Today is a day without trading in the US markets. Americans are enjoying a long weekend due to the 250th anniversary of independence (July 4). For this reason, the NFP data was exceptionally not released on the first Friday of the month, but a day earlier.

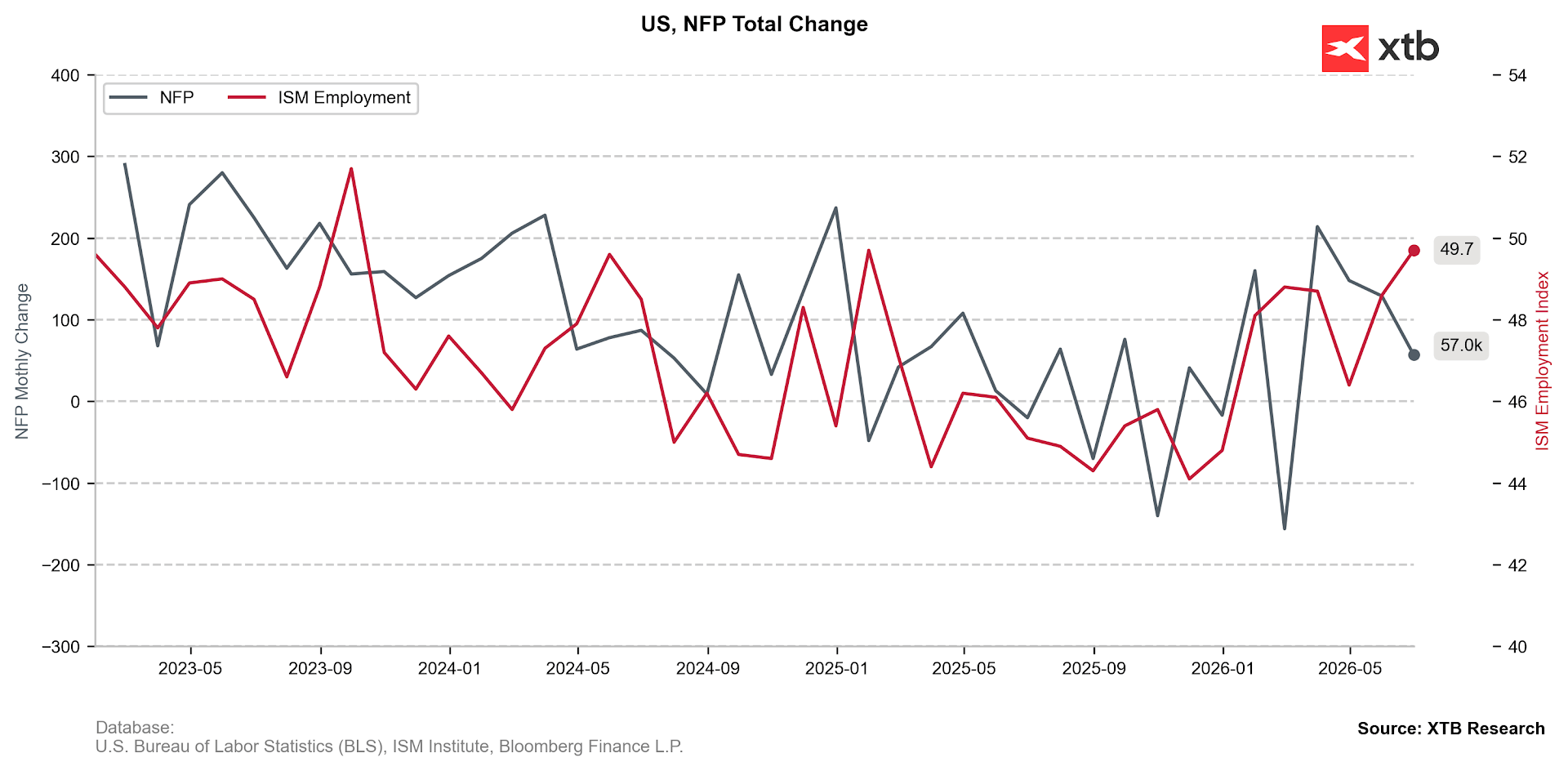

Let us recall that it proved to be an unpleasant surprise for investors, showing significantly lower than expected non-farm payroll growth (+49k vs. +107k) with a significant downward revision of data for the last two months (-74k).

