong pace of buying, gold could resume its long-term uptrend.

- As a result, oil prices and upcoming inflation data may prove to be the key catalysts for gold's next major move.

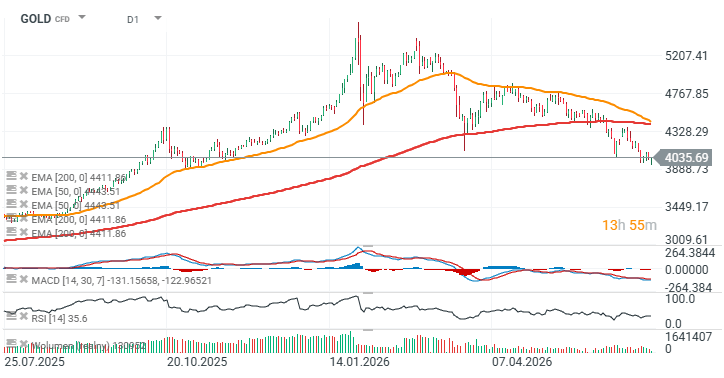

GOLD chart (D1)

- From a technical perspective, the first major resistance is located near $4,400 per ounce, where the 200-day Exponential Moving Average (EMA200, red line) is currently positioned.

- The EMA50 and EMA200 are approaching a bearish "death cross" formation. If confirmed, it would be the first such crossover since 2023. However, this pattern does not reliably predict future price direction and often appears after a significant sell-off, making it more a sign of an oversold market than a standalone bearish signal.

- The next important support for gold is located around $3,800 per ounce, corresponding to a major price reaction zone established in 2025.

Source: xStation5

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.