We have passed another trading day where market volatility was heavily dominated by headlines coming out of the Middle East.

Global Stock Markets

W godzinach porannych w globalnych serwisach przewodziły doniesienia odnośnie kolejnego ostrzału sił amerykańskich oraz odwetu ze strony Iranu, co doprowadziło do wzrostów cen surowców energetycznych oraz pogorszenia sentymentu względem ryzyka. Z tego też względu na czerwono dzień zamknęły kluczowe europejskie indeksy.

- The French CAC40 fell by 0.2%.

- The German DAX dropped by 0.3%.

- The pan-European STOXX 600 declined by 0.5%.

- The British FTSE 100 shed 0.8%.

These declines were primarily supported by morning reports regarding the continuation of US shelling directed at Iran.

The US stock market began the day with minor losses but is finishing it with a substantial rally. The main catalyst behind the upward moves on Wall Street is the positive news regarding negotiations between the US and Iran, which broke around 4:00 PM. According to a report by Axios, a tentative agreement has been reached on a 60-day memorandum—it currently awaits approval from President Trump and Ayatollah Khamenei.

- The NASDAQ Composite is recording a gain of 0.8%

- The S&P 500 is rising by 0.6%

Geopolitics

The US continued its strikes against Iran, shooting down four drones and hitting an Iranian ground control station in Bandar Abbas. United States Central Command (CENTCOM) once again framed the shelling as a "defensive action"—stating the drones posed a threat to US forces and commercial shipping near the Strait of Hormuz.

Iran chose to retaliate this time by launching a ballistic missile at a US airbase in Kuwait. Kuwait intercepted the missile; no casualties or damage were reported. The Islamic Revolutionary Guard Corps (IRGC) warned of a "more decisive response" in the event of further US aggression.

Crucially, however, after 4:00 PM Axios reported that the US and Iran had reached an agreement on a 60-day memorandum, which still requires Donald Trump's signature. The deal would reportedly involve an extension of the ceasefire, during which the Strait of Hormuz would be reopened. Iran would be allowed to freely sell crude oil, and the parties would conduct negotiations aimed at limiting the Iranian nuclear program.

Under the terms, Iran would commit to not pursuing nuclear weapons and enter negotiations to suspend enrichment and remove its stockpiles of highly enriched uranium. Both Trump and mediators have suggested that an announcement could come this Sunday. However, the agreement has not yet been finalized and could still fall through.

