ICE cocoa futures are rising by more than 6% today, climbing above USD 4,100 per tonne and posting one of their strongest gains in several weeks. Just a few days ago, investors were focused on increasing supply from West Africa and rebuilding inventories, but the market has quickly been reminded of the risks that could once again constrain production in the coming seasons. El Niño forecasts, deteriorating prospects for the 2026/27 crop, and a record number of funds betting on further price declines have all moved into focus.

Funds forced to cover shorts: Is El Niño back in play?

One of the main drivers behind today’s move is the market’s technical setup. According to the latest Commitment of Traders report, investment funds increased their net short positions in early June to 21,111 contracts. This marked the highest level in more than three years and was a clear indication that a significant portion of the market had been positioned for further downside.

Such a large concentration of bearish positions often increases the risk of sharp moves in the opposite direction. All it takes is a fundamental catalyst or a shift in sentiment for investors to begin closing short positions en masse. This process, known as short covering, frequently leads to powerful rallies in commodity markets.

Today’s rebound fits that scenario perfectly. The market received several new reasons to be cautious about expectations for continued supply growth, prompting some investors to lock in profits on short positions. As a result, the rally gained additional momentum.

The most important factor supporting prices remains the weather outlook for West Africa. Japan’s Meteorological Agency confirmed this week that an El Niño pattern has formed across the equatorial Pacific. At the same time, the U.S. National Oceanic and Atmospheric Administration (NOAA) estimates a 67% probability of a so-called Super El Niño, which could rank among the strongest ever recorded.

For the cocoa market, this development is highly significant. El Niño often brings hotter and drier conditions to West Africa, a region responsible for roughly 70% of global cocoa production. Under such circumstances, cocoa yields can deteriorate significantly, especially if unfavorable weather persists for several months.

In addition, early surveys for the 2026/27 season indicate below-average cherelle formation on cocoa trees. This is one of the first warning signs suggesting that the main crop, which begins in October, may disappoint. Investors are therefore beginning to price in the possibility that the current improvement in supply could prove temporary.

Data from Africa currently tell a very different story

At the beginning of the week, bearish arguments still dominated the market narrative. Ivory Coast reported a significant improvement in cocoa arrivals at its ports. Since the start of the 2025/26 marketing season on October 1, approximately 1.95 million tonnes of cocoa had reached ports by June 7.

This represents an increase of 18.9% compared with the same period a year earlier. Moreover, in May, the country raised its full-season cocoa delivery forecast to 2.2 million tonnes from the previous estimate of 1.8–1.9 million tonnes. Authorities cited favorable weather conditions and better-than-expected harvests as the key reasons for the revision.

Several institutions monitoring the cocoa market have also highlighted the improving supply situation. The International Cocoa Organization (ICCO) estimates that global cocoa production in the 2024/25 season will rise by 8.3% year-on-year to 4.723 million tonnes. If confirmed, this would mark the first global cocoa surplus after four consecutive years of deficits.

Inventories are rising, but the market remains unconvinced

Another bearish factor remains the increase in inventories monitored by ICE. At the beginning of June, exchange-monitored stocks climbed above 2.93 million bags, reaching their highest level in roughly 1.75 years. For many market participants, this signaled that supply pressures were gradually easing.

At the same time, some analysts argue that higher inventories do not automatically solve the market’s structural challenges. Cocoa production remains highly concentrated geographically, with the majority of global supply coming from just a handful of West African countries.

In practice, this means that even if inventories recover temporarily, the market remains extremely vulnerable to weather-related disruptions. Investors still remember how quickly prices reacted in recent years to reports of droughts, crop diseases, and logistical bottlenecks across the region.

Chocolate demand proves more resilient than expected

For months, elevated cocoa prices raised concerns about weakening chocolate consumption. However, recent data paint a more nuanced picture. Earnings reports from major chocolate manufacturers such as Hershey and Mondelez came in above expectations, suggesting that consumers continue to absorb higher prices for chocolate products.

At the same time, cocoa grinding data indicate weakening demand in several regions. In North America, first-quarter grindings declined by 3.8% year-on-year to 106,087 tonnes. In Europe, grindings fell by 7.8% to 325,895 tonnes, a weaker-than-expected result and the lowest first-quarter reading in 17 years.

