- The Brazilian real remains the world’s best-performing currency in 2026*.

- However, last week saw a political scandal and a significant weakening of the currency.

- The Central Bank of Brazil’s interest rates remain very high, also in real terms.

- The country is benefiting from higher oil prices as well.

- The Brazilian real remains the world’s best-performing currency in 2026*.

- However, last week saw a political scandal and a significant weakening of the currency.

- The Central Bank of Brazil’s interest rates remain very high, also in real terms.

- The country is benefiting from higher oil prices as well.

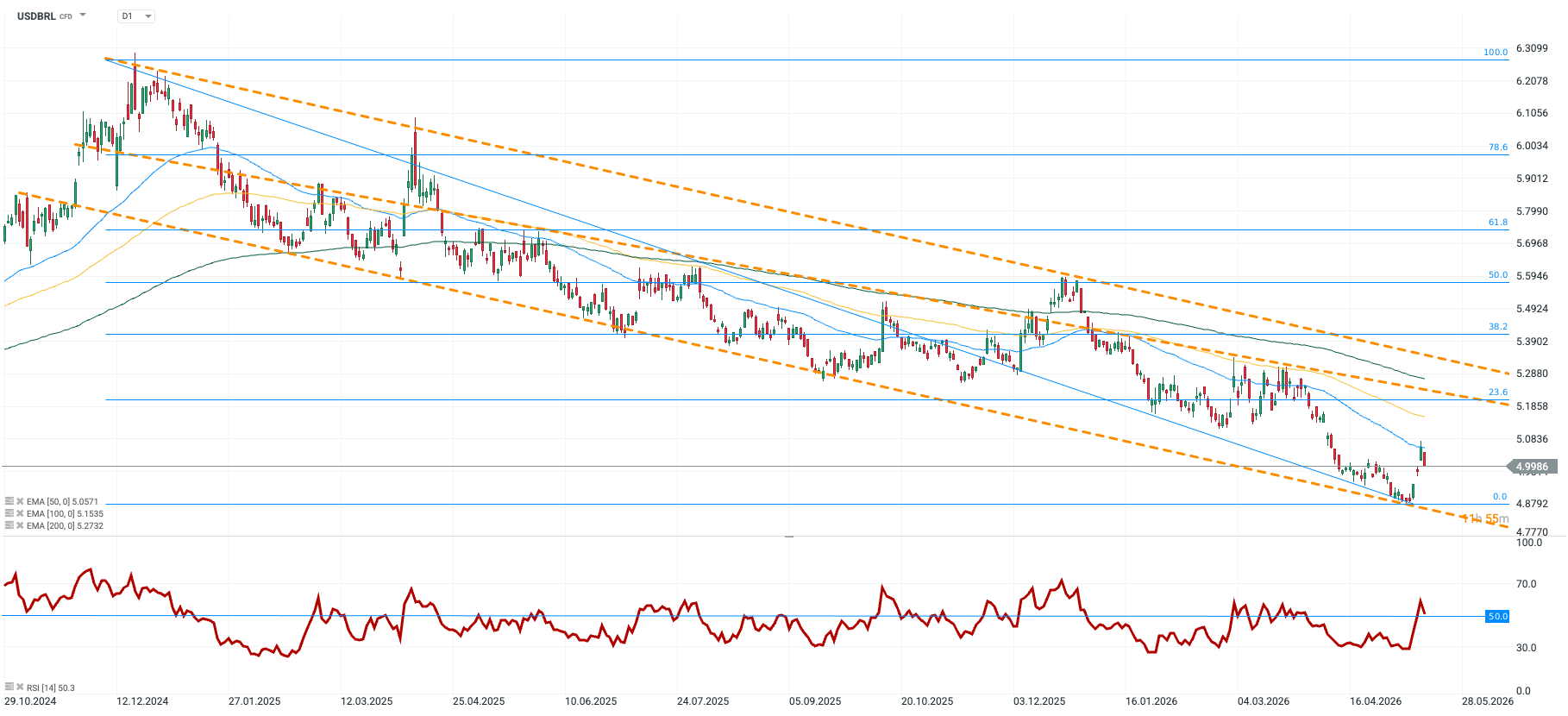

The best-performing currency of 2026*, the Brazilian real, came under fire last week, suffering its largest weakening against the US dollar since October 2025.

