European markets closed on a mixed note. Germany's DAX fell 0.5%, the Euro Stoxx 50 lost more than 0.2%, while France's CAC 40 gained 0.2%, supported by a strong rebound in luxury stocks. The sector outperformed after luxury giant Compagnie Financière Richemont reported strong results, sending its shares more than 6.5% higher.

U.S. equities are enjoying another solid session today, although the Nasdaq 100 is down less than 0.2% despite an initially sharp selloff in AI-related stocks. The S&P 500 is up 0.3% and is moving closer to the 7,600-point mark, while the Dow Jones remains near record highs. June producer price inflation came in below expectations, and together with strong corporate earnings and a rally in ASML shares, helped support risk assets.

- June PPI (MoM): -0.3% (Expected: 0.0%; Previous: 0.6%)

- June PPI (YoY): 5.5% (Expected: 6.2%; Previous: 6.0%)

- Core PPI (MoM): 0.2% (Expected: 0.3%; Previous: 0.4%)

- Core PPI (YoY): 4.7% (Expected: 5.2%; Previous: 4.9%)

Another U.S. inflation report surprised to the downside. Producer prices declined 0.3% month over month, while both headline and core annual inflation measures slowed more than expected, reinforcing yesterday's softer-than-expected CPI report.

Today's gains on Wall Street are being led by shares of Meta Platforms, Alphabet, Microsoft, Apple, Amazon, and Oracle, potentially signaling a gradual shift in investor sentiment and a rotation of capital away from AI infrastructure suppliers toward the Magnificent Seven. Bank stocks are also performing strongly, supported by another round of record earnings, with the broader financial sector led by BlackRock. Shares of the asset management giant are up more than 6% after the company beat expectations on revenue, earnings, and assets under management (AUM), which reached a record $15.3 trillion.

The U.S. Dollar Index is trading lower today, approaching the 100 level, while EUR/USD is up 0.5% to 1.147. Bitcoin has climbed back above $65,000, extending its rebound and gaining roughly 10% from its recent lows.

The Bank of Canada (BoC) left its benchmark interest rate unchanged at 2.25%, in line with market expectations. Policymakers said the current level of interest rates remains appropriate to support the economic recovery. The central bank lowered its 2026 GDP growth forecast to 0.7% from 1.2%, while raising its 2027 growth projection to 1.8% from 1.6%. It also increased its estimate for second-quarter annualized GDP growth to 2.5%, following a 0.1% contraction in the first quarter.

The BoC expects economic growth to gradually accelerate through 2027 and 2028. It forecasts inflation to slow to around 2.5% in the second half of 2026 before returning to its 2% target in early 2027. The central bank also noted that long-term business inflation expectations remain well anchored, while Canada's labor market continues to be weak but broadly stable.

The latest EIA report delivered mixed signals for the energy market. U.S. crude oil inventories fell by 1.69 million barrels, slightly more than expected, while gasoline inventories also declined by 1.53 million barrels. However, distillate inventories unexpectedly increased by 4.56 million barrels despite forecasts calling for a decline. Oil and natural gas prices are trading broadly flat today, although crude oil remains up more than 7% over the past week.

The Federal Reserve's Beige Book indicated that U.S. economic activity continued to expand between mid-May and early July, although growth was generally modest to moderate, with several districts reporting little or no growth. Consumer spending remained under pressure from higher prices, particularly for fuel, while demand for services continued to increase.

The labor market remained stable, with employment rising modestly across most Federal Reserve districts. However, businesses continued to report difficulties finding skilled workers, particularly in construction, manufacturing, and retail. Wage pressures remained moderate, although wage growth eased in several regions.

Some companies also reported increasing use of artificial intelligence in hiring processes and to improve employee productivity. Most districts continued to report rising costs and prices, particularly in services, construction, and manufacturing, with some businesses passing higher costs on to customers. Labor market contacts cited by the Fed remained cautiously optimistic about further economic growth but highlighted persistent cost-related uncertainty and expect inflation to ease only gradually.

U.S. equities are enjoying another solid session today, although the Nasdaq 100 is down less than 0.2% despite an initially sharp selloff in AI-related stocks. Those losses have been largely offset by a rebound in Big Tech shares. The S&P 500 is gaining 0.3% and moving closer to the 7,600-point mark, while the Dow Jones remains near record highs. June producer price inflation came in below expectations, and together with strong corporate earnings and a rally in ASML shares, helped support risk assets.

- June PPI (MoM): -0.3% (Expected: 0.0%; Previous: 0.6%)

- June PPI (YoY): 5.5% (Expected: 6.2%; Previous: 6.0%)

- Core PPI (MoM): 0.2% (Expected: 0.3%; Previous: 0.4%)

- Core PPI (YoY): 4.7% (Expected: 5.2%; Previous: 4.9%)

Another U.S. inflation report surprised to the downside. Producer prices fell by 0.3% month over month, while both headline and core annual inflation measures slowed more than expected, reinforcing yesterday's softer-than-expected CPI report.

