We end Wednesday with declines across nearly all key indices. Investors are staging a minor correction following the recent spectacular rally. Headlines from the Middle East are playing a significant role in this context.

Commodities

We have seen the third consecutive day of rising energy commodity prices. WTI crude oil prices rose by over 2% (climbing above $95), and NATGAS saw similar gains (moving towards $5.0).

- The surge in energy prices can be largely attributed to the renewed escalation in the Middle East. Upward pressure may have also been amplified by today's release from the US Department of Energy, which showed an unexpectedly large drop in crude inventories—by as much as 8 million barrels (the market had anticipated a decline of just 3 million).

On the flip side, gold (-1%) and silver (-2%) moved in the opposite direction.

- A key factor here was the rise in bond yields. 10-year yields pushed upward in the US (+1.1%), Germany (+2%), and Japan (+2.3%), among others.

Geopolitics

Iran has attacked an airport in Kuwait and violated airspace in Bahrain. This reportedly comes as retaliation for the shelling of an Iranian tanker by US forces.

The probability of the two sides reaching an agreement to permanently reopen the Strait of Hormuz later this June is falling. Markets are currently pricing the likelihood of such a scenario at around 20%.

Stock Market

All of this is leading to a modest investor retreat from risk.

- European stock markets took a particularly hard hit today, including the German DAX (-1.3%), which was dragged down by weak performances from major corporations. Declines were seen in SAP (-4,3%), Deutsche Bank (-3.7%), Mercedes-Benz (-3.3%), Adidas (-3.2%), and Deutsche Telekom (-2.7%).

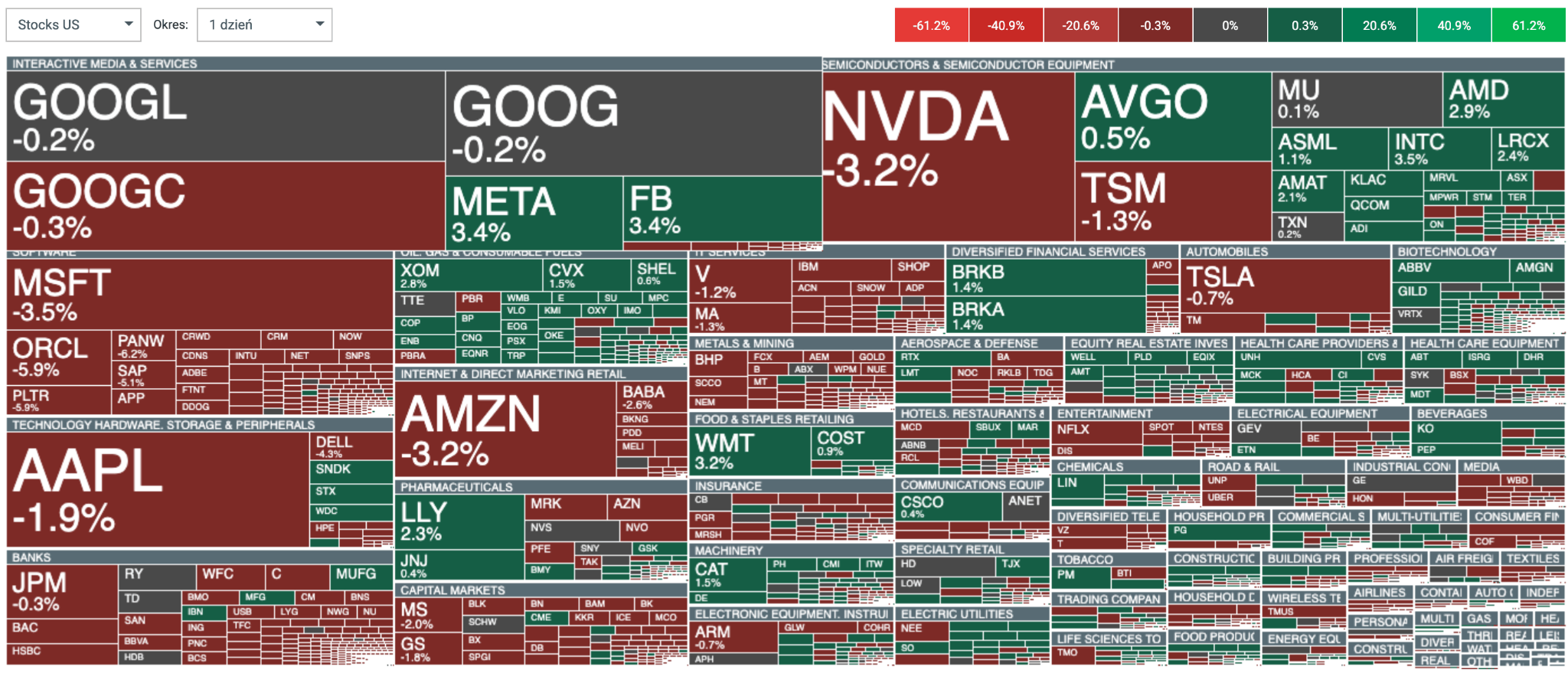

However, weakness was also visible in the United States today.

- The S&P 500 fell by 0.6%, while the NASDAQ Composite dropped by 1%.

- A key driver in this context was a more than 3% drop in NVIDIA's share price. Microsoft (-3.8%), Amazon (-3.1%), and Palantir (-6.1%) also headed downward.

On the other hand, shareholders of Marvell have reason to be pleased, as the stock has soared by over 35% compared to Tuesday's opening (up 5.3% today). This is partly driven by highly complimentary remarks from Nvidia CEO Jensen Huang. Speaking on stage in Taipei alongside Marvell's chief executive, Huang anointed the company as the next one poised to reach a trillion-dollar valuation.

Chart 1: Heatmap of the day's winners and losers on the US market (06.03.2026)

Source: xStation, 06.03.2026

Source: xStation, 06.03.2026

Macroeconomic Data

The May ISM Services PMI indicators were released today. These data points are of secondary importance to the markets, so in the absence of a major surprise, the investor reaction remains limited. The print of 54.5 came in above expectations, but it wasn't enough to trigger elevated volatility.

Our attention is drawn to the unexpectedly high new orders sub-index (57.3) and the prices paid index (71.3)—the latter being consistent with expectations of intensifying price pressures, climbing to its highest level since 2022. Meanwhile, employment data came in slightly below 50 (47.9), though markets are already eagerly anticipating Friday's NFP (Non-Farm Payrolls) print. This is the data release with by far the highest potential to stir up volatility this week.

---

Michał Jóźwiak, Financial Markets Analyst at XTB

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.