- Political turmoil hangs over the valuations

- The European military industry continues to move the markets

- British economy slows down, rate cuts expected

- European inflation in line with expectations

- Political turmoil hangs over the valuations

- The European military industry continues to move the markets

- British economy slows down, rate cuts expected

- European inflation in line with expectations

The European session is proceeding in a calm mood, with a predominance of moderate optimism. Most indices remain around the opening levels, but with slight increases. The growth leader is FTSE1000, whose contracts are rising by over 1.4% on the wave of new expectations regarding the interest rate path. ITA40 and NED25 contracts are up by 0.4%. DAX remains around the opening price of the quotations. Declines can be observed in French and Swiss indices, but they are limited to 0.3%.

Investors on the European market have a long series of political information and macroeconomic data to discount.

- Donald Trump threatens retaliation against European technology companies in response to fines against American corporations. The US president also threatens invasion of Venezuela again. This may generate additional volatility during the session or in the coming days.

- Germany is introducing a series of significant decisions that the market may interpret as growth-oriented. Firstly, the EU coalition voted for significant concessions in the law banning the sale of combustion vehicles. At the same time, Germany is withdrawing from a series of restrictions on electricity consumption by enterprises.

- KNDS — The German tank manufacturer is preparing IPO plans, and the company's management is expected to present a preliminary schedule for entering the public market by the end of this week.

Macroeconomic data:

- Inflation in the UK: The CPI reading turned out to be below expectations, reaching 3.2% year-on-year compared to the expected 3.4%. On a monthly basis, deflation was recorded at 0.2%. This provides more room for rate cuts by the BoE.

- The IFO index from Germany is below expectations, remaining in contraction territory at 87.6.

- Eurozone HCPI inflation was in line with market expectations, at 2.4% annually and -0.5% MoM.

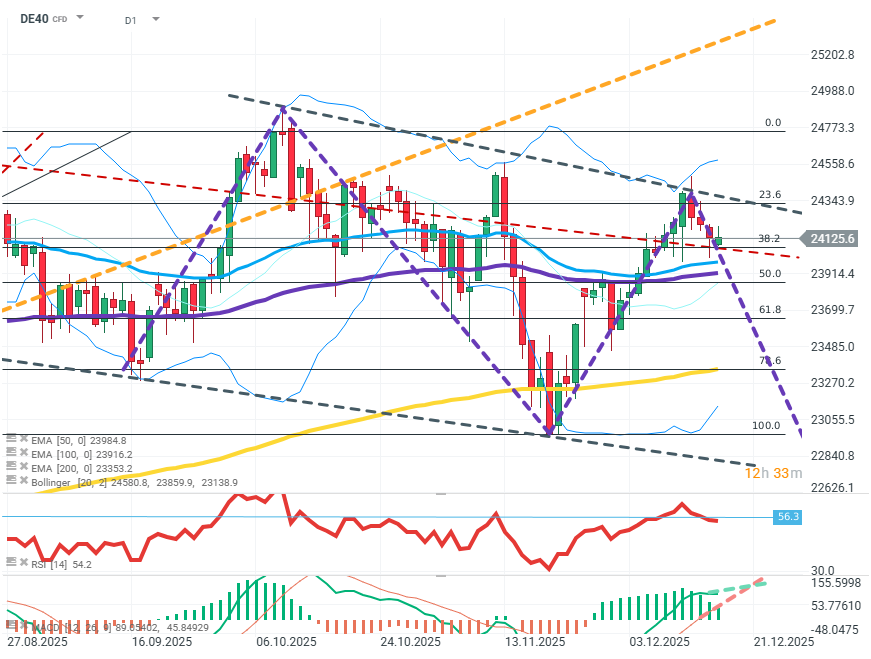

DE40 (D1)

Source: xStation5

The chart shows the continuation of the formation of a broad downward pattern with a low trend slope. The EMA average and MACD show a decreasing spread, indicating growing weakness among buyers, who need to break the FIBO 23.6 level to prevent further declines. If sellers want to maintain the initiative, it is crucial to quickly overcome the EMA 50 and 100 averages and then FIBO 50.

Company news:

- RENK (R3NK.DE), Rheinmetall (RHM.DE) - German defense companies are correcting part of the recent declines. This is a result of further failures in peace negotiations, NATO countries' purchases, and information about alleged, unannounced Russian military gatherings and exercises in Belarus. Valuations are rising by about 1.5-2.5%.

- Siemens Healthineers (SHL.DE) - The company announces that one of its owned startups is reporting progress in ongoing projects.

- Suedzucker (SZU.DE) - The food producer published a disappointing revenue growth forecast. The company is losing over 3%.

- Thyssenkrupp Nucera (NCH2.DE) - The company specializing in energy equipment published results above expectations and with good forecasts for the future. Shares are up by over 2%.

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.