Chart 1: USDBRL (29/10/2024 - 19/05/2026)

Source: xStation, 19/05/2026

Source: xStation, 19/05/2026

* Zambian kwacha, Russian ruble and Costa Rican colón place higher on the dashboard, but are not among currencies we analyse on a regular basis.

What stands behind such a significant move?

The reason behind the depreciation of the real can be found primarily in the recordings and news published by The Intercept Brazil incriminating Flavio Bolsonaro, senator and right-wing candidate for the presidential position in the October elections. According to the materials, Flavio demanded millions of dollars from Daniel Vorcaro, former CEO of Banco Master. The total amount of the transactions under investigation is estimated to be over $25 million.

According to Bolsonaro, the money was intended to finance a biopic about his jailed father, Jair Bolsonaro, the country's former president. Flavio claims it was 100% private sponsorship of a private project, with Vorcaro and Banco Master not set to receive any political favours in return.

The federal police and the Supreme Court immediately took up the matter, which – despite Bolsonaro's explanations – led to a decline in his ratings. Flavio had been on an upward trend for some time. Since the beginning of May, he had been the favorite to win the election according to the odds on the Polymarket platform, surpassing Lula in most polls too.

The market sees a certain risk in the increased likelihood of a victory for Lula, the leader of the left. The lack of even gradual fiscal consolidation, given the budget deficit, which has exceeded 8% of GDP for 3 years now, seems problematic. The market seems to have partially priced in these concerns, which allowed the real to rebound at the beginning of the week.

What supports the real?

High interest rates

Banco Central do Brasil has already made two cuts in the current cycle, but the reference rate remains at a very high level (14.5%), allowing the currency to benefit from the carry trade. While further cuts cannot be ruled out in the coming months, their scale should be limited due to the unanchored inflation expectations and loose fiscal policy. This could allow the real to continue to benefit from the carry trade.

Net oil exporter position

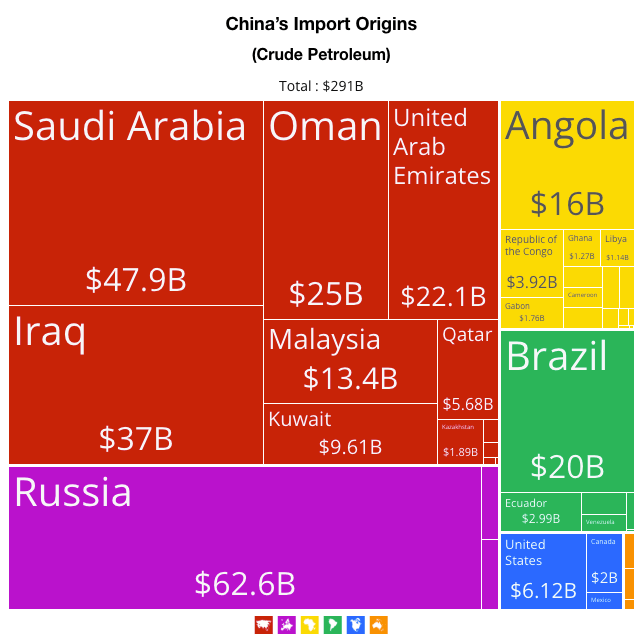

Brazil is one of the world's largest oil producers (approximately 4.2 million barrels per day). While some of this is consumed domestically, the surplus is significant enough to make the country a major player on the global stage, generating over $55 billion in revenue annually from oil exports. The main recipient of Brazilian oil (43% of total exports) is China, which currently has little room for negotiation. Its import structure is dependent on the Middle East (55%), Russia (21%), aforementioned Brazil (7%) and Angola (5%).

Chart 2: China's Crude Oil Import Structure (2024)

Source: OEC (19/05/2026)

Source: OEC (19/05/2026)

The currency is also supported by the increase in soybean prices, which account for over 12% of domestic exports.

Improved sentiment towards emerging markets

April brought a significant improvement in risk sentiment on both currency and equity markets. Recent days have cast doubt on the continuation of this trend. However, if President Trump's announcements regarding the ongoing US-Iran negotiations would indeed come into life, the real, due to its high beta (specific risk, sensitivity to market changes), could continue its gains (although assuming such a scenario, we can expect declines in oil prices, which would put some pressure on the currency).

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

Daily Summary: A sell-off with a spin-off

Iran Escalation: What to Watch and What to Expect

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.