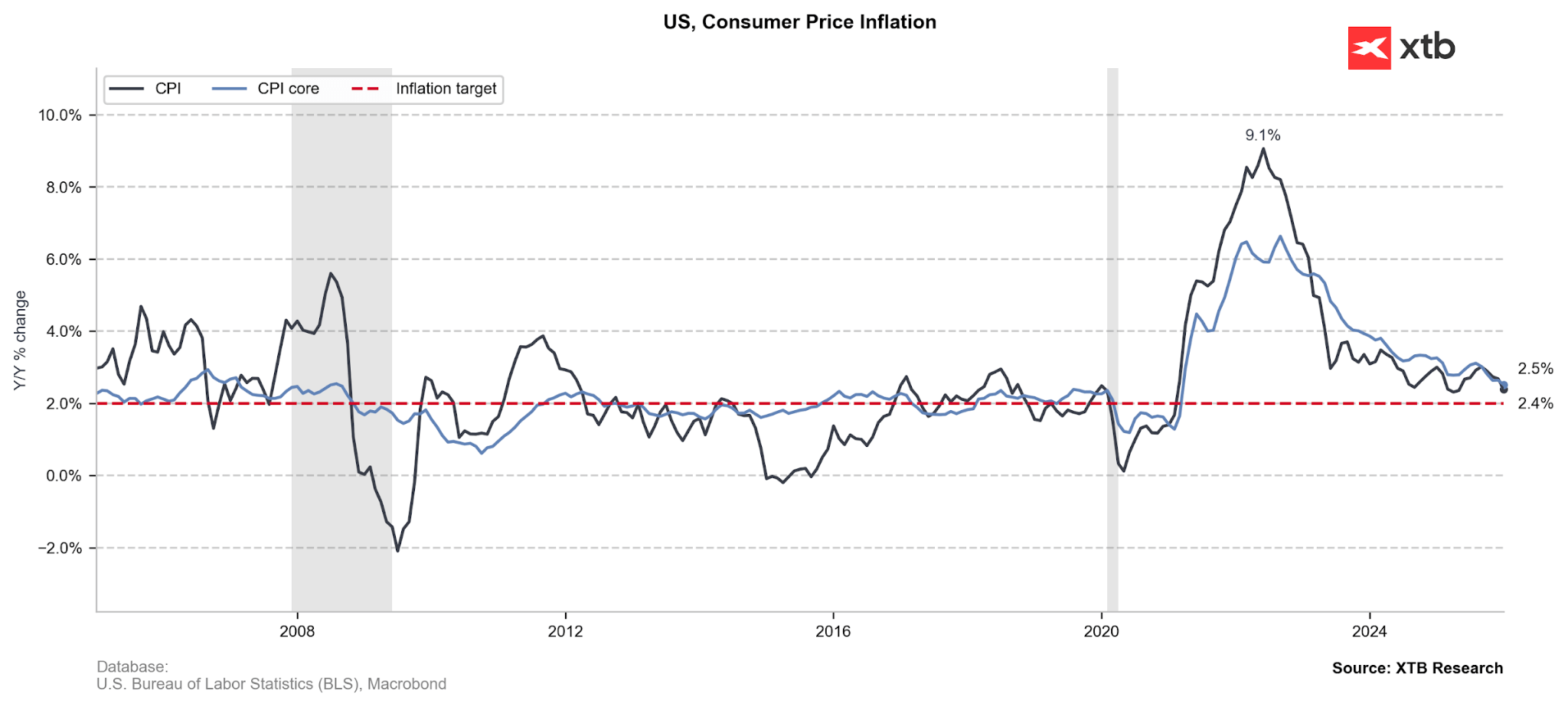

The January inflation report reveals a cooling headline rate — a dynamic that confirms a steady downward trend and places the Federal Reserve in an increasingly enviable position. However, there are still some persistent underlying pressures. While energy provided a significant disinflationary impulse to support this comfortable stance, the fact that service-sector costs and volatile categories like travel remained elevated ensures the Fed will likely remain patient and vigilant.

Disinflation has progressed over recent months, though post-shutdown data uncertainty and continued tariffs transmission raise questions about its sustainability. Source: XTB Research

Headline vs. Core Dynamics:

-

Headline Inflation: The "All items" index rose 0.2% MoM in January, a slight deceleration from the 0.3% recorded in December. This brings the annual (YoY) inflation rate to 2.4%.

-

Core Inflation: Excluding food and energy, prices accelerated slightly to 0.3% MoM (up from 0.2% in December), maintaining a yearly rate of 2.5%.