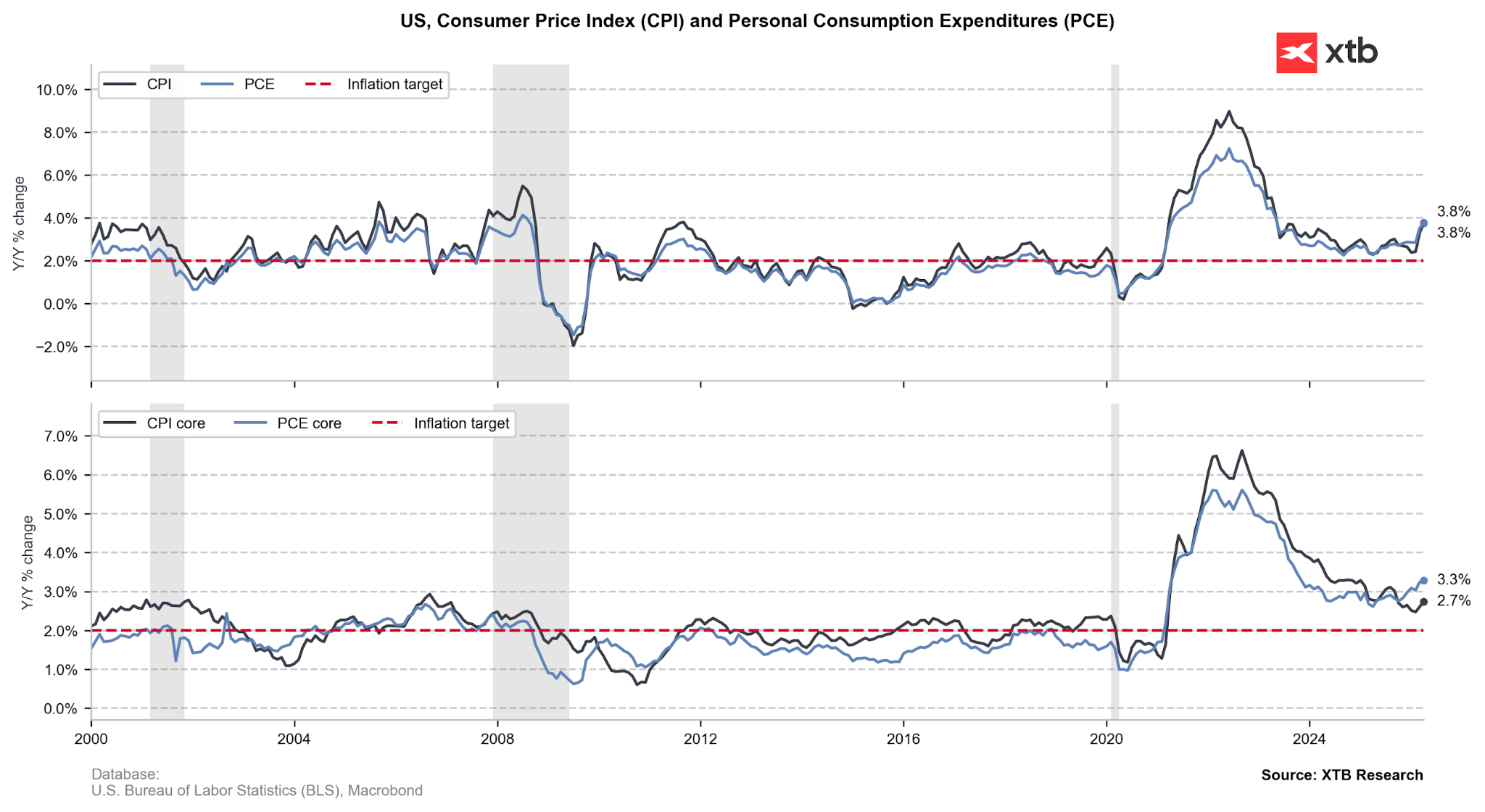

Macroeconomic Data

Investors anxiously awaited the release of a batch of key US data scheduled for 2:30 PM. However, these figures did not trigger any major surprises and were quickly overshadowed by the subsequent news from the Middle East. Nonetheless, based on today’s readings, we can draw at least three conclusions:

- The American consumer is weakening: Household income is growing at a very slow pace, meaning that any increase in spending is occurring primarily at the expense of savings, which are declining at an alarming rate.

- Inflation may (but does not have to) prove problematic: The savings rate is falling dynamically (reaching 2.6% in April), which could lead to increased price elasticity of demand. This would limit the room for manufacturers to hike prices in the face of rising production costs.

- The market is hunting for any arguments against FOMC rate hikes: Today's data does not come as a major surprise. In essence, it confirms what we have been observing in the US economy for several weeks, and in some cases, even months. However, this did not stop markets from scaling back their expectations for Fed interest rate hikes. The probability of an upward move before the end of the year currently stands at approximately 55%.

Figure 1: US CPI & PCE Inflation (2000 - 2026)

