CME Group shares (CME.US) are currently trading at an all-time high, near USD 300 per share, and have risen by more than 10% year-to-date, against a mixed backdrop on Wall Street. The stock is supported by strong institutional participation in the market, the growing systemic importance of the exchange, and new products that offer a prospect of improving revenue growth momentum.

- The company benefits both from elevated volatility and record-high volumes in the metals market (as the owner of COMEX), strong positioning in agricultural commodities (CBOT), trading in Bitcoin and Ethereum (where it is the clear leader), and other cryptocurrency derivatives.

- CME is also a beneficiary of very high trading volumes in the U.S. Treasury market, as well as in futures on the S&P 500 stock index (E-mini).

Will rare earth futures drive CME higher?

Yesterday, the Chicago exchange operator said it is working on the world’s first rare earth metals futures contract - according to Reuters sources, the project is expected to focus on neodymium and praseodymium (NdPr).

- The goal of the contract is to enable governments, companies, and banks to hedge exposure to the rare earths market, which is currently dominated by China.

- ICE is also considering a similar product, but according to two sources, it is at an earlier stage of development than CME.

- Rare earths (17 elements) are critical to the energy transition, electronics, and the defense sector; NdPr are particularly important because they are used to produce permanent magnets found, among other things, in EV motors, wind turbines, fighter jets, and drones.

- Sources emphasize that such an instrument is currently a “missing piece” from the perspective of markets and supply-chain risk management.

- A decision to launch the contract has not yet been made, and the main barrier is that rare earths are illiquid and represent a relatively small market compared with other metals traded on futures exchanges.

- The topic is gaining importance as the West steps up efforts to increase production of critical minerals - the U.S. has created a preferential trade bloc with allies and launched a strategic stockpile worth about USD 12 billion.

- NdPr prices are currently set mainly in China and are reflected in indices from agencies such as Fastmarkets, Benchmark Mineral Intelligence, and Shanghai Metals Market.

- In China, there are two spot exchanges for rare earths (Ganzhou Rare Metal Exchange and Baotou Rare Earth Products Exchange), and the Guangzhou Futures Exchange has signaled plans to launch rare earths futures contracts.

What did the company report for Q4 2025?

Q4 2025 results were broadly in line with market expectations. CME highlighted broad-based growth in activity across all asset classes and a rising share of retail investors (higher volumes, among others, in interest rates, energy, metals, agricultural products, and crypto).

