-

On a month-on-month basis, prices fell for the first time since 2020 – by as much as 0.4%.

-

Fuel prices are down 9.7% compared with May.

-

Crucially, the core measure remained unchanged month-on-month (0.0%), down year-on-year (2.6%).

-

The probability of an FOMC rate increase as early as September has fallen to around 66%.

-

One rate hike before the end of the year is now the baseline scenario.

-

The EUR/USD pair strengthened by 0.6%.

-

This is not the end of the volatility – Kevin Warsh’s first testimony before the US Congress is due at 3PM.

-

On a month-on-month basis, prices fell for the first time since 2020 – by as much as 0.4%.

-

Fuel prices are down 9.7% compared with May.

-

Crucially, the core measure remained unchanged month-on-month (0.0%), down year-on-year (2.6%).

-

The probability of an FOMC rate increase as early as September has fallen to around 66%.

-

One rate hike before the end of the year is now the baseline scenario.

-

The EUR/USD pair strengthened by 0.6%.

-

This is not the end of the volatility – Kevin Warsh’s first testimony before the US Congress is due at 3PM.

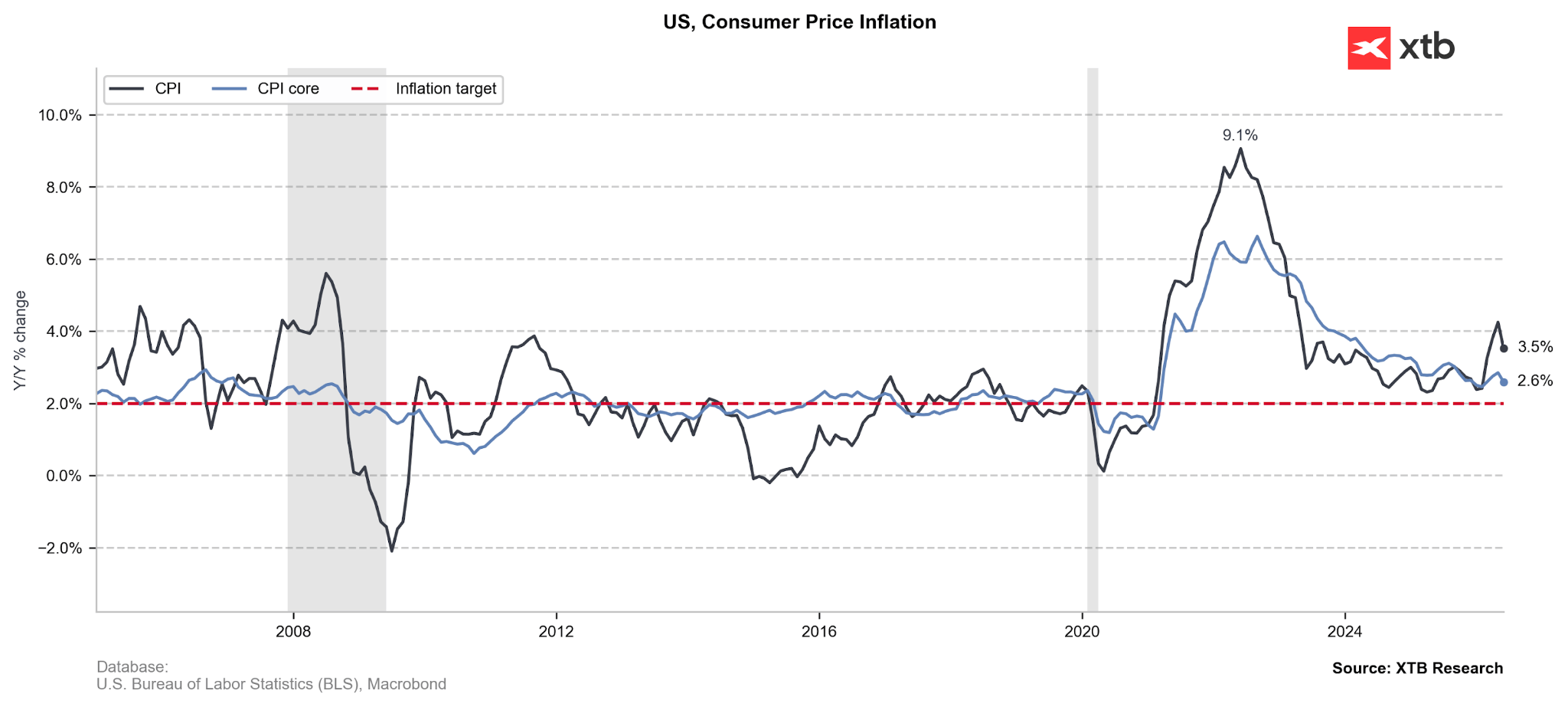

In light of lower energy commodity prices, many anticipated a June decline in US inflation. Its magnitude has significantly surprised the markets, however. On a monthly basis, prices fell for the first time since the COVID year of 2020, dropping by as much as 0.4%. Perhaps even more importantly, core inflation (2.6%), a measure that excludes the most volatile energy and food prices, came in far lower than expected.

Figure 1: US CPI Inflation (2005 - 2026)

Source: XTB Research, 14.07.2026

Source: XTB Research, 14.07.2026

What does the data reveal?

Had the drop in inflation relied solely on lower fuel prices at petrol stations (down 9.7% compared to May) and continued modest growth in food prices (up by only 0.2% month-on-month), the reading could have been dismissed. In such a volatile geopolitical environment, both of these components can significantly distort the perception of real inflationary pressure.

