Today's market attention is primarily focused on Germany, where key labor market and inflation figures could shape expectations ahead of the European Central Bank's next policy meeting. Markets are currently pricing in a 25-basis-point ECB rate hike with nearly 85% probability, making today's inflation releases particularly important for policymakers and investors alike. Earlier in the session, traders will assess German labor market data, with the unemployment rate expected to remain unchanged at 6.4% and the number of unemployed projected to increase by 10,000, compared with 20,000 previously. However, the main event will come in the afternoon with Germany's preliminary inflation figures, where CPI is expected to ease slightly to 2.8% YoY from 2.9%, while HICP is forecast to remain unchanged at 2.9% YoY. Any upside surprise in inflation could reinforce expectations of further ECB tightening despite signs of slowing economic activity across the euro area. A more hawkish ECB outlook could, at least in theory, create some pressure on Germany's DAX index futures.

Economic Calendar

Europe

- 7 AM GMT – Switzerland: KOF Leading Indicator (Forecast: 98.0, Previous: 97.9)

- 7 AM GMT – Spain: Preliminary CPI YoY (Previous: 3.2%)

- 7 AM GMT – Spain: Preliminary CPI MoM (Forecast: 0.2%, Previous: 0.4%)

Germany

- 7:55 AM GMT – Germany: Unemployment Rate (Forecast: 6.4%, Previous: 6.4%)

- 7:55 AM GMT – Germany: Change in Unemployment, SA (Forecast: +10K, Previous: +20K)

- 7:55 AM GMT – Germany: Total Unemployed, SA (Previous: 3.006M)

Italy

- 8 AM GMT – Italy: Unemployment Rate (Forecast: 5.3%, Previous: 5.2%)

German Regional Inflation Releases

- 8 AM GMT – Saxony: CPI YoY (Previous: 2.9%)

- 8 AM GMT – Saxony: CPI MoM (Previous: 0.6%)

- 8 AM GMT – North Rhine-Westphalia: CPI YoY (Previous: 2.7%)

- 8 AM GMT – North Rhine-Westphalia: CPI MoM (Previous: 0.4%)

- 8 AM GMT – Bavaria: CPI YoY (Previous: 2.9%)

- 8 AM GMT – Bavaria: CPI MoM (Previous: 0.5%)

Italy Inflation Data

- 9 AM GMT – Italy: Preliminary HICP YoY (Forecast: 3.3%, Previous: 2.8%)

- 9 AM GMT – Italy: Preliminary HICP MoM (Forecast: 0.3%, Previous: 1.6%)

- 9 AM GMT – Italy: Preliminary CPI YoY (Forecast: 3.1%, Previous: 2.7%)

- 9 AM GMT – Italy: Preliminary CPI MoM (Forecast: 0.1%, Previous: 1.1%)

Italy GDP

- 10 AM GMT – Italy: Final GDP QoQ (Forecast: 0.2%, Previous: 0.2%)

- 10 AM GMT – Italy: Final GDP YoY (Forecast: 0.7%, Previous: 0.7%)

Germany Inflation Data

- 12 PM GMT – Germany: Preliminary CPI YoY (Forecast: 2.8%, Previous: 2.9%)

- 12 PM GMT – Germany: Preliminary HICP YoY (Forecast: 2.9%, Previous: 2.9%)

- 12 PM GMT – Germany: Preliminary HICP MoM (Forecast: 0.0%, Previous: 0.5%)

- 12 PM GMT – Germany: Preliminary CPI MoM (Forecast: 0.1%, Previous: 0.6%)

North America

- 12:30 PM GMT – Canada: Annualized GDP QoQ (Forecast: 1.5%, Previous: -0.6%)

- 12:30 PM GMT – Canada: GDP MoM (Forecast: 0.0%, Previous: 0.2%)

- 12:30 PM GMT – Canada: GDP QoQ (Previous: -0.2%)

- 12:30 PM GMT – United States: Advance Wholesale Inventories MoM (Forecast: 0.8%, Previous: 1.3%)

- 12:30 PM GMT – United States: Advance Retail Inventories ex Autos (Previous: 0.4%)

- 12:30 PM GMT – United States: Advance Goods Trade Balance (Forecast: -$87.0B, Previous: -$87.45B)

- 12:30 PM GMT – United States: Chicago PMI (Forecast: 50.3, Previous: 49.2)

