Ethereum's transition to Proof of Stake is imminent which temporarily improves sentiment in the cryptocurrency market. The improvement, however, still seems to be bypassing Bitcoin, which may prove to be a sleeping giant and will again cool demand if it moves south:

- Bitcoin remains below $20,000, Ethereum has risen above $1,600;

- Ethereum is undergoing its last Bellatrix update today before 'Merge' . As part of it, the Beacon chain will merge with the ETH mainnet, the consensus algorithm will be changed to PoS. The developers have not reported any bug so far, which the market received positively. The next update will already take place during the 'merge' and it will be the 'Paris Upgrade'.

- Ethereum's network throughput will increase to 1,000 or 1,500 transactions per second in real terms, from the current 20. Ultimately, Ethereum is expected to be able to process 100,000 transactions per second;

- After the completion of the Merge, which still looks risky, the Ethereum project will be 80% finished according to information from the developers' website;

- Miners mining Bitcoins with so-called 'diggers' have been hit by a spike in electricity prices. Bitcoin's crypto minig yield has fallen nearly 70% since the beginning of the year and is at 2020 lows, according to Bitinfocharts. Rising electricity prices may weigh on the activity of miners in cryptocurrency ecosystems based on the PoW 'Proof of Work' consensus method;

- Short-term addresses aggressively accumulated Bitcoin between June and August by making the current Bitcoin price volatility a test of the conviction of the most willing investor group. If this proves insufficient to stem declines and the group contributes to increased supply, a further downward price reaction remains unlikely.