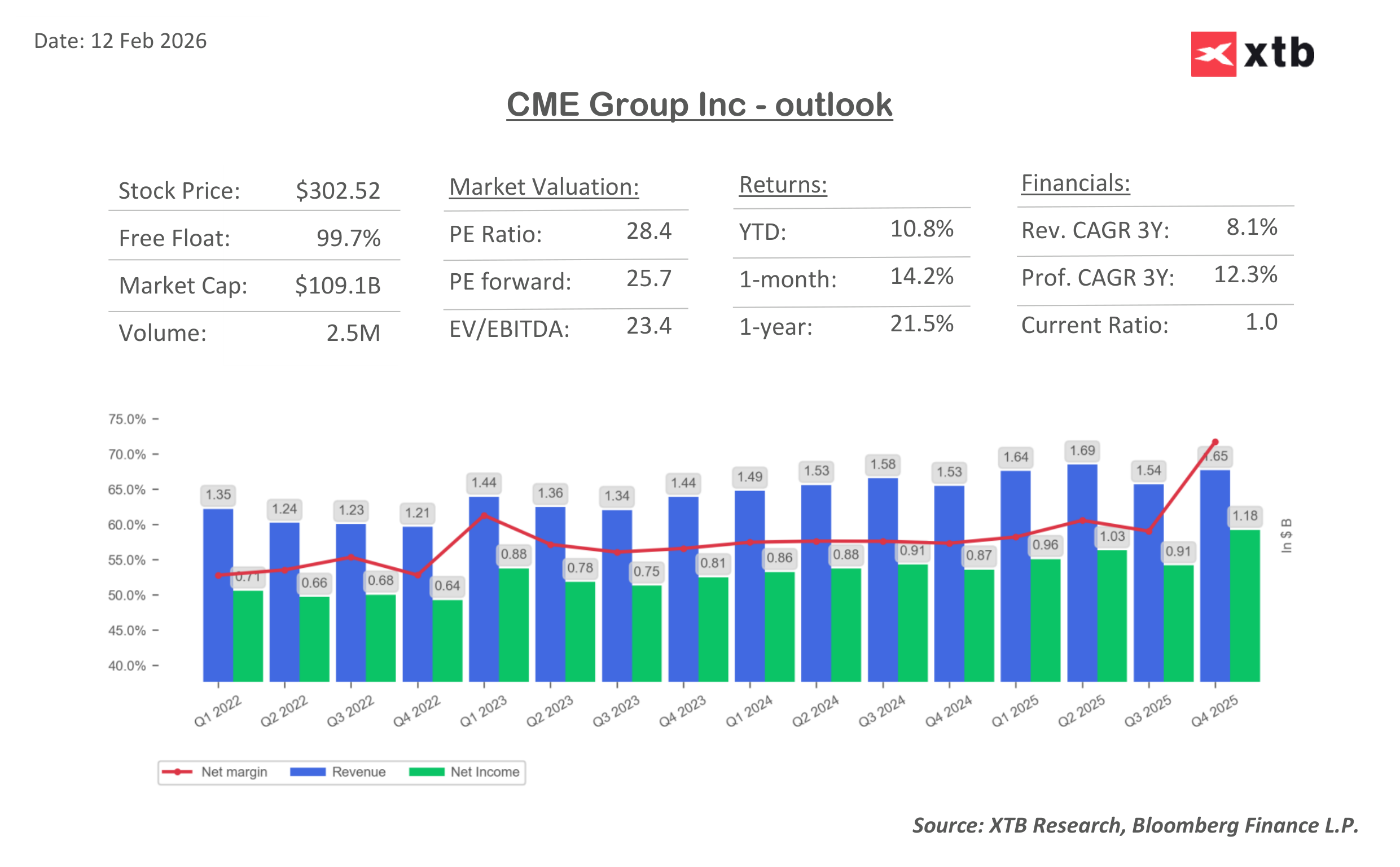

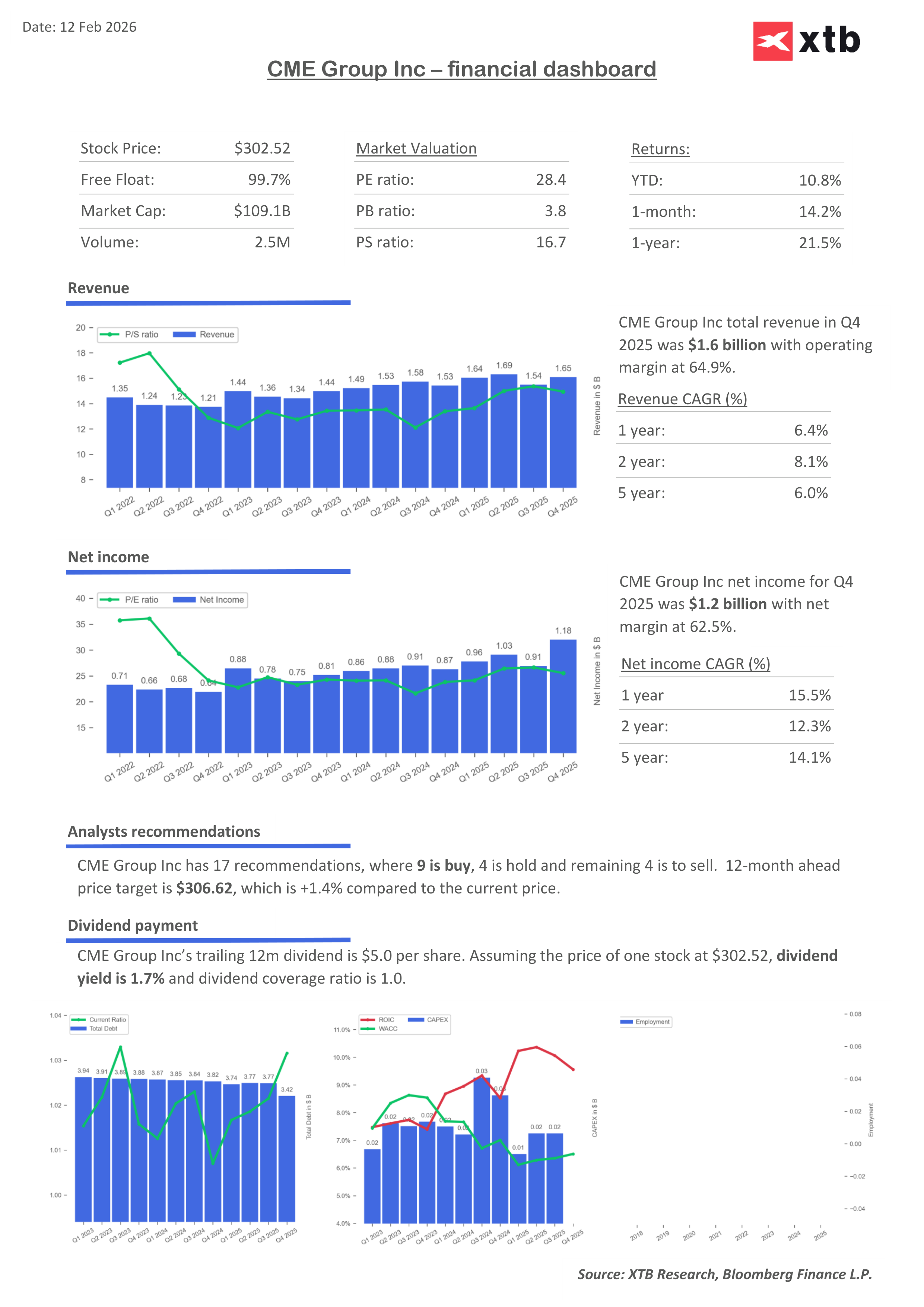

- Key figures: revenue of USD 1.65bn (vs. USD 1.64bn consensus; +8.1% y/y), adjusted EPS of USD 2.77 (vs. USD 2.74 forecast), adjusted EBITDA of USD 1.13bn (in line with expectations; margin 68.6%), operating margin of 61.8% (similar to last year), market cap of about USD 110bn.

- What did management point to as the quarter’s “driver”? New so-called “event contracts” and strong sales/retail activity in micro products. The company also emphasized diversification of its client base and solid conditions in both institutional and retail segments amid elevated volatility.

Key takeaways from the analyst call

-

Client base resilience amid volatility and margin changes: management pointed to solid demand from both retail and institutional clients, with rising open interest and volumes seen as evidence of a “healthy ecosystem.”

-

Prediction markets and regulatory risks: questions were raised about CME’s involvement and legal oversight; the company stressed a cautious approach and a focus on products within the CFTC framework (swap-based).

-

Pricing changes and impact across asset classes: CME spoke about diversified revenue growth from market data, selective fee adjustments (including in metals and micro products), and a review of incentive programs.

-

Durability of market data revenues in the AI era + capital returns: management argued that proprietary data remain key to clients’ strategies; the topic of buybacks was linked to the use of funds (including from a transaction in Austria) for share repurchases.

-

Migration to Google Cloud and costs: the company reported progress, and future technology spending is expected to be incorporated into overall guidance as “legacy” costs are phased out.

CME share price chart (CME.US), D1 interval

Source: xStation5

CME valuation

CME’s valuation, measured by the standard price-to-earnings ratio, does not appear overly demanding (P/E around 28, forward P/E 25), given the business’s high margins, relatively strong growth predictability, and a degree of “resilience,” since the company earns mainly on trading volumes — not on the direction of indices or the price moves of individual assets. Over the past five years, average annual profit growth has reached 14%, and if this pace were to be maintained over the next five years, with a similar net margin, we can reasonably say that the rise in the share price is not yet decoupled from CME’s fundamentals. The gap between ROIC and WACC indicates that the company is focused on creating shareholder value, and it offers an average annual dividend yield of around 2%.

Source: Bloomberg Finance LP, XTB Research

Source: Bloomberg Finance LP, XTB Research

Chart of the Day: AI supports gains – can Tesla and Google sustain them? (22.07.2026)

Economic Calendar: Time for Tesla and Google Earnings (22.07.2026)

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Did SaaS lost too much? Morgan Stanley says yes.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.