Central Bank Speakers

- 8:20 AM GMT – United Kingdom: BoE Governor Andrew Bailey

- 8:30 AM GMT – Eurozone: ECB Executive Board Member Fabio Panetta

- 10:50 AM GMT – United States: Fed Governor Adriana Kugler

- 11:15 PM GMT – Eurozone: ECB Governing Council Member Olli Rehn

- 1:10 PM GMT – United States: Fed Governor Michael Barr Bowman

- 1:15 PM GMT – United States: Philadelphia Fed President Patrick Harker

- 1:35 PM GMT – Eurozone: ECB Governing Council Member Madis Müller

- 4:40 PM GMT – United States: New York Fed President John Williams

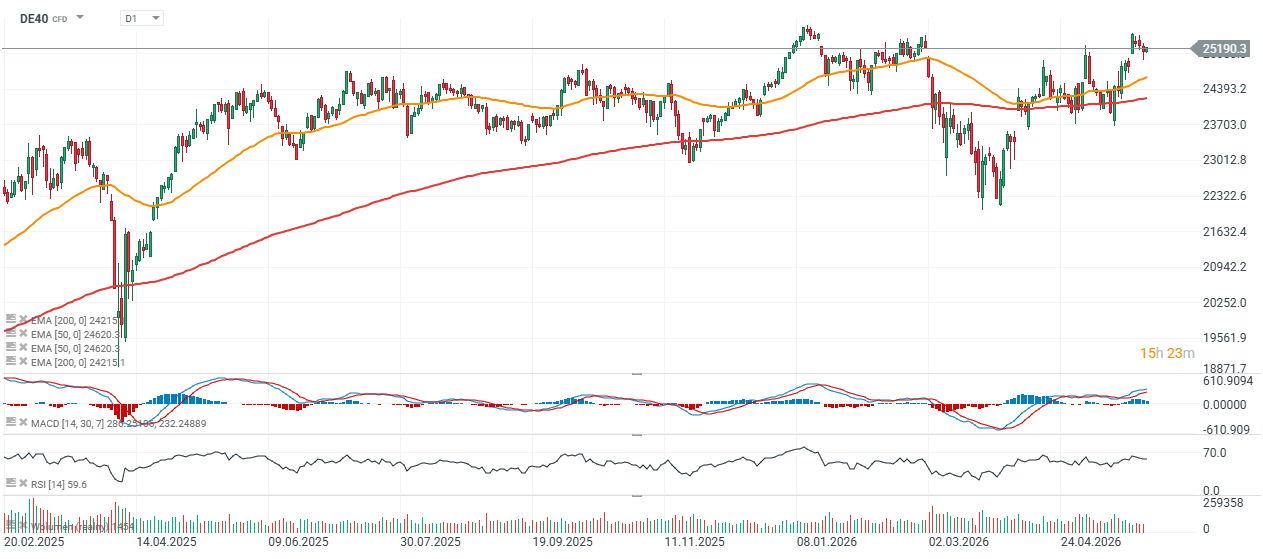

DE40 Technical Analysis (D1)

The German DE40 index remains in a strong uptrend, having recovered almost all losses from the March-April correction and once again testing record highs. The index is currently trading near 25,200 points, just below a key resistance zone defined by recent peaks.

Trend and Moving Averages

- Price remains above both the 50-day EMA (24,620) and the 200-day EMA (24,215).

- The 50-day EMA remains comfortably above the 200-day EMA, maintaining a classic bullish structure.

- Recent weeks have produced a series of higher highs and higher lows, confirming continued buyer dominance.

From a technical perspective, the long-term trend remains firmly bullish.

Key Resistance Zone

The most important resistance area currently lies between:

25,200 – 25,350 points

This zone corresponds to both this year's highs and all-time highs, which have already been tested multiple times during May.

A decisive breakout above this area could trigger another leg higher, as there is virtually no historical resistance overhead.

MACD

The MACD remains above the zero line, while the histogram has started to expand higher again.

This suggests:

- Improving bullish momentum

- Continued buyer control

- Potential for a move toward fresh record highs

At present, the indicator does not signal an imminent larger correction.

RSI

The RSI is currently trading near 60.

This level:

- Remains well below overbought territory

- Continues to support a bullish outlook

- Leaves room for additional upside without requiring a deeper pullback

Key Technical Levels

Resistance

- 25,250 – 25,350 (all-time highs)

- 25,500 (psychological target after a breakout)

- 26,000 (extended bullish target)

Support

- 24,900 – 25,000

- 24,600 (50-day EMA)

- 24,200 (200-day EMA)

- 23,700 (April lows)

Scenarios

If the index remains above 25,000 and breaks through resistance around 25,300, the market could enter a new price-discovery phase. Under this scenario, the next upside targets would be located in the 25,500–26,000 region. Failure to break above record highs could trigger profit-taking. The first downside target would be the 24,900–25,000 support zone, while a deeper correction could push the index back toward the 50-day EMA near 24,600. A sustained move below this level would represent the first meaningful sign of weakening bullish momentum. DE40 remains one of the strongest major equity indices from a technical perspective. Price action continues to hold above key moving averages, MACD supports the bullish trend, and RSI remains comfortably below overbought territory. As long as the index stays above 24,600, the base-case scenario remains further upside and another attempt to establish new all-time highs.

Source: xStation5

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.