Today's gains on Wall Street are being led by Meta Platforms, Alphabet, Microsoft, Apple, Amazon, and Oracle, potentially signaling a gradual shift in investor sentiment and a rotation of capital away from AI infrastructure suppliers toward the Magnificent Seven. Bank stocks are also performing strongly, supported by another round of record earnings, with the broader financial sector led by BlackRock. Shares of the asset management giant are up more than 6% after the company beat expectations on revenue, earnings, and assets under management (AUM), which reached a record $15.3 trillion.

The U.S. Dollar Index is trading lower today, approaching the 100 level, while EUR/USD is up 0.5% to 1.147. Bitcoin has climbed back above $65,000, extending its rebound and gaining roughly 10% from its recent lows.

The Bank of Canada (BoC) left its benchmark interest rate unchanged at 2.25%, in line with market expectations. Policymakers said the current level of interest rates remains appropriate to support the economic recovery. The central bank lowered its 2026 GDP growth forecast to 0.7% from 1.2%, while raising its 2027 growth projection to 1.8% from 1.6%. It also increased its estimate for second-quarter annualized GDP growth to 2.5%, following a 0.1% contraction in the first quarter.

The BoC expects economic growth to gradually accelerate through 2027 and 2028. It forecasts inflation to slow to around 2.5% in the second half of 2026 before returning to its 2% target in early 2027. The central bank also noted that long-term business inflation expectations remain well anchored, while Canada's labor market continues to be weak but broadly stable.

The latest EIA report delivered mixed signals for the energy market. U.S. crude oil inventories fell by 1.69 million barrels, slightly more than expected, while gasoline inventories also declined by 1.53 million barrels. However, distillate inventories unexpectedly increased by 4.56 million barrels, despite forecasts calling for a decline. Oil and natural gas prices are trading broadly flat today, although crude oil remains up more than 7% over the past week.

The Federal Reserve's Beige Book indicated that U.S. economic activity continued to expand between mid-May and early July, although growth was generally modest to moderate, with several districts reporting little or no growth. Consumer spending remained under pressure from higher prices, particularly for fuel, while demand for services continued to increase.

The labor market remained stable, with employment rising modestly across most Federal Reserve districts. However, businesses continued to report difficulties finding skilled workers, particularly in construction, manufacturing, and retail. Wage pressures remained moderate, although wage growth eased in several regions.

Some companies also reported increasing use of artificial intelligence in hiring processes and to improve employee productivity. Most districts continued to report rising costs and prices, particularly in services, construction, and manufacturing, with some businesses passing higher costs on to customers. Labor market contacts cited by the Fed remained cautiously optimistic about further economic growth but highlighted persistent cost-related uncertainty and expect inflation to ease only gradually.

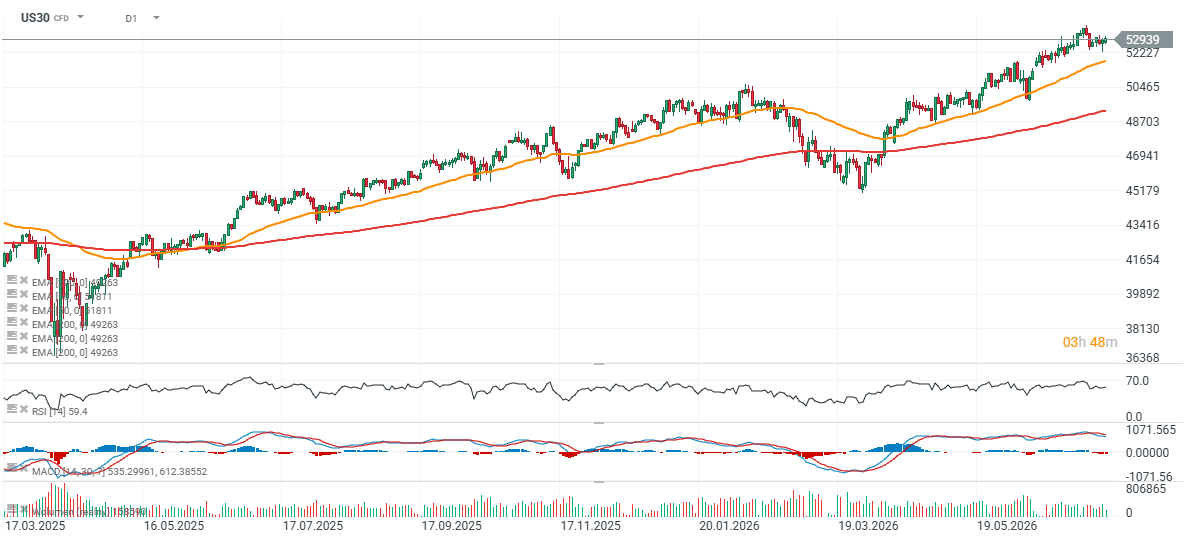

DJIA futures chart (US30, D1 interval)

The Dow Jones Industrial Average, which has greater exposure to traditional "old economy" companies, continues to outperform. DJIA futures are posting gains today, remaining largely unfazed by the weakness seen in the AI infrastructure sector.

Source: xStation5

Source: xStation5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.