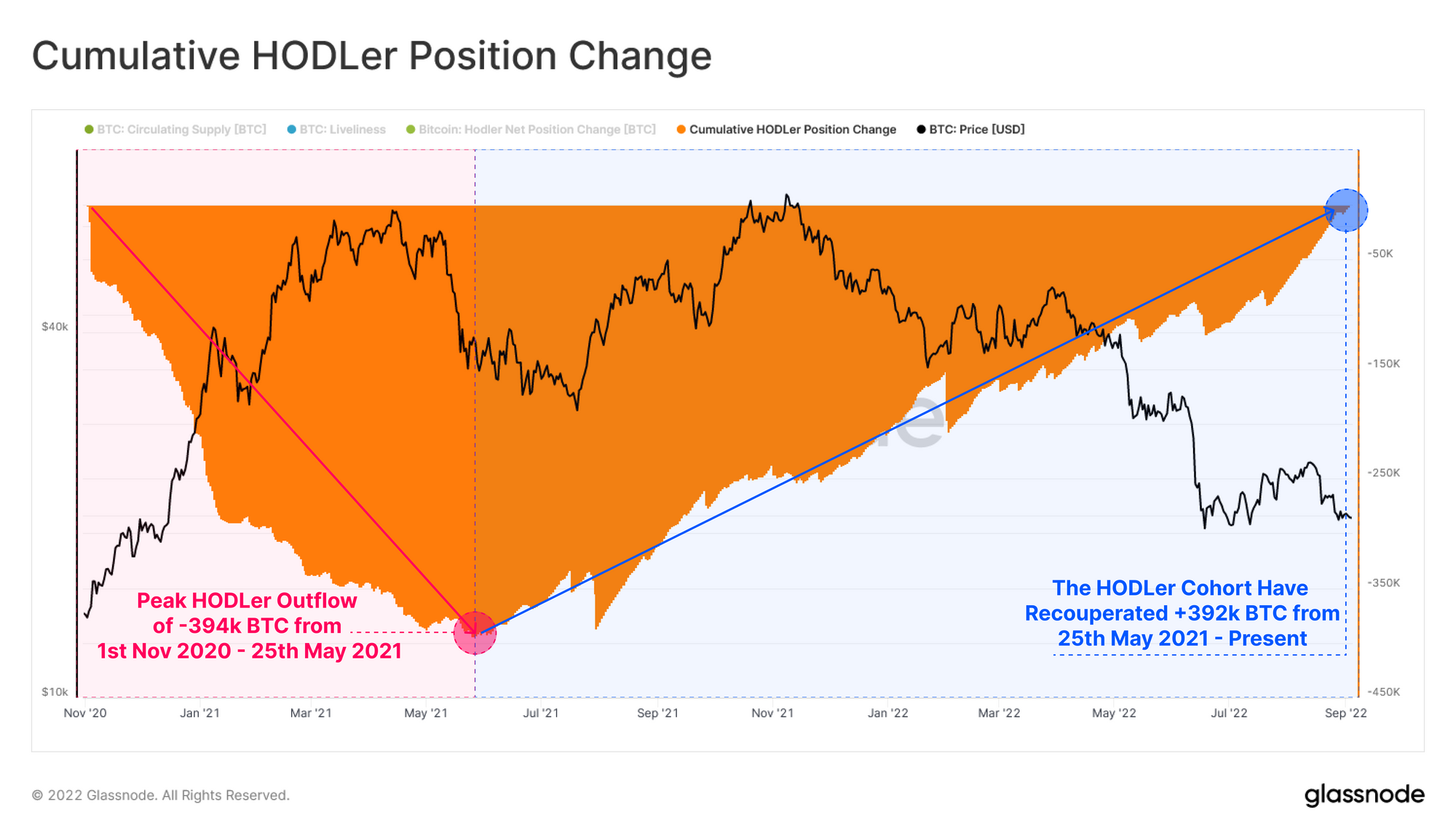

The chart shows the cumulative net inflows and outflows (supply and demand) from so-called HODLers, i.e., addresses holding Bitcoins purchased by addresses that have not disposed of reserves for at least the past six months. Over the course of November 2020 and May 2021, registered sales of 394,000 BTC held by long-term holders who aggressively sold during the bull market. From May 2021 to September 2022, we noted the impact of 394 thousand BTC, which 'patched' the hole left by the previous distribution. The accumulation of HODLers confirms the still relatively strong belief in Bitcoin's future among investors with potentially the highest level of conviction and experience. The market probably needs to test the conviction level of short-term traders, who were particularly aggressive in their purchases between June and September this year. Source: Glassnode

The chart shows the cumulative net inflows and outflows (supply and demand) from so-called HODLers, i.e., addresses holding Bitcoins purchased by addresses that have not disposed of reserves for at least the past six months. Over the course of November 2020 and May 2021, registered sales of 394,000 BTC held by long-term holders who aggressively sold during the bull market. From May 2021 to September 2022, we noted the impact of 394 thousand BTC, which 'patched' the hole left by the previous distribution. The accumulation of HODLers confirms the still relatively strong belief in Bitcoin's future among investors with potentially the highest level of conviction and experience. The market probably needs to test the conviction level of short-term traders, who were particularly aggressive in their purchases between June and September this year. Source: Glassnode

