In recent quarters, Nvidia has been almost synonymous with AI infrastructure for the market. Today it remains at the forefront of innovation and the efficiency of AI computing solutions, but even Nvidia is starting to run into technological constraints, at least according to analysts at SemiAnalysis.

In today’s AI industry, it is no longer enough to buy the best GPUs. Increasingly strong emphasis is being placed on complete, integrated computing systems, that is, fully built server racks where every component is designed from scratch, custom-made, and perfectly synchronized with the rest to maximize efficiency.

One such device that is expected to appear in Nvidia’s lineup is the “Kyber NVL144.”

According to analysts at SemiAnalysis, the Kyber NVL144 system could be pushed back by as much as about 12 months, from the planned 2027 to 2028. The reason is said to be a problem with producing a key component (the so-called PCB midplane, a multilayer intermediate board connecting modules inside the entire rack).

The market did not react to these reports with panic, and some analysts even dismissed them as “noise,” but the nature of the problem is more serious than it may seem to investors unfamiliar with technical issues. The information is significant enough that Nvidia representatives commented to Bloomberg, denying the rumors and reassuring that development of the system is proceeding according to plan.

That is precisely why SemiAnalysis reports about a possible delay to the Kyber NVL144 architecture matter. This is not about a cosmetic slip in the roadmap, but a signal that further AI scaling is starting to depend more and more on very down-to-earth engineering constraints.

Kyber NVL144 was meant to be one of the most ambitious elements of the next generation of AI infrastructure. The system, based on the Rubin Ultra architecture, was supposed to house as many as 144 GPUs in a single rack, while also offering integrated liquid cooling. Such a project was expected to deliver a huge performance increase and allow Nvidia to further expand the so-called “scale-up” domain, meaning the number of GPUs connected via the very fast, proprietary NVLink interconnect.

In the largest AI systems, it is not enough to have more chips. You also have to make them communicate with each other fast enough. So if Nvidia has a problem with Kyber, it is not just a problem with a single board. It is a problem with the next leap in the scale of the entire architecture, and with market expectations built on the breakthroughs the company is expected to deliver.

These reports also fit into the broader picture of the growing complexity of Nvidia’s roadmap. For competitors, this could be a potentially important window. SemiAnalysis suggests that a Kyber delay could improve the position of

AMD solutions or in-house chips designed by hyperscalers, such as Google’s TPU.

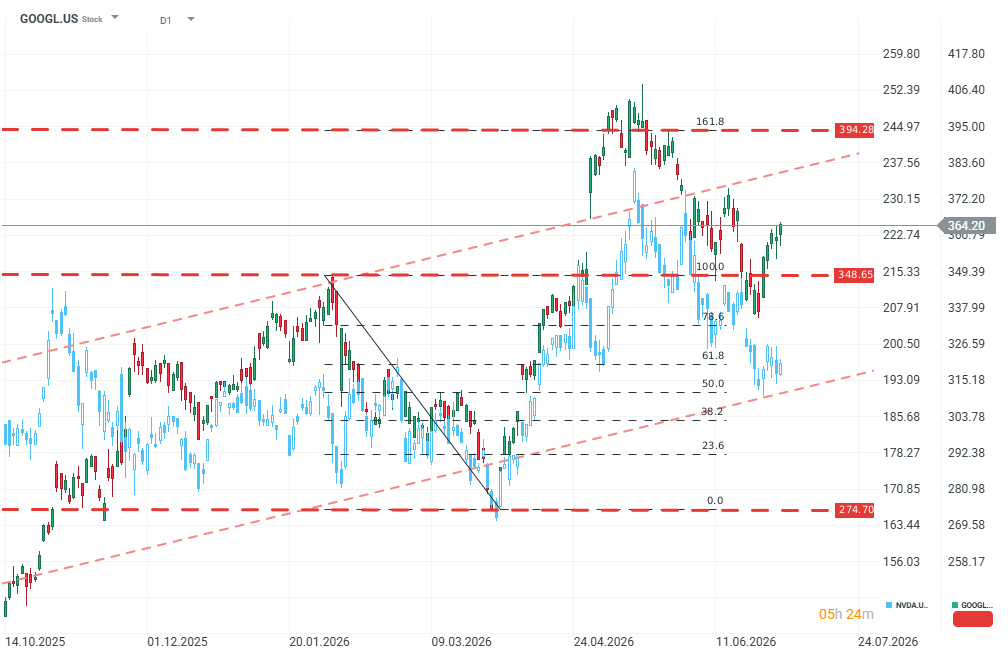

Analysis of Nvidia and Google price chart (NVDA.US/GOOGL.US) (D1)

Both companies move in a similar way, based on similar price impulses and broader market trends. However, the market is currently hard to convince that there are further growth catalysts for Nvidia, while Google is increasingly beginning to dominate in terms of the pace and scale of valuation growth, driven in part by many company initiatives aimed at vertical integration and reducing dependence on external suppliers. Source: xStation5

This does not automatically mean the end of Nvidia’s dominance in this segment, but if the analysts’ reports are confirmed, it could mean a major blow to the company’s long-term plans.

Texas Instruments earnings: Growth without cash

All or nothing: ServiceNow earnings preview

Did SaaS lost too much? Morgan Stanley says yes.

US OPEN: The market extends losses as investor concerns grow

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.