The USD/JPY pair continues its upward trajectory, breaching the resistance zone between 146.5 and 147. This marks its highest level since the latter half of June. The pair's outlook has notably shifted recently, following a significant decline from its recent peak in the begining of 2025.. A decisive break of this latest resistance could signal a continued ascent towards the 150 mark, where the 50.0 Fibonacci retracement of the previous downward wave and the 200-period moving average converge. So, what's driving the yen's recent weakness?

The Bank of Japan (BoJ) was widely expected to embark on a rate-hiking path this year, yet its last increase occurred in February. Nevertheless, the BoJ remains exceptionally hawkish compared to the past decade and a half, given that interest rates are at their highest since 2008 and bond purchase tapering has been underway since 2024. Intriguingly, the BoJ has refrained from further hikes despite persistent high inflation, which stood at 3.5% in May (down from 3.6% in April). Notably, Japan has recently experienced a sharp rise in food prices, with rice prices surging over 100% in May, posing a significant challenge for less affluent segments of society. The BoJ's current dilemma is economic growth, or rather, its contraction, which registered an annualized -0.2% in the first quarter, albeit better than the anticipated -0.7%.

Economic growth, in turn, faces increased peril from the escalating trade war. Donald Trump's proposed 25% tariff on all Japanese products is deemed unacceptable by the export-oriented nation. Even prior to this, the 25% tariff on automobiles posed a considerable hurdle. Analysts at UBS caution that tariffs could shave 0.8 percentage points off Japan's GDP this year, with a worst-case scenario seeing a nearly 2 percentage point reduction.

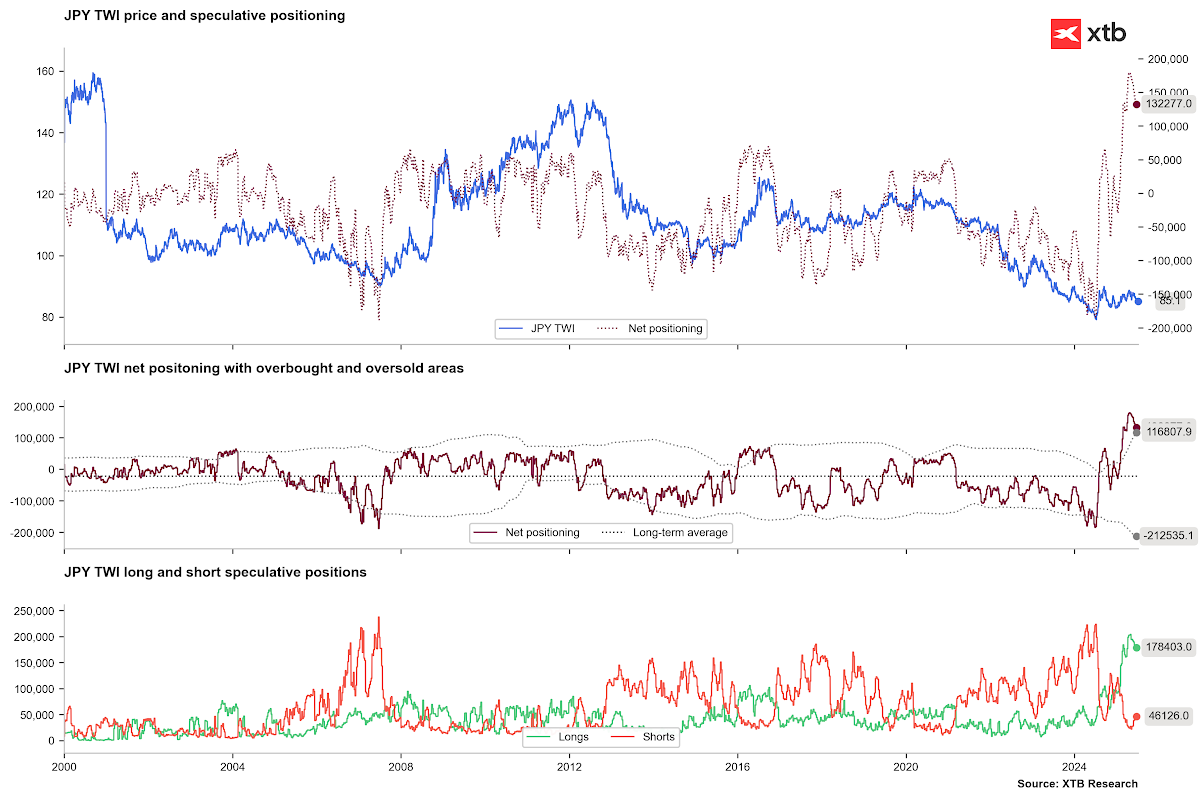

The deteriorating outlook for Japan is prompting a shift in investor sentiment, potentially leading to a resurgence of carry trade strategies. Recently, the number of long positions has decreased from extremely high levels, while short positions have simultaneously increased. Source: Bloomberg Finance LP, XTB

Should the resistance at the 38.2 Fibonacci retracement and the upper boundary of the ascending trend channel be decisively broken, the target would be around 150. Conversely, sustained resistance and an increase in demand for the yen could result in a renewed decline towards the lower boundary of the ascending trend channel. Source: xStation5

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Tensions around Iran weigh on markets!

US Open: Alphabet and Tesla Weigh on Wall Street, While Oil Prices Renew Investor Concerns

Wheat climbs to the highest level since May 2024 🚜 Black Sea export risks fuel rally

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.