The USDJPY rose to its highest level since December 1986 (162.8) on Wednesday. Since then, however, it has recorded a decline of over 1%.

A shift in approach to currency interventions

June's intervention attempts by the Japanese authorities proved unsuccessful. Following temporary declines, the USDJPY pair reached new highs.

Consequently, according to Reuters reports, officials are set to abandon the previous practice of signaling intervention risks, instead taking action to exert pressure on speculators and increase the costs associated with betting against the yen. Communication signaling specific exchange rate levels that could trigger action from the authorities is also expected to be abandoned.

This change in approach appears to be gaining market approval; the yen strengthened yesterday morning by nearly 0.9% against the dollar, holding gains until the end of the day thanks to a weaker-than-expected US non-farm payrolls (NFP) report.

Today, the Japanese currency is experiencing further strengthening, potentially influenced by broader dollar weakness as well as comments from Finance Minister Satsuki Katayama, who stated that Tokyo remains ready to intervene in the foreign exchange market while emphasizing close cooperation with Washington in this regard. She also addressed rising bond yields, noting that fiscal policy will be conducted in a way that restores market confidence.

Further rate hikes ahead

The Bank of Japan is currently at a historic turning point, moving away from decades of ultra-loose monetary policy. In mid-June, it raised the main interest rate to its highest level since 1995 (1%).

In line with market consensus and signals from board members (including the hawkish Naoki Tamura), this is not the end of the tightening cycle. The market expects rates to rise systematically over intervals of several months towards the neutral rate, which, according to policymakers, currently stands at 1.5%-2.0%.

The government administration is pushing hard for rate hikes to prevent excessive currency depreciation. As an aside, it is worth adding that one of the main beneficiaries of this situation is the Japanese banking sector.

Tightening supported by macroeconomic data

Data remains the foundation for the continuation of the hawkish pivot. The Bank has significantly raised its inflation forecasts, expecting the core measure to rise to 2.5-3% in fiscal year 2026, well above the 2% inflation target.

Medium- and long-term inflation expectations also remain elevated. Moreover, inflation is no longer being driven solely by external factors. Wages grew in April (3.5%) at their fastest pace since 2024, and Japanese companies are increasingly willing to pass higher labor costs onto final prices.

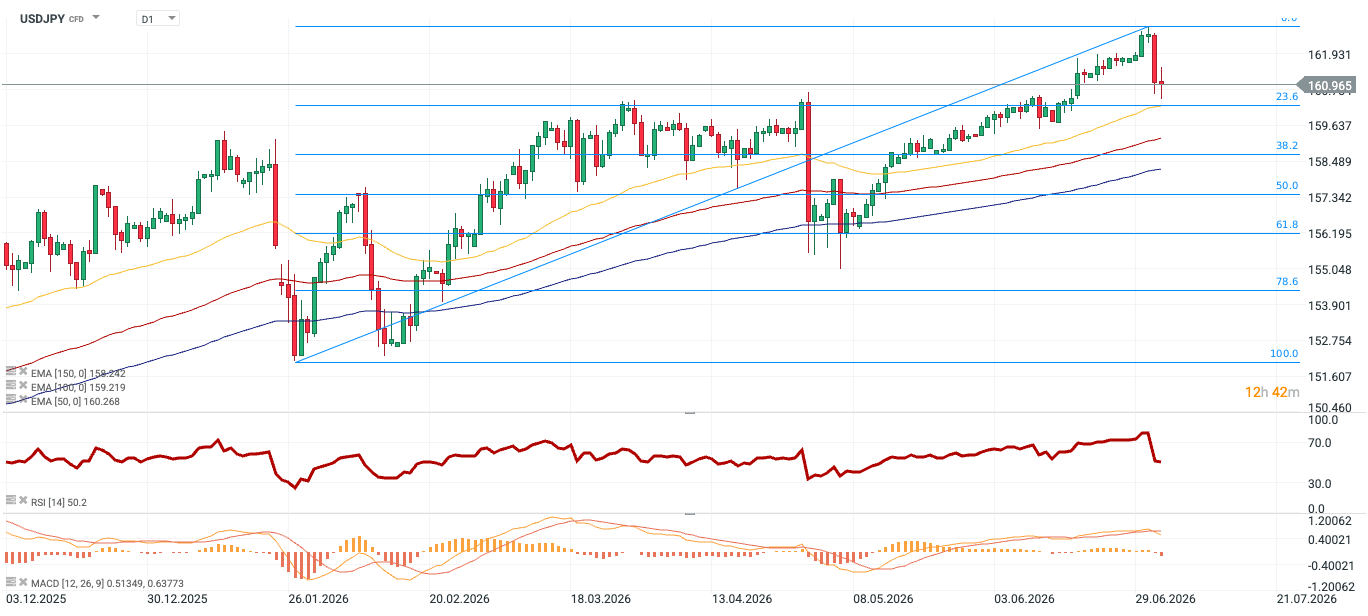

Technical Analysis

Figure 1: USDJPY (03.12.2025 - 03.07.2026)

Source: xStation, 03.07.2026

Source: xStation, 03.07.2026

Despite a significant correction, the pair is still in a long-term, stable uptrend. The basic structure (a pattern of higher highs and higher lows on a daily basis) has not yet been permanently negated.

The 160.2 area currently acts as a critical defensive zone, resulting from the convergence of two significant technical factors: the 50-period exponential moving average (EMA 50 – 160.268) and the 23.6% Fibonacci retracement level for the broader upward wave.

The RSI has left the strong overbought territory and stabilized at an almost completely neutral level (50.2). This creates space for generating a new directional impulse.

Short-term dominance of the selling side is confirmed by the MACD. The crossover of the signal line from above and the growing negative histogram reflect downward momentum, which dictates caution when prematurely assuming that the correction has definitively ended.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

Economic Calendar: Time for Tesla and Google Earnings (22.07.2026)

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.