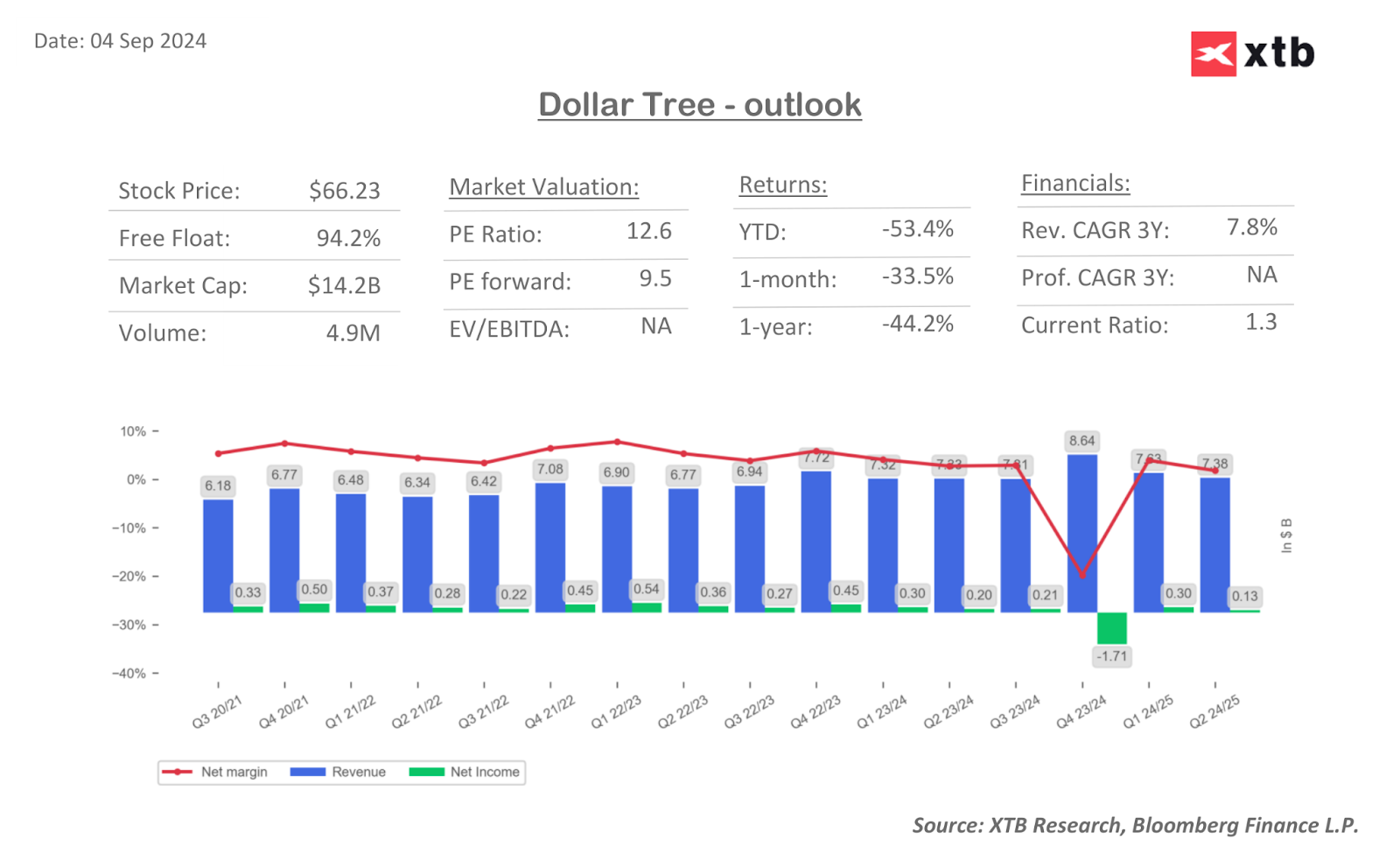

Dollar Tree disappointed the market today with both its results for the previous quarter and its forecasts for the full fiscal year. The company reached the March 2020 lows today, when the stock was pushed down by the outbreak of the COVID-19 pandemic. The company is down nearly 20% today, and has lost more than -53% since the beginning of the year.

The company reported revenues of $7.37 billion, marking the second consecutive quarter of downward sales trend. On a y/y basis, revenues managed to improve slightly (by 0.7%), however, comparing this to the previous year's growth rate (+6.9% y/y) is a disappointment, especially since the market consensus was for +1.45% revenue growth.

The Family Dollar segment performed poorly, with sales down -4% y/y. What's more, the company also recorded a 0.1% decline in comparable sales there, although in this case it was a lower decline than forecast.

Even though the company improved its gross profit margin to 30% (vs. 29.2% a year earlier), the improvement was in line with market expectations, so it did not help the company's stock price. Its increase was mainly due to lower freight costs, while being undermined by higher rental costs and increased distribution costs in the Family Dollar segment.

The biggest disappointment in the results was earnings per share, which fell to $0.67 (versus an expected increase to $1.05).

In addition to the deterioration in profitability, the company heavily slashed its outlook for the coming quarter. Dollar Tree expects Q3 revenue of $7.4-7.6 billion (average: $7.5 billion) versus forecasts of $7.6 billion. At the EPS level, the company expects $1.05-$1.15 (average: $1.1) versus forecasts of $1.32. Such forecasts are impacted by updated assumptions for costs related to the acquisition and reopening of 99 Cents Only Stores, as well as higher depreciation and deprecation throughout the 2024/25 fiscal year.

2Q24/25 RESULTS

- Adj. EPS $0.67 vs. $0.91 y/y, estimate $1.05

- EPS $0.62 vs. $0.91 y/y

- Enterprise comparable sales +0.7% vs. +6.9% y/y, estimate +1.45%

- Family Dollar comparable sales -0.1%, estimate -0.21%

- Dollar Tree Segment comparable sales +1.3% vs. +7.8% y/y, estimate +2.89%

- Net sales $7.37 billion, +0.7% y/y

- Dollar Tree net sales $4.07 billion, +5% y/y, estimate $4.16 billion

- Family Dollar net sales $3.31 billion, -4% y/y, estimate $3.35 billion

- Gross profit margin 30% vs. 29.2% y/y, estimate 29.9%

- Dollar Tree gross margin 34.2% vs. 33.4% y/y, estimate 34.1%

- Family Dollar gross margin 24.9%, estimate 24.6%

- Total location count 16,388, -0.5% y/y, estimate 16,374

- Dollar Tree Locations 8,627, +5.5% y/y, estimate 8,294

- Family Dollar locations 7,761, -6.5% y/y, estimate 8,071

Although the company's results remain disappointing and forecasts for future periods lower than expected, so the reaction of the markets seems slightly exaggerated, considering the values of the fundamental indicators for the company and comparing them to the period in March 2020, when the company was trading at similar levels. Revenues compared to that period are 17% higher, gross profit is up 13%. Concerns may be raised by the weaker operating profit, which is down 65% compared to that period, however this is probably a one-time problem for the company.

In terms of fundamental ratios, the company is trading at more favorable values on each of its key price-based ratios than it did during the Covid discount (P/E: 12.5x vs. 16.3x; P/BV 1.92x vs. 2.82x; P/S 0.5x vs. 0.76x; P/CF 5.19x vs. 8.28).

In just two weeks, the company lost more than 31% of its market capitalization. Source: xStation

Daily Summary: Markets limit the pullback while awaiting the Fed

France Challenges Palantir, Market Reacts.

US OPEN: Deeper sell-off and a SaaS rebound

Mercedes earninigs: Is optimism justified?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.