- European markets recover from corrections, mostly due to Donald's Trump ease of rhetoric towards China

- European pharmaceuticals producers make a bid to circumvent tariffs

- Automakers stocks up despite difficult situation

- France's new government forming puts some of the investors at ease

- European markets recover from corrections, mostly due to Donald's Trump ease of rhetoric towards China

- European pharmaceuticals producers make a bid to circumvent tariffs

- Automakers stocks up despite difficult situation

- France's new government forming puts some of the investors at ease

The week on European stock exchanges clearly begins with gains. Most major indices in Western Europe are experiencing a solid rebound, which can be interpreted as a corrective rise following last week's declines. The German DAX, along with CAC40 and the Italian FTSE MIB, gains on opening by an average of over 1%.

Despite the lack of significant macroeconomic publications, today's session brings large price movements. It is evident that investors in Europe are again reacting mainly to events from across the ocean, but this time the sentiment is positive. Donald Trump has noticeably toned down his policy and statements regarding the trade war with China, which has significantly reduced market tension. Additionally, a certain impulse for local markets came from France, where a new government was formed at an express pace. The partial resolution of the political impasse reduces uncertainty and gives investors a small but noticeable reason for optimism.

Source: Bloomberg Terminal LP

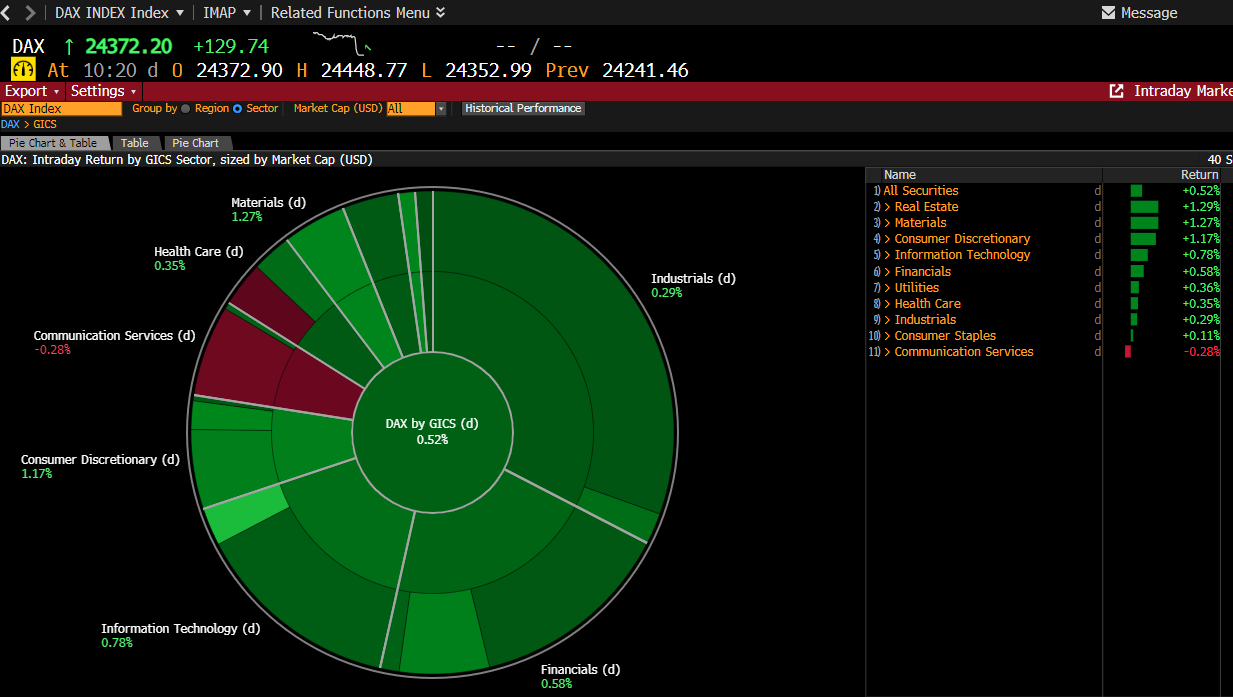

We are experiencing noticeable gains across whole sectors. Among the leaders of growth in Europe today are companies from the automotive sector, pharmaceutical firms, and the broadly defined IT sector.

