- European equity markets ended the session higher — Germany’s DAX gained nearly 1%. Sentiment around the European stocks improved on hopes of a potential end to the war in Ukraine. Earlier, NBC News reported — citing sources within the U.S. administration — that the Ukrainian delegation had agreed to the terms of a U.S.-backed peace proposal. Meanwhile, shares of German defense manufacturer Rheinmetall fell to their lowest levels since April, reflecting weakening momentum across the defense sector.

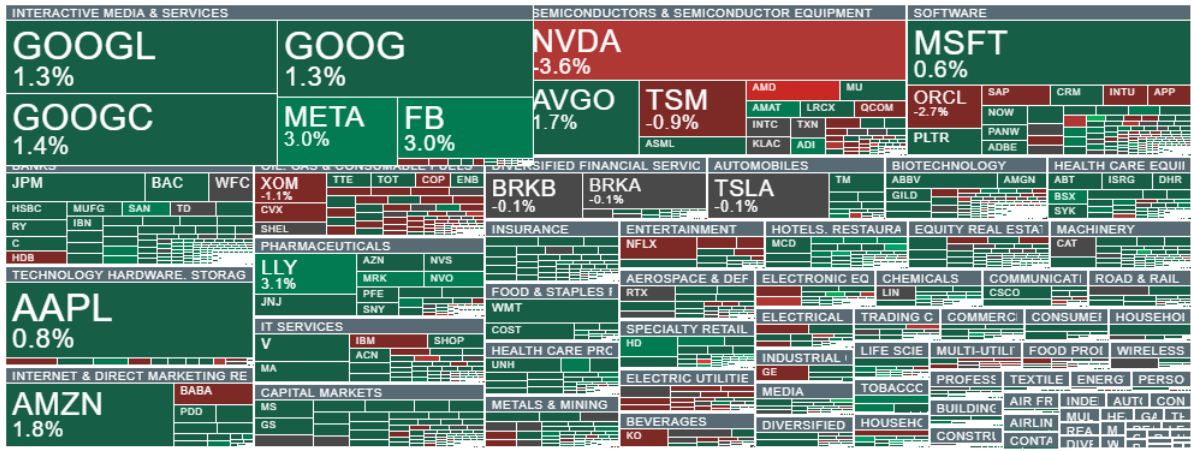

- Market sentiment on Wall Street continues to show a strong appetite for gains, despite Nvidia’s shares initially plunging nearly 7%. The decline in NVDA has now eased to around 3%, and the tech sector is rebounding; losses in Taiwan Semiconductor, AMD and Oracle have also slowed. Meta Platforms and Eli Lilly are trading higher, while Alphabet has reached new all-time highs. Nearly all equity sectors are in the green.

- Semiconductor stocks reacted negatively to reports that Meta is considering using Google’s TPU chips instead of Nvidia’s GPUs. This narrative struck at Nvidia’s perceived “monopolistic” market position and boosted optimism around Alphabet, which, alongside Broadcom, is increasingly viewed as a major challenger to Jensen Huang’s company.

The U.S. dollar is weakening today following soft retail sales data and a drop in consumer sentiment in the Conference Board survey. Wall Street is increasing its bets on a December rate cut, and EURUSD is up 0.4%, rebounding from key support at the 200-day EMA and testing the 1.158 area. Below is today’s U.S. macro data:

-

Conference Board Consumer Confidence: 88.7 (Forecast: 93.3, Previous: 94.6, Revised: 95.5)

-

Pending Home Sales Index: 76.3 (Forecast: –, Previous: 74.8, Revised: 71.8)

-

Retail Sales YoY: 4.3% (Forecast: –, Previous: 5.0%)

-

PPI YoY: 2.7% (Forecast: 2.6%, Previous: 2.6%)

-

Core PPI MoM: 0.1% (Forecast: 0.2%, Previous: -0.1%)

-

Core PPI YoY: 2.6% (Forecast: 2.7%, Previous: 2.8%)

-

PPI MoM: 0.3% (Forecast: 0.3%, Previous: -0.1%)

-

Core Retail Sales MoM: 0.3% (Forecast: 0.3%, Previous: 0.7%, Revised: 0.6%)

-

Retail Sales MoM: 0.2% (Forecast: 0.4%, Previous: 0.6%)

-

Business Inventories MoM: 0% (Forecast: 0%, Previous: 0.2%)

-

Pending Home Sales Change MoM: 1.9% (Forecast: 0.2%, Previous: 0.0%, Revised: -0.1%)

-

Richmond Fed Manufacturing Index: -15 (Forecast: -5, Previous: -4)

-

House Price Index YoY: 1.7% (Forecast: –, Previous: 2.3%)

-

House Price Index MoM: 0% (Forecast: 0.2%, Previous: 0.4%)

-

Case-Shiller 20-City Index YoY: 1.36% (Forecast: 1.4%, Previous: 1.6%)

-

Redbook YoY: 5.9% (Previous: 6.1%)

- ICE coffee futures are rising for the third consecutive session, rebounding after the recent sell-off. The main driver behind the rally is drought in Brazil’s key growing region, Minas Gerais, where rainfall is only around 50% of the historical average.

- Natural gas futures are down more than 2.5% as forecasts for cold weather across many U.S. states have eased, though they are recovering part of earlier losses after dropping over 4.5% in the afternoon.

- Cryptocurrency prices are falling despite improving sentiment in equity markets. Bitcoin is holding around $87,000 and has failed to climb back above $90,000 despite a solid stock market rebound. Ethereum is trading just below $2,900.

- Scott Bessent noted that hearings for Federal Reserve chair candidates are still underway; the White House intends to complete them before the holidays. According to anonymous sources, Kevin Hassett—considered loyal to Donald Trump—has recently gained the upper hand.

- Trump stated that a peace agreement between Russia and Ukraine is “close,” while Ukraine’s President Zelensky expressed his willingness to meet with the U.S. President as soon as possible.

- FedEx shares are up nearly 3% today; the company will invest $200 million to modernize its logistics hub in Anchorage, Alaska — including a new sorting facility and additional aircraft parking capacity.

Source: xStation5

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.