The point, however, is that even after excluding the most volatile elements, prices in June did not rise (core measure: 0.0% m/m). Furthermore, in many sectors such as healthcare, apparel, and the secondary car market, price decreases were observed.

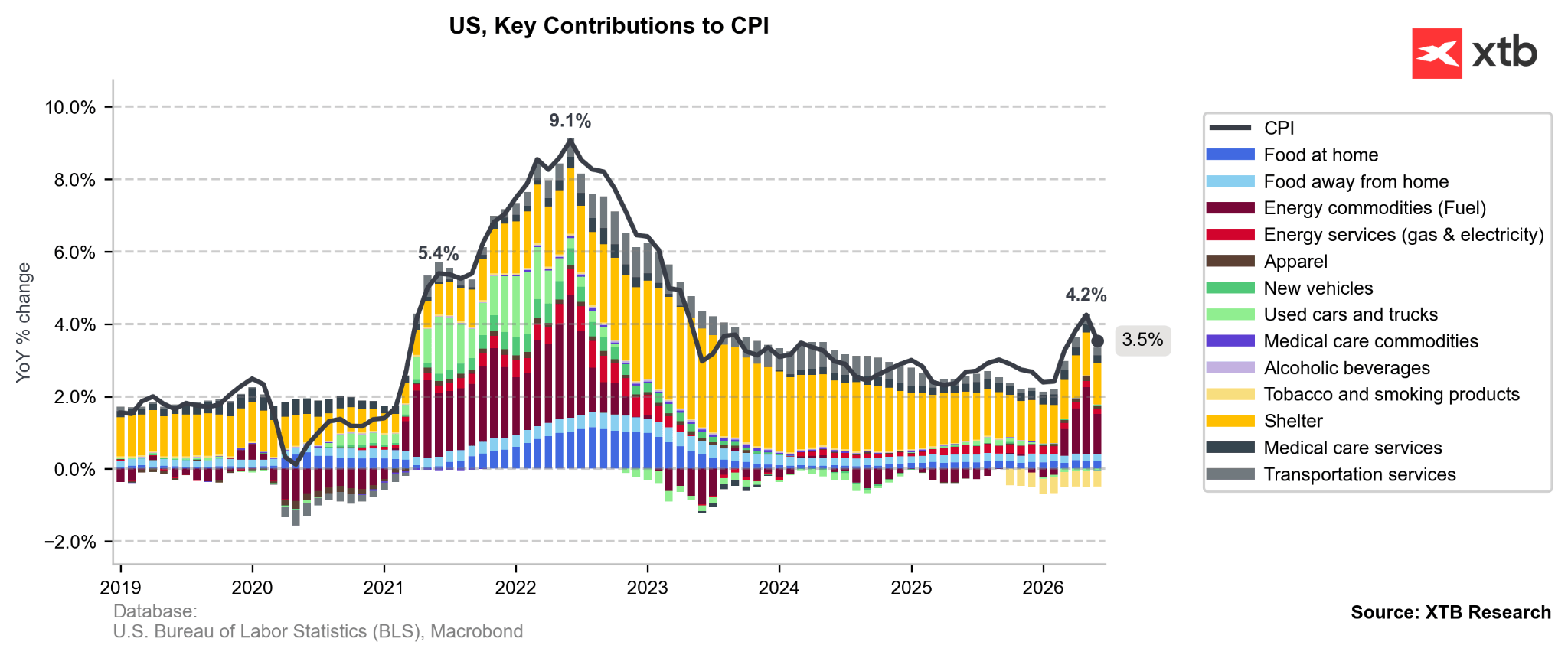

Figure 2: US CPI Inflation by Segment Contribution [y/y] (2018 - 2026)

Source: XTB Research, 14.07.2026

Source: XTB Research, 14.07.2026

Market less convinced regarding US rate hikes

Such a major surprise naturally brought about a repricing of the Fed's interest rate path as valued by the markets. Due to the recent escalation of tensions between the USA and Iran, investors at the beginning of the week began pricing in two hikes by the FOMC before the end of the year. Currently, the base scenario has returned to a single move upwards. The probability of a hike as early as September has fallen to approximately 66%.

Dollar down, Nasdaq up

This is the key factor driving the weakness of the dollar. The EURUSD pair strengthened by 0.6% and returned to the level seen at the end of last week (1.145).

Expectations of a less aggressive tightening of monetary policy by the Fed naturally also support the US stock market. The Nasdaq 100 index is gaining 0.9%.

High volatility does not end here?

Kevin Warsh's first report to the US Congress lies ahead of us. Today at 3:00 PM, the FOMC Chairman will answer questions from the House of Representatives. Tomorrow at the same time, he will appear before the Senate. Historically, the first day of hearings has carried the greatest market volatility.

We can expect Warsh to be asked about his plan to bring inflation back to target. He will most likely also have to explain the abandonment of forward guidance. However, the crucial question may be how his approach to the economy and monetary policy differs from that presented by Trump. This is particularly significant in the face of ongoing concerns regarding the loss of independence by the Federal Reserve.

—

Michał Jóźwiak, Financial Markets Analyst, XTB

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

Nasdaq Gains 0.6% and Reclaims 29,000 🔼 Strong Results from ON Semiconductor and Palantir

🗽 US500 sets a new record high

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.