Significant MoM Changes (Dec 2025 to Jan 2026):

-

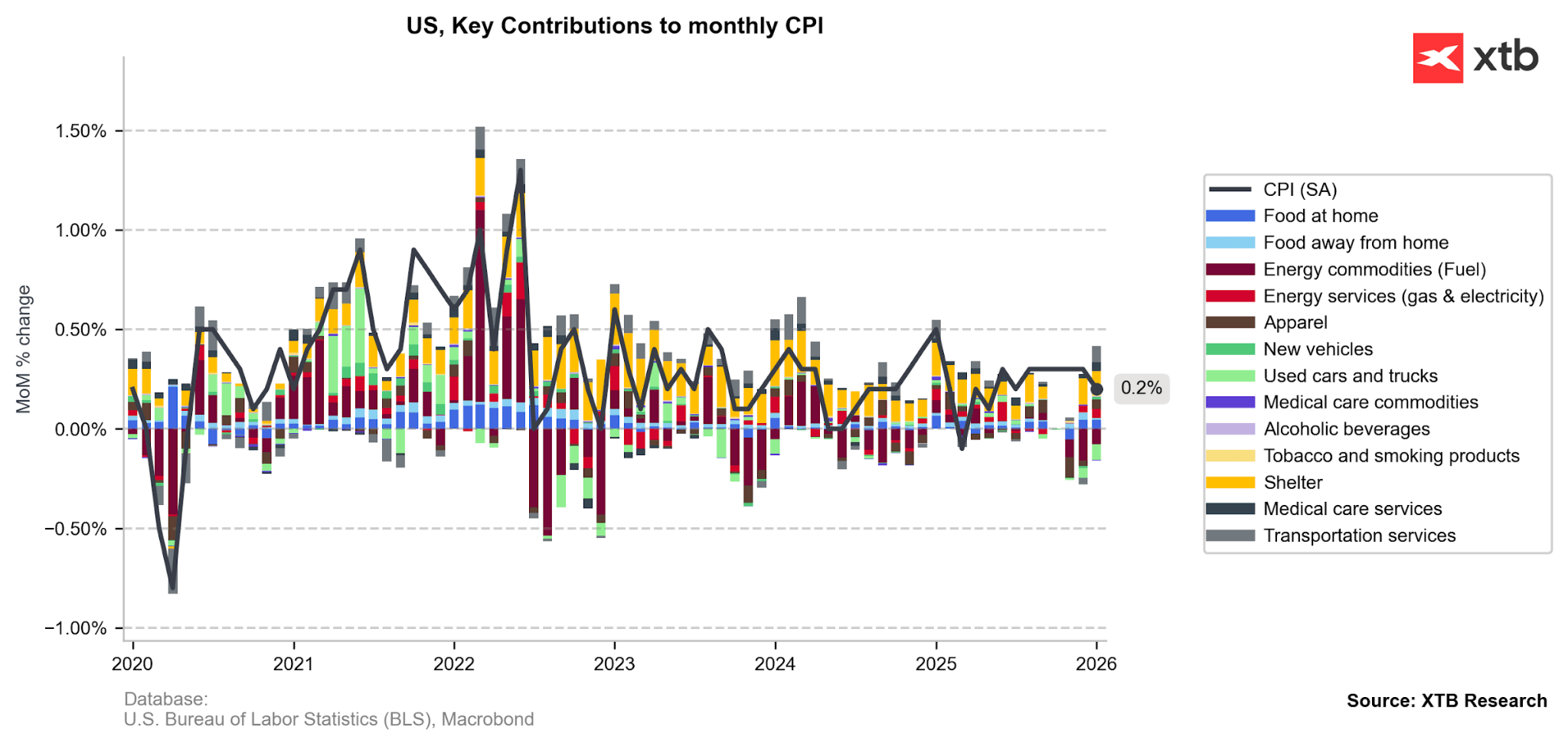

Energy Drag: Energy prices saw a sharp reversal, falling 1.5% MoM in January after a 0.3% increase in December. This was primarily driven by Gasoline, which plunged 3.2% during the month.

-

Service Stickiness: The services sector remains a primary driver of inflation, rising 0.4% MoM. Notably, Airline Fares surged by 6.5%, significantly accelerating from December's 3.8% increase.

-

Housing & Shelter: There was a notable deceleration in the housing sector price; Shelter grew by 0.2% MoM, down from the 0.4% pace seen in December.

-

Overall Goods Deflation: Used Cars & Trucks continued to decline, dropping 1.8% MoM. Conversely, Apparel saw a modest uptick of 0.3% following a flat reading previously.

-

Tariffs Are Still Creeping In: Conversely, tariff-sensitive categories showed marked price increases during this period. Costs for furnishings rose by 0.7%, while appliances—such as washing machines—increased by 1.3%. Even sharper growth was recorded in video and audio equipment (+2.2%) and the computers and software segment, which surged by 3.1%.

