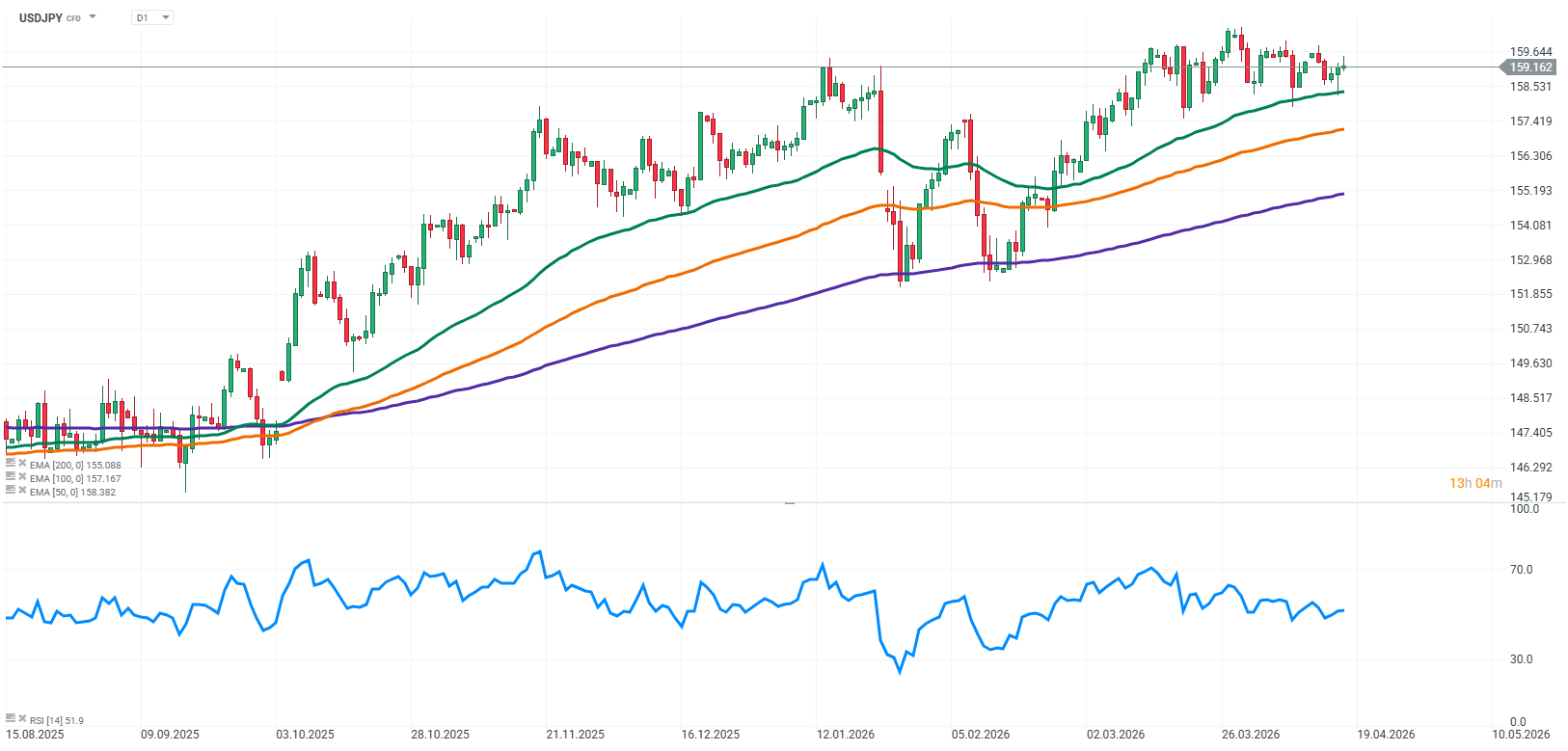

USDJPY remains at the center of global currency market attention, with its price action increasingly driven not only by macroeconomic fundamentals but also by rising political risk. As the exchange rate approaches the psychological barrier at 160, the market is beginning to view this level as a potential tolerance threshold for Japanese authorities rather than just another point on the chart. As a result, the discussion around the next directional move is becoming less purely fundamental and increasingly focused on whether and when a response from Japan’s Ministry of Finance could materialize.

Source: xStation5

What Is Driving USDJPY today?

Rising Intervention Risk Around the 160 Area

As USDJPY moves closer to the 160 zone, sensitivity to potential currency intervention is clearly increasing. This level is widely seen as a boundary where Japanese authorities may step in, either through direct market operations or via strong verbal warnings. Historical experience suggests that such environments can trigger sharp and asymmetric market reactions, as speculative positions built on yen weakness become vulnerable to rapid unwinding once intervention signals emerge.

Bank of Japan Between Inflation Pressures and Growth Risks

At the same time, the Bank of Japan remains a key piece of the puzzle. On one hand, persistent inflation supports the case for gradual policy normalization. On the other hand, growing concerns about slowing economic momentum and emerging stagflation-like risks continue to weigh on the policy outlook. As a result, the BoJ remains cautious and avoids committing to aggressive tightening, which limits yen strength and sustains uncertainty about the future path of monetary policy.

Interest Rate Differentials as the Core Trend Driver

Despite rising volatility around key levels, the primary structural driver remains the wide interest rate differential between the United States and Japan. This gap continues to support US dollar strength and keeps carry trade strategies attractive. However, market participants are increasingly aware that such an environment can persist for an extended period without being stable, especially as USDJPY approaches levels perceived as potentially sensitive to intervention risk.

The Role of Oil and the Gulf Region for Japan

An often underestimated factor in the broader USDJPY picture is the oil market and Japan’s dependence on energy imports from the Gulf region. As a highly import-dependent economy, Japan is particularly sensitive to fluctuations in oil prices, with higher energy costs directly worsening its terms of trade and adding inflationary pressure domestically. In this context, developments in the Middle East and OPEC production policy can have a meaningful impact not only on Japan’s external balance but also on expectations regarding Bank of Japan policy.

Rising oil prices from the Gulf region act as an additional inflationary force for Japan. In such an environment, the FX market increasingly incorporates not only interest rate differentials but also external cost shocks that may influence the pace of monetary policy normalization and the broader outlook for the yen.

Key Takeways: A Market Defined by Boundaries and Event Risk

Overall, USDJPY is in a phase where traditional fundamental drivers still support higher levels, but their influence is increasingly counterbalanced by political risk and the possibility of intervention. As a result, the market is becoming less of a directional trend story and more of a range-bound, event-driven regime where asymmetry of risk and sudden volatility shifts play a dominant role.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.