Asia remains the notable exception. Cocoa grindings in the region increased by 5.2% year-on-year to 223,503 tonnes, despite market expectations for a 6.7% decline. This suggests that weaker demand in developed economies is at least partially being offset by rising consumption in emerging markets.

More institutions are cutting surplus forecasts

Although the market remains formally in surplus, expectations regarding the size of that surplus continue to shrink. StoneX recently lowered its forecast for the global cocoa surplus in the 2026/27 season to 149,000 tonnes from 267,000 tonnes projected in January. The revision was largely driven by growing concerns over the potential impact of El Niño on West African cocoa production.

At the same time, StoneX reduced its 2025/26 surplus estimate to 247,000 tonnes from 287,000 tonnes previously forecast. A similar trend can be seen in ICCO projections. At the end of May, the organization cut its 2024/25 surplus estimate to 48,000 tonnes from 75,000 tonnes.

Nigeria, the world’s fifth-largest cocoa producer, is also emerging as a source of concern. Cocoa exports from the country fell 20% year-on-year in April to 14,921 tonnes. Meanwhile, the local Cocoa Association expects production in the 2025/26 season to decline by 11% to 305,000 tonnes.

Logistical challenges are adding further support to prices. Ongoing disruptions linked to shipping through the Strait of Hormuz are increasing freight, fuel, and insurance costs, raising the overall cost of cocoa imports around the world.

Producer policy decisions also remain relevant. Ghana cut the official price paid to cocoa farmers by nearly 30% ahead of the 2025/26 season, while Ivory Coast reduced farmer payments by 57% for the mid-crop harvest that began in March. Together, the two countries account for more than half of global cocoa production.

Today’s rally highlights how cautious investors remain about forecasts of a lasting improvement in supply conditions. Despite rising production, increasing inventories, and a market that remains technically in surplus, only a few weather-related warning signs were needed to trigger a sharp rebound. It serves as another reminder that cocoa remains one of the world’s most weather-sensitive and disruption-prone commodities.

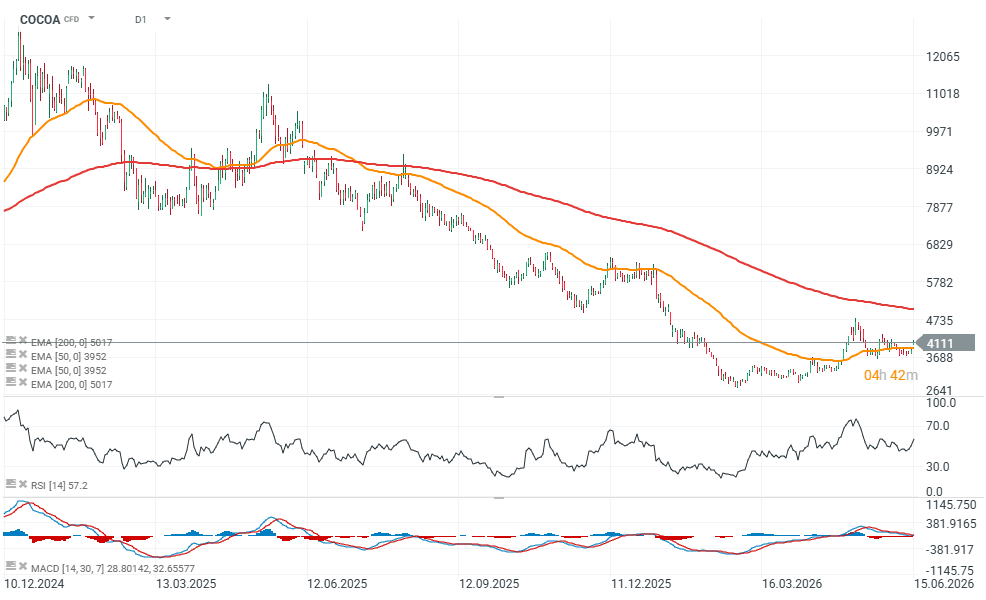

COCOA chart (D1)

Source: xStation5

Eryk Szmyd XTB Financial Markets Analyst

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.