Shelter component has been persistently the key driver of consumer inflation, so its falling share in the newest CPI print should encourage the discussion around the interest rate cuts. The expected further drop in oil prices should also sustain a disinflationary effect of energy commodities and possibly limit the volatility of airfares. Source: XTB Research

Implications for Fed

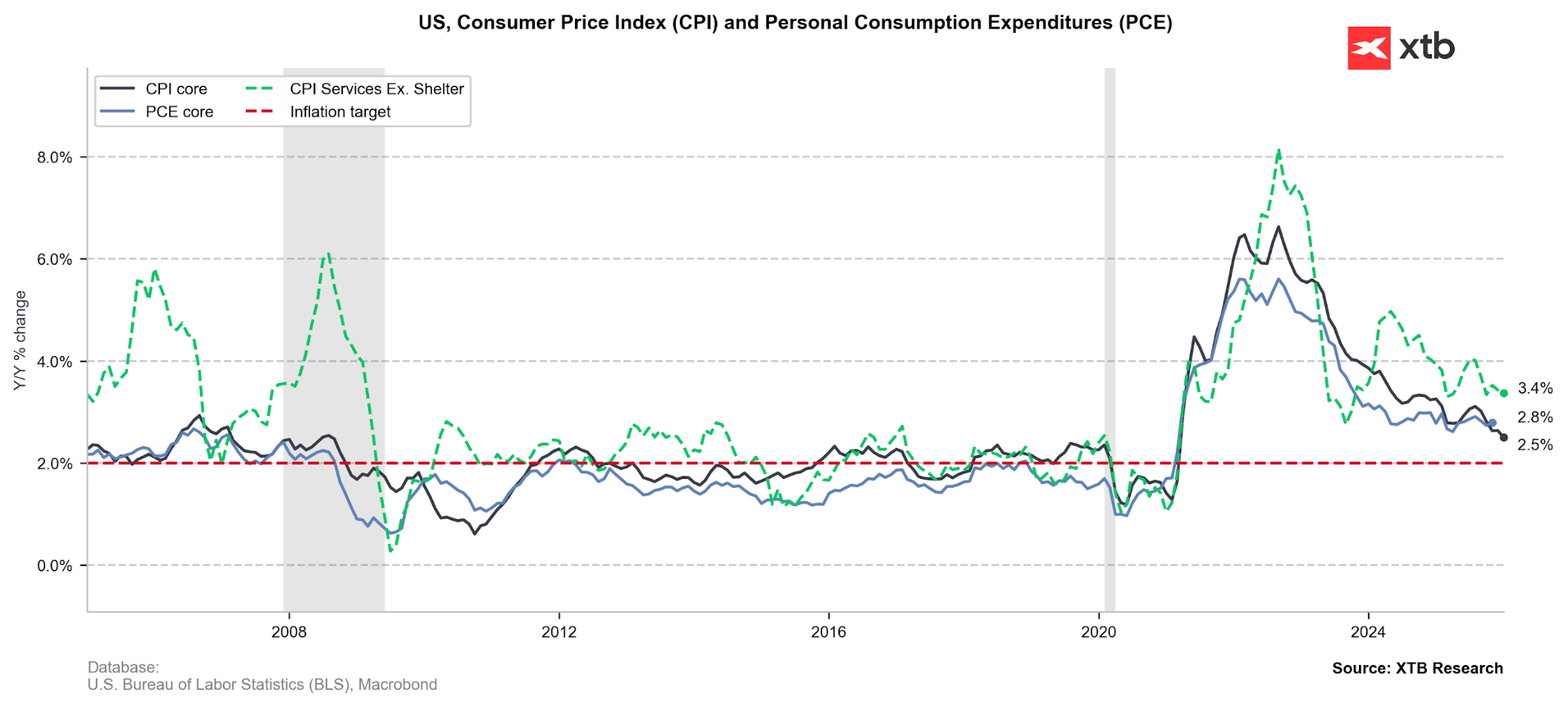

The latest inflation data provides the FOMC with significant breathing room to discuss the potential return of monetary easing rather than feeling pressured to rush into it. The cooling of the headline rate is largely supported by a sharp drop in gasoline prices and subdued food inflation, which should help keep consumer inflation expectations firmly anchored. Furthermore, the deceleration in shelter costs to a 0.2% monthly pace offers the most robust relief yet for the core services sector.

Nevertheless, more hawkish committee members are likely to keep their guard up due to "sticky" core dynamics and clear inflationary pressures in tariff-sensitive goods. Ultimately, the combo of progressing disinflation and a comfortable labour market data grants the Federal Reserve the space to adjust freely to risks on both sides of their mandate, which currently appear relatively low

Overall lower services inflation should encourage the discussion around further rate cuts. Source: XTB Research

Market Reaction

U.S. Treasuries experienced a significant rally, with 10-year yields falling to their lowest in 3 months (currently around 4.06%).

The futures on 10Y Treasury Notes are at their highest since early December 2025. Source: xStation5

According to the Federal Funds Futures, the short-term rate cut expectations remain well-anchored, with implied probabilities for the first half of 2026 remaining broadly unchanged (approx. 10% for March, 35% for April and 90% for June). The longer end, however, turned more dovish, with markets currently pricing 2.56 rate cuts before the end of 2026, compared to 2.3 a week ago.

Source: Bloomberg Finance LP

CPI report capped today’s strength in the dollar, clearing all the gains in the USDIDX, although the overall volatility in the FX caused by the print was limited.

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.