The EURUSD rate dived below 1.1600 again in response to the return of oil gains and the cooling of temporary risk appetite on Wall Street. However, the weakness of the common currency was limited by alleged comments from Iran regarding the Strait of Hormuz and new pricing of interest rate hikes in the Eurozone.

The EURUSD rate returned above 1.1610 despite clear downward pressure during the Asian session. RSI is scraping the oversold boundary, and volume remains subdued, suggesting reluctance and caution before entering large transactions amid geopolitical pressure, expectations for the ECB minutes, and tomorrow's NFP report. Source: xStation5

What is shaping the EURUSD rate today:

-

Yesterday's dollar correction was mainly technical in nature and resulted from apparent relief brought by a New York Times report, suggesting that Iran conveyed readiness for negotiations to the CIA. The rumors were denied by Iranian representatives, and the narrative of full readiness for a prolonged conflict on both sides has once again blunted risk appetite.

-

In the current situation, the euro moves like a high-risk instrument, losing as much at the start of the session as the "risk currencies" of the Antipodes (AUDUSD: -0.4%; NZDUSD: -0.3%). The reason is primarily Europe's geographical proximity to the Middle East and its significant exposure to risks related to energy prices and humanitarian crises (mass migrations). In the options market, "Put" options still dominate, indicating a dominance of fears about further declines in the euro.

-

The extent of the resumed declines in the euro was limited by a Bloomberg report based on military-linked sources, according to which Iran has not closed the Strait of Hormuz and intends to respect maritime laws. Approximately 20% of global oil supplies flowed through the strait, mainly to China, which reportedly pressured Iran regarding supply disruptions. Brent oil contracts turned back from nearly 85 to about 82.6 USD, although Kpler data points to a strong decline in traffic in the strait.

-

Retail sales in the Eurozone increased in January above expectations in year-on-year terms (2% vs. forecast 1.7%). The previous reading was revised upward from 1.3% to 1.8%, while sales compared to the previous month fell unexpectedly by 0.1% (forecast: +0.3% MoM). The data is thus of a fairly mixed nature, though it should not generate excessive pessimism.

-

The declines in monthly terms were mainly due to fuel and non-food spending, while the revision for last month significantly increased the base (from -0.5% to +0.2%). Furthermore, record frosts in January simply limited consumer mobility and their inclination for shopping trips.

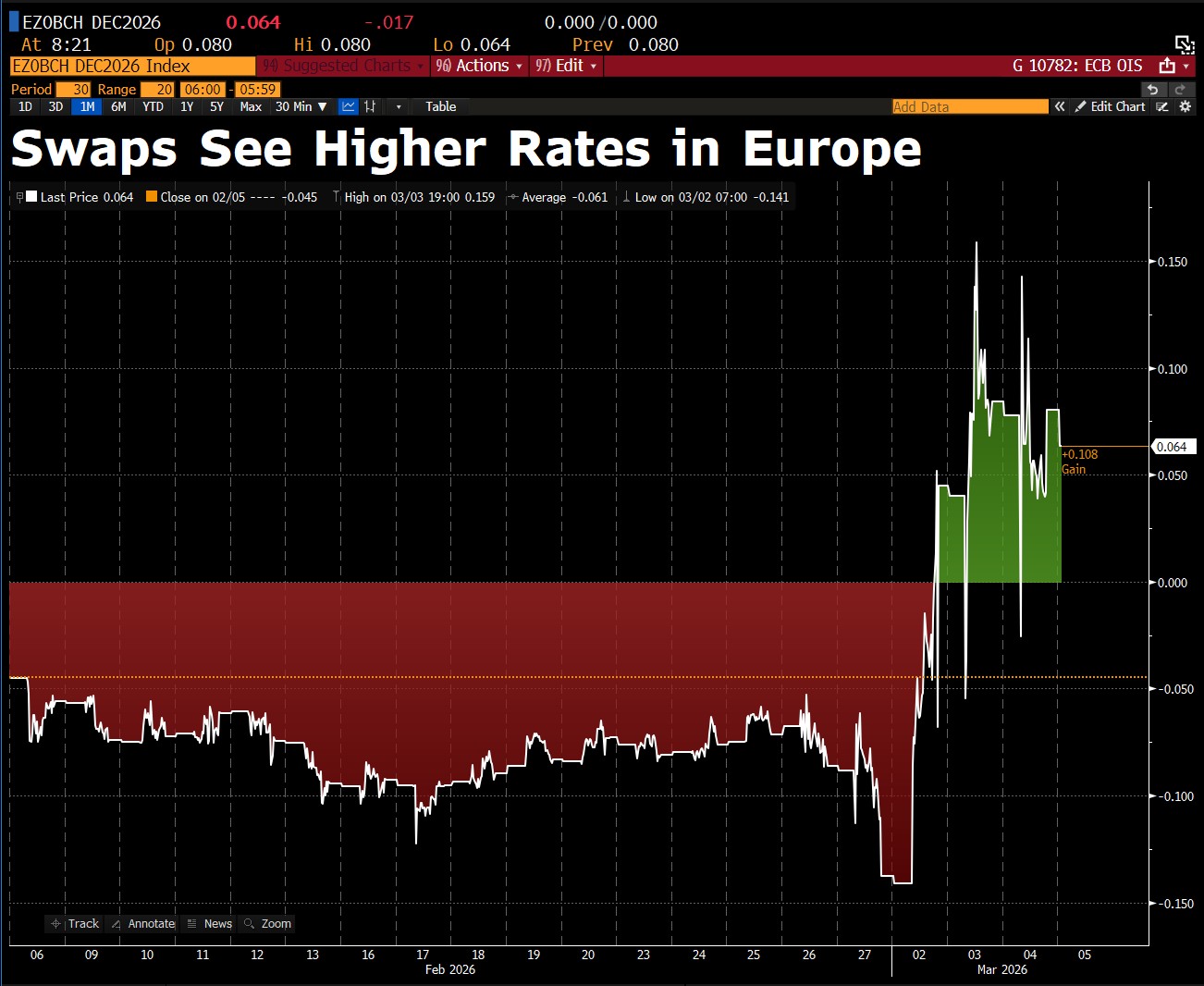

The swap market has begun to price in the probability of an interest rate hike in the Eurozone in 2026. The retail sales reading did not, therefore, divert attention from concerns about rising energy prices and the return of inflation on the Old Continent. Source: David Ingles for Bloomberg.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.