- The main driver behind the decline is better-than-expected harvests in West Africa, the key cocoa-producing region. Improved supply conditions have forced analysts to revise earlier deficit forecasts for the 2025/26 season, putting additional pressure on prices, particularly futures.

- Prices are also being weighed down by weaker demand from food manufacturers. During the period of record-high prices, many companies reduced cocoa content in their products and adjusted formulations to cut costs. The effects of these changes are still visible today.

- Despite the drop in raw material prices, chocolate prices in stores have not yet declined. This is largely due to long-term contracts signed at much higher price levels, as well as manufacturers’ reluctance to quickly revert to previous formulations, which would involve additional costs.

- As a result, the market remains in a typical lagged price transmission phase, where falling raw material prices do not immediately translate into lower prices for end products. In the short term, a noticeable decline in chocolate prices for consumers is therefore unlikely.

- Weather conditions in Ivory Coast remain less favorable for the mid-crop cocoa season. In most growing regions, no rainfall was recorded last week, and farmers are signaling an increasing need for moisture to support the development of the mid-crop, which runs from March to August.

- Although the country has officially entered its rainy season, precipitation remains below market expectations. In practice, this creates a risk of slower pod development during the key months from May to August, despite the presence of many pods of varying sizes on trees.

- The largest rainfall deficits have been reported in several key production regions, including Soubre, Agboville, Divo, Abengourou, Daloa, Bongouanou, and Yamoussoukro. In some of these areas, rainfall totals were significantly below the five-year average, increasing pressure on plantation conditions.

- Farmers are also highlighting deteriorating soil moisture, particularly in central and west-central parts of the country. This is a relevant signal for the market, as Ivory Coast remains the world’s largest cocoa producer, and local weather issues can quickly translate into global supply expectations.

- Harvests remain modest for now, but farmers expect improvement from May. The base scenario assumes higher supply in the coming weeks, although this will largely depend on the return of more regular rainfall.

Alongside demand, weather may once again become a key driver for cocoa prices. If the rainfall deficit persists, it could limit the recovery potential of mid-crop production and increase price sensitivity to supply-side risks. On the other hand, cocoa demand remains weak, while inflationary pressures in the global economy may further increase household sensitivity to prices making a demand destruction a major risk force to future price trend, even despite the weather risk.

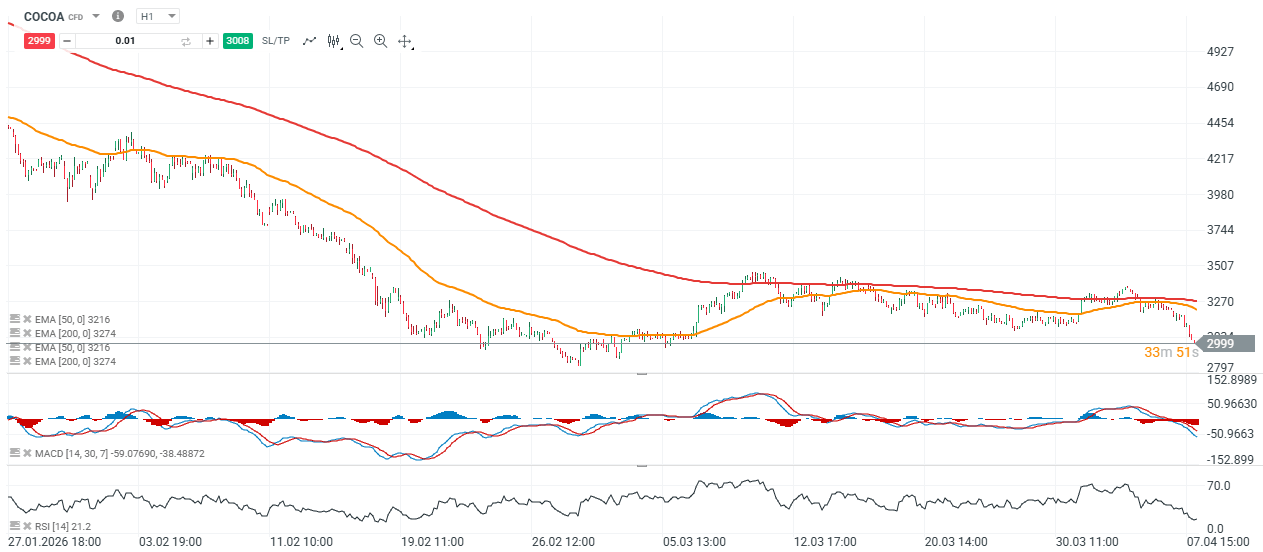

COCOA (H1 chart)

Source: xStation5

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.