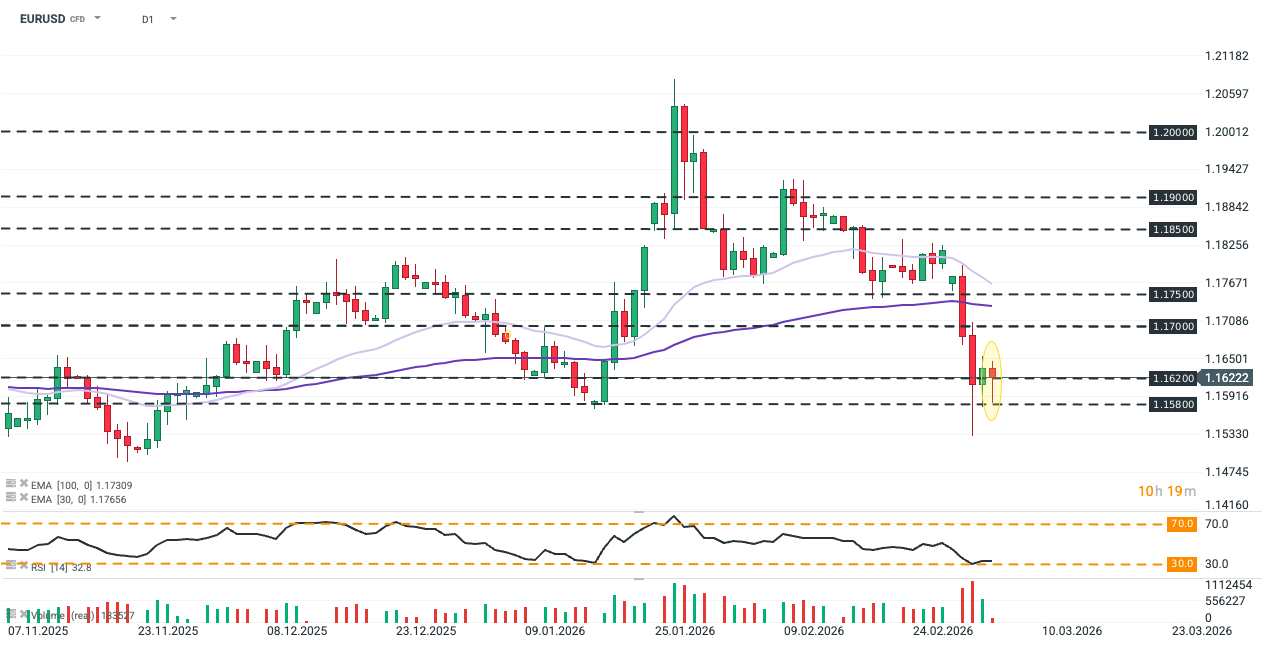

The ECB minutes failed to have any significant effect on the EURUSD rate, as the release reiterated the balanced ECB stance on tamed inflation and resilient growth momentum, which are becoming obsolete due to the newly emerged war in the Middle East.

Source: xStation5

The minutes emphasize the euro’s previous persistent appreciation, driven by its emerging safe-haven status and structural confidence. However, this strength poses a growing challenge for a trade-sensitive Eurozone. While the peak disinflationary impact from the 2025 rally is still pending, the balance of risks has fundamentally shifted following the Iran conflict.

The euro is increasingly behaving as a risk currency vulnerable to energy shocks. With rates projected to stay on hold through 2027, the ECB must now balance historical FX resilience against the new reality of energy-driven inflation.

You can find the breakdown of most important matters below:

Outlook for Inflation

-

Upward Revisions: Inflation fixings (HICP excluding tobacco) have been revised upward since December 2025, primarily due to higher oil and industrial metal prices.

-

Projections: Inflation is expected to hover around 1.8% for the second half of 2026 (approximately 1.9% when including tobacco).

-

Drivers: Higher energy and industrial metal costs added up to 30 basis points to inflation compensation, while the appreciation of the euro had only a modest dampening effect on the outlook.

-

Target: The Governing Council remains committed to returning inflation to its 2% target in the medium term.

Economic Growth and Activity

-

Global Resilience: Global growth momentum remains resilient, surprising on the upside in late 2025 and expected to stay stable at slightly over 3% through 2026 and 2027.

-

Euro Area Confidence: confidence in the Eurozone has been bolstered by a major German fiscal package (announced in March 2025) which is expected to support potential output growth through increased public investment.

-

Trade Deceleration: Despite overall growth, world trade is expected to decline substantially in 2026 due to the adverse impact of tariffs and high policy uncertainty.

Euro:

-

Drivers of Strength: The euro appreciated 1% against the USD since the previous meeting, though this was attributed to USD weakness (driven by US-specific risk shocks) rather than internal euro strength.

-

Safe Haven Status: The euro is increasingly perceived as a "safe haven" currency, particularly during periods of geopolitical crisis or US tariff threats.

-

Lagged Impact: The "peak disinflation effect" from the significant euro appreciation seen in mid-2025 has not yet been reached and is expected to play out over the next three years.

-

Competitiveness: It was noted that despite nominal stability, the persistent strength of the euro since early 2025 has made European exporters less competitive.

Risks and Uncertainties

-

Tariffs and Trade: High policy uncertainty and the threat of global tariffs remain the primary risks to global trade growth in 2026.

-

Exchange Rate Sensitivity: The Eurozone is particularly sensitive to exchange rate fluctuations given its status as a major global trading region.

-

Geopolitical Tensions: Rising geopolitical tensions have led to a sharp rally in EU defense stocks, though tariff-sensitive sectors continue to underperform.

Monetary Policy Path

-

Interest Rates: The ECB is expected to keep interest rates unchanged throughout 2026 and likely 2027; market pricing suggests a full 25 basis point hike may not occur until early 2028.

-

Approach: The Governing Council maintains a data-dependent, meeting-by-meeting approach, retaining the option to adjust the future rate path if the environment changes.

Platinum gains 6% as precious metals rebound, US Dollar weakens

🚨 Brent crude falls below $80!

Nasdaq Gains 0.6% and Reclaims 29,000 🔼 Strong Results from ON Semiconductor and Palantir

Cocoa Pauses Its Sharp Rally 🚩 Production Concerns in West Africa Return

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.