Source: XTB Research, 28.05.2026

Source: XTB Research, 28.05.2026

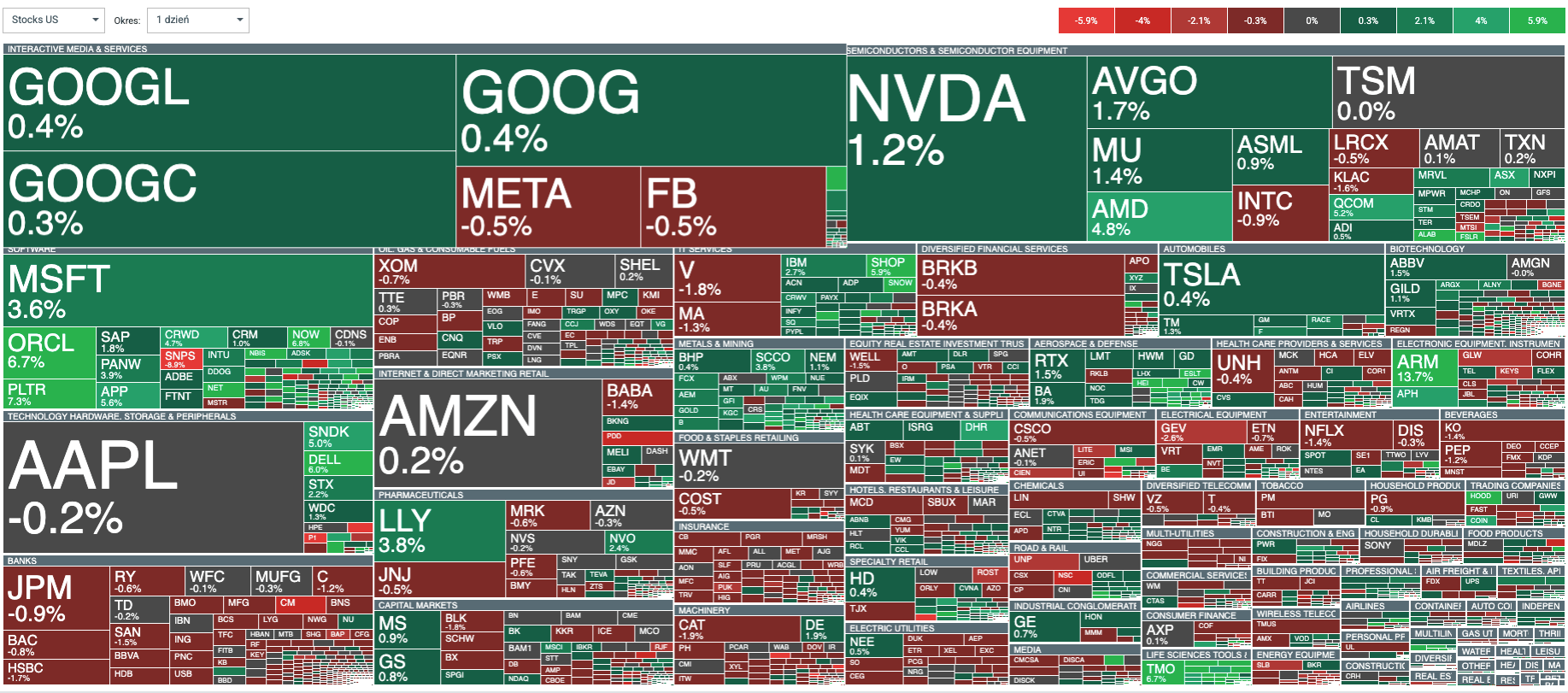

News from companies

Gains in the United States are being led by the technology sector. Notable gainers include Oracle (+6.7%), Palantir (+7.3%), and AMD (+4.8%).

Figure 2: Heatmap of the Day's Winners and Losers on the US Stock Market (28.05.2026)

Source: xStation, 28.05.2026

Source: xStation, 28.05.2026

Ford is also continuing its winning streak, with its shares rallying by 32.6% over the past month. The catalyst is a fundamental shift in the investment narrative: Ford Energy, after signing a five-year framework contract with EDF Power Solutions, expects further contracts with the utility sector and hyperscalers. Morgan Stanley rated the deal as the first major commercial victory for the division.

Following the publication of Q1 results, substantial gains are also being recorded by:

- Dollar Tree (DLTR.US): The company is posting the strongest rally in the entire S&P 500 index today. Shares are surging by 19% on the back of fantastic Q1 results. Adjusted earnings per share (EPS) came in at $1.74, beating the consensus by over $0.20. Revenue increased by 7.2% YoY, and the gross margin expanded by 1.2 percentage points.

- Best Buy (BBY.US): Near the top of today's leaderboard is the leading American consumer electronics retailer. An 18% jump can also be attributed to its Q1 fiscal results. Adjusted EPS came in at $1.28 versus the expected $1.22, while revenue reached $8.94 billion against a consensus of $8.83 billion. Comparable store sales grew by 2% YoY, driven predominantly by gaming consoles, computers, and mobile phones.

Commodities

- Gold & Silver: A decline in US bond yields is supporting an increase in the price of precious metals, with gold up 1.2% and silver gaining 1.7%.

- Brent Crude Oil: Down 0.6%. The decline is driven by the Axios reports regarding the approaching agreement between the US and Iran.

- NATGAS: Up 5.8%. The net build in natural gas inventories for the week ending May 22 came in lower than expected at 92 billion cubic feet (Bcf). Additionally, weather forecasts for the coming weeks were recently revised upward.

---

Michał Jóźwiak, Financial Markets Analyst at XTB

France Challenges Palantir, Market Reacts.

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.