Figure 1: Change in Non-farm Payrolls (NFP) and ISM PMI Employment Subcomponent (2023 - 2026)

Source: XTB Research, 03.07.2026

Source: XTB Research, 03.07.2026

Today, attention is primarily focused on PMI readings. We have behind us the publication of data from Asia, and ahead of us are revisions of readings for European countries.

🌏 Key publications from the Asian session

China

According to June PMI data, the growth pace in the services sector slowed slightly but remained very solid (54.1). A key role was played by an increase in foreign orders.

- The number of orders grew for the eighth time in a row, which contributed to renewed employment growth, and that at the fastest pace since July 2024.

- Higher personnel, raw material, and transport costs contributed to price increases, which is consistent with the latest PPI inflation data (3.9%, the highest level in nearly 4 years).

Japan

In the Land of the Rising Sun, we could only speak about a revision of data, which is of secondary importance. However, the indicator for the services sector rose from 51.8 to 52.2.

- It is worth noting in this context that the number of new orders in both the manufacturing and services sectors grew at the second fastest pace in three years, mainly due to stronger domestic demand, not exports.

Statements by the Minister of Finance, Satsuki Katayama, attracted more attention; she stated that Tokyo remains ready to intervene in the currency market. She also emphasized close cooperation with Washington in this area. She also referred to rising bond yields, noting that fiscal policy will be conducted in such a way as to regain market confidence.

Australia

We also recorded a modest upward revision in June PMI data in the Antipodes.

- The indicator for the services sector rose finally to 50.5.

- The number of new orders fell, both domestic and foreign.

- Production price inflation is the lowest since January.

- Confidence regarding prospects for the next 12 months fell to the lowest level since November 2023, influenced by concerns about the economic environment and tax changes in the federal budget.

Macroeconomic Calendar

Friday

- Spain: PMI for the services sector

- Time: 08:15 AM

- Consensus: 51

- Previous reading: 50.1

- Italy: PMI for the services sector

- Time: 08:45 AM

- Consensus: 50.3

- Previous reading: 49.4

- Germany: PMI for the services sector (revision)

- Time: 08:55 AM

- Consensus: 46.8

- Previous reading: 48.1

- Eurozone: PMI for the services sector (revision)

- Time: 09:00 AM

- Consensus: 48.9

- Previous reading: 47.7

- UK: PMI for the services sector (revision)

- Time: 09:30 AM

- Consensus: 48.7

- Previous reading: 49.3

- UK: Speech by BoE Governor Andrew Bailey

- Time: 04:00 PM

Earnings Releases

- None, US market closed due to the celebration of the 250th anniversary of independence.

3 Markets to Watch

- Japanese Yen (JPY): The USDJPY pair fell below the psychological barrier of 162. Minister of Finance, Satsuki Katayama, emphasizes, however, that Tokyo remains ready to intervene in the currency market.

- Gold and Silver: Prices of precious metals are rebounding from local lows, which can be primarily linked to lower treasury bond yields in the largest economies. This movement is supported by yesterday's data from the American labour market.

- EU50: In the face of a lack of trading in the American market, investors' attention will turn to Europe. The main question is whether capital rotation towards more defensive sectors will continue.

—

Michał Jóźwiak, Financial Markets Analyst, XTB

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Tensions around Iran weigh on markets!

US Open: Alphabet and Tesla Weigh on Wall Street, While Oil Prices Renew Investor Concerns

Market wrap: AI CAPEX loses its shine?🚩 Alphabet and Tesla weigh on global markets (23.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.