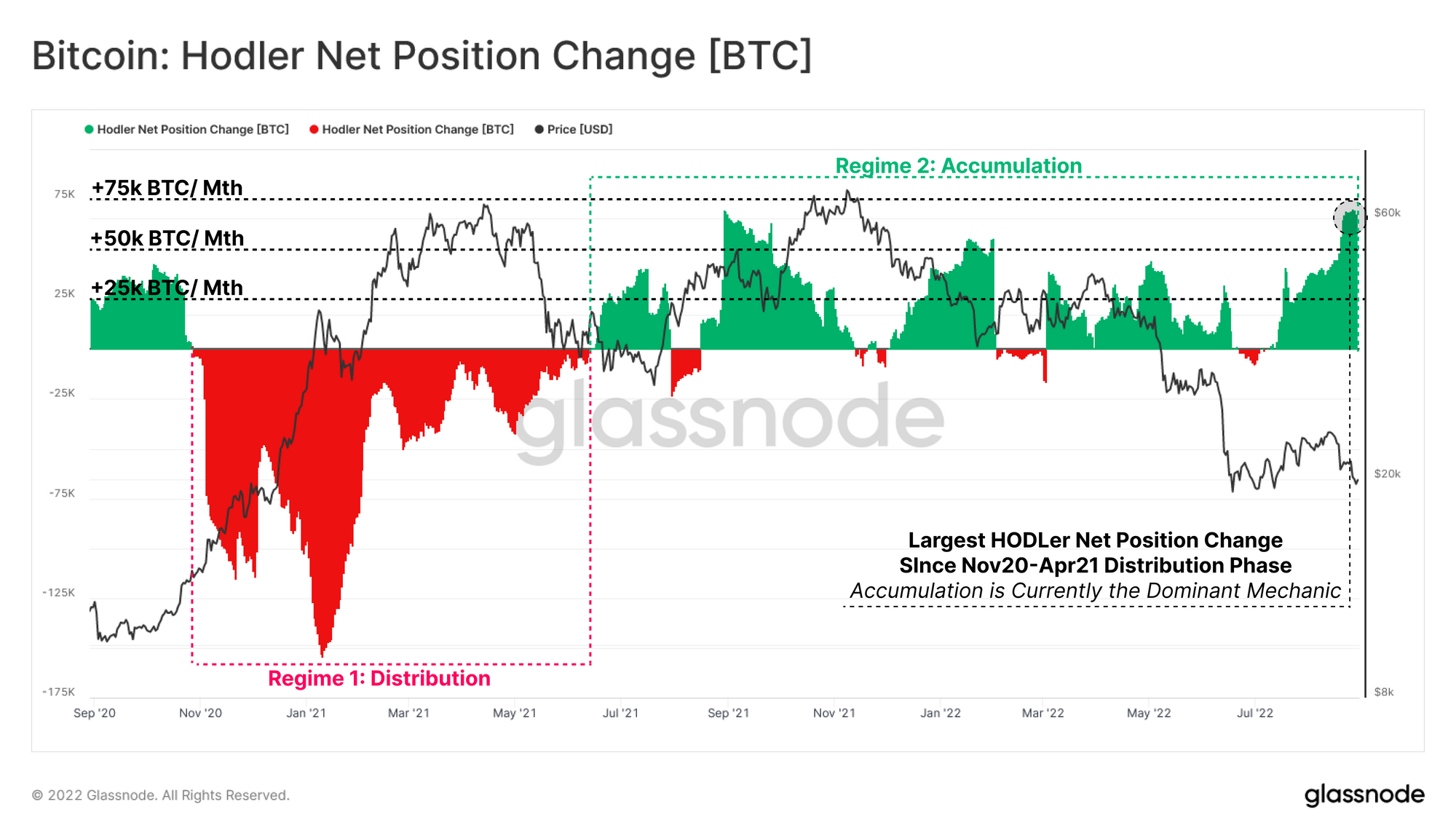

The chart shows the change in net position of HODLers. This metric can be used to verify the monthly change in HODLed supply, with two potentially interesting phases during this cycle. At its peak in November 2020 and April 2021, HODLers disposed of as much as 150,000 BTC per month. HODLers accumulated tokens throughout the second half of 2021 and continue to do so to the present. We are now seeing record Bitcoin accumulation by HODLErs at up to 70 thousand BTC per month, which is the largest monthly change in the position of this group of holders since March 2020, when we were observing pandemic-induced declines. Source: Glassnode

The chart shows the change in net position of HODLers. This metric can be used to verify the monthly change in HODLed supply, with two potentially interesting phases during this cycle. At its peak in November 2020 and April 2021, HODLers disposed of as much as 150,000 BTC per month. HODLers accumulated tokens throughout the second half of 2021 and continue to do so to the present. We are now seeing record Bitcoin accumulation by HODLErs at up to 70 thousand BTC per month, which is the largest monthly change in the position of this group of holders since March 2020, when we were observing pandemic-induced declines. Source: Glassnode

Bitcoin chart, H4 interval. The price of Bitcoin has been consolidating in a sideways trend for nearly 2 weeks, which in the past has usually heralded an upcoming big price move. Source: xStation5

Bitcoin chart, H4 interval. The price of Bitcoin has been consolidating in a sideways trend for nearly 2 weeks, which in the past has usually heralded an upcoming big price move. Source: xStation5 Chart of Ethereum, H4 interval. Ethereum is doing noticeably better than Bitcoin, although the RSI is dangerously fast approaching levels at 70 points, which in the past have usually heralded an impending correction. Source: xStation5

Chart of Ethereum, H4 interval. Ethereum is doing noticeably better than Bitcoin, although the RSI is dangerously fast approaching levels at 70 points, which in the past have usually heralded an impending correction. Source: xStation5

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Crypto News: Bitcoin Ignores Optimism On Wall Street. Is the Crypto Bull Market Ready to Return?

Morning Wrap: Wall Street Returns to the Offensive as Palantir Fuels AI Optimism

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.