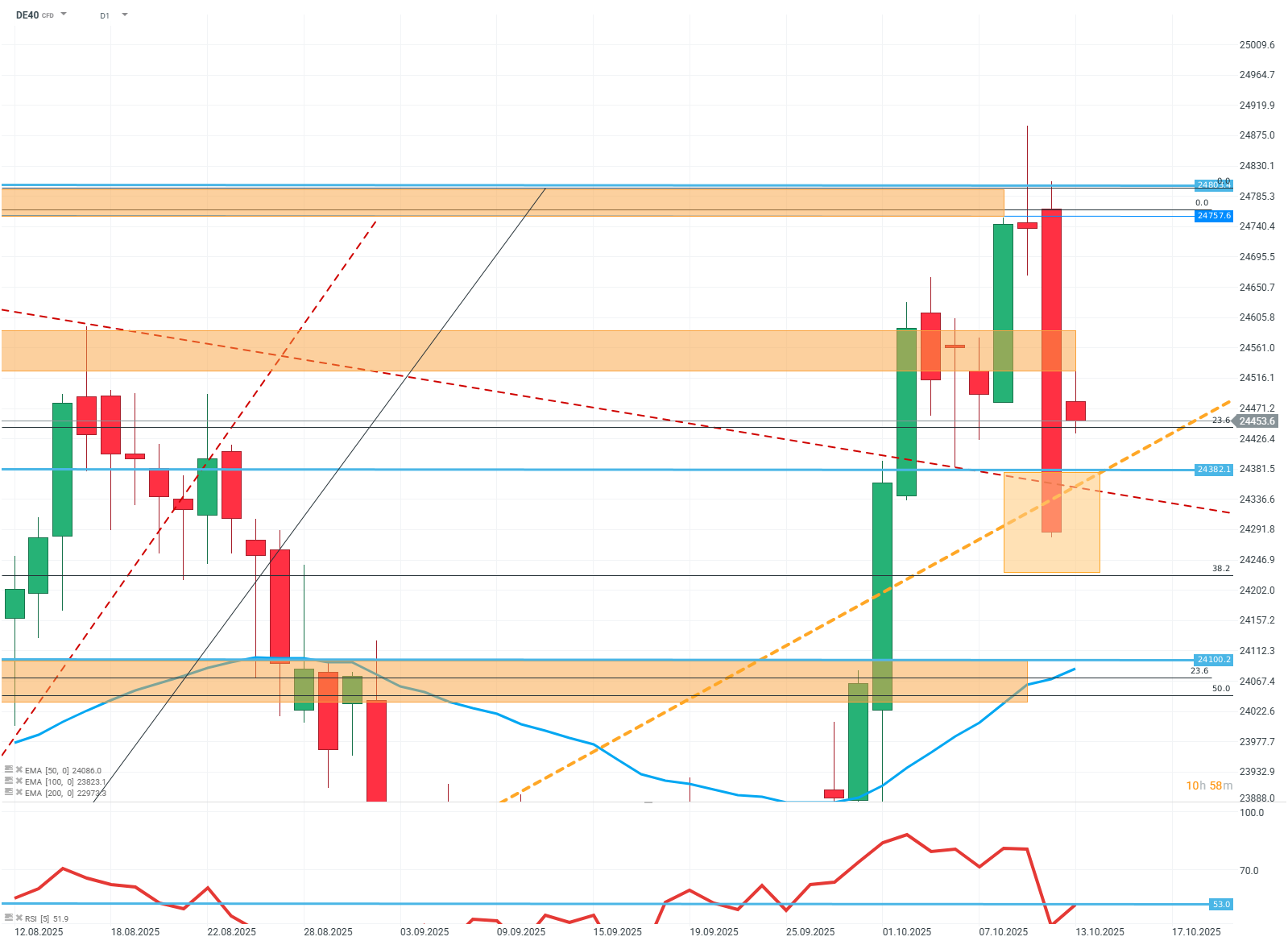

DE40 (D1)

Source: Xstation5

The chart shows that after bouncing off the levels of the last ATH, the index temporarily fell below the medium- and long-term trend lines (orange and red). However, a quick breakout above them confirmed their technical significance. Currently, the quotations are in the area of the FIBO 23.6% retracement of the last upward wave - which constitutes a key point of resistance/support. To maintain a positive scenario, it is necessary to defend the resistance around 24380 points, as its breach could initiate a correction towards 24100 points. The RSI indicator remains in the moderate valuation zone, suggesting neutral sentiment.

Company news:

SUESS MicroTec (SMHN.DE) — The semiconductor manufacturing company is up over 13% after receiving a positive recommendation from an investment bank.

Pharmaceutical companies have proposed supplies/discounts for the American healthcare system in exchange for tariff exemptions. Shareholders are mixed in their reactions. AstraZeneca (AZN.UK) is down about 1%. Sanofi (SNF.FR) is up about 0.5%, Novo Nordisk (NOVOB.DK) is down 2%.

PSI Software (PSAN.DE) - The software producer for energy manufacturers is up 34%, driven by the planned acquisition of the company by a private fund. This is a continuation of last week's movement, in which the company already rose by about 38%.

Despite few fundamental bases, automotive companies in Europe are experiencing a broad rebound. BMW(.DE) is up 1.7%, Stellantis (STLAM.IT) is up 2.3%.

Theon International (THEON.NL) - The Greek night vision manufacturing company announced the acquisition of shares in one of its French partners, with the stock price rising by over 8%.

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.