While the current week has once more been dominated by Brexit headlines, markets on the whole appear to be consolidating after the wild swings seen in previous weeks. In this analysis we will look at the current state of play and focus on what to look out for going forward that could drive GBP pairs.

Summary:

-

GBP the best performing FX major of late

-

EU grant Brexit extension to January 31st 2020

-

Two possible paths forward; Boris’s deal passes or GE

The pound has enjoyed strong gains in the past month with the largest appreciation seen in the GBPJPY and GBPCHF pairs. Source: Bloomberg

News that the EU have granted another extension to the Article 50 deadline shouldn’t come as too much of a surprise as the recent defeat in UK Parliament for the government meant that an orderly exit by the previous deadline of October 31st was all but ruled out. The new deadline is now 31st January 2020 and given the 3-month extension there are two broad routes that may be pursued going forward.

-

Press ahead with WAB

Recent events in the House of Commons have brought us to the current situation with the rejection of the program motion bill essentially ending any hopes of PM Johnson delivering on his “do or die” pledge to deliver Brexit by the end of the month. However, before that there was a landmark moment with a Withdrawal Agreement Bill (WAB) receiving parliamentary backing for the first time. On the face of it this means that there appears to be enough support for Boris’s deal to pass into law with the only issue being the October 31st deadline. Therefore, there’s a feeling that the bill’s progress will be resumed from its current state of limbo and could well by passed into law in just a few weeks time, now that an extension has been granted. Investment banks including JP Morgan and Goldman Sachs have since stated that this is their base case scenario, and it would likely give the pound another boost if it transpires.

-

Government calls GE

While the first path clearly looks plausible, if Brexit has taught anything it is that politics is rarely as straightforward as it seems. While the WAB received a larger than expected majority of 30 there is a feeling that this wasn’t a “clean” vote and some of those who supported it did so, safe in the knowledge that they would subsequently vote against the program motion and effectively halt the government’s plans to pass the bill. Furthermore, the bill had yet to reach the stage where possible amendments such as a customs union or 2nd referendum could be attached and therefore it is far from given that its current guise wouldn’t be changed significantly and to a point where the government would no longer support it - they can withdraw the bill if they disagree with any amendments.

The most obvious way around this hurdle would be if the government moved to call a general election (GE) in a bid to seek to change the composition of MPs and secure a more favourable level of parliamentary arithmetic. The risk here is clear, with it being far from guaranteed that the government would gain seats and additional MPs who support their deal - something PM Johnson’s predecessor Theresa May can attest to. In terms of what a GE would mean for the pound it would depend entirely on the result. A greater level of support for the current WAB would then ensure its passage but there is also a chance that it could bring more extreme outcomes such as no-deal and a 2nd referendum back to the table. In the short-term the increased uncertainty associated with this would likely weigh on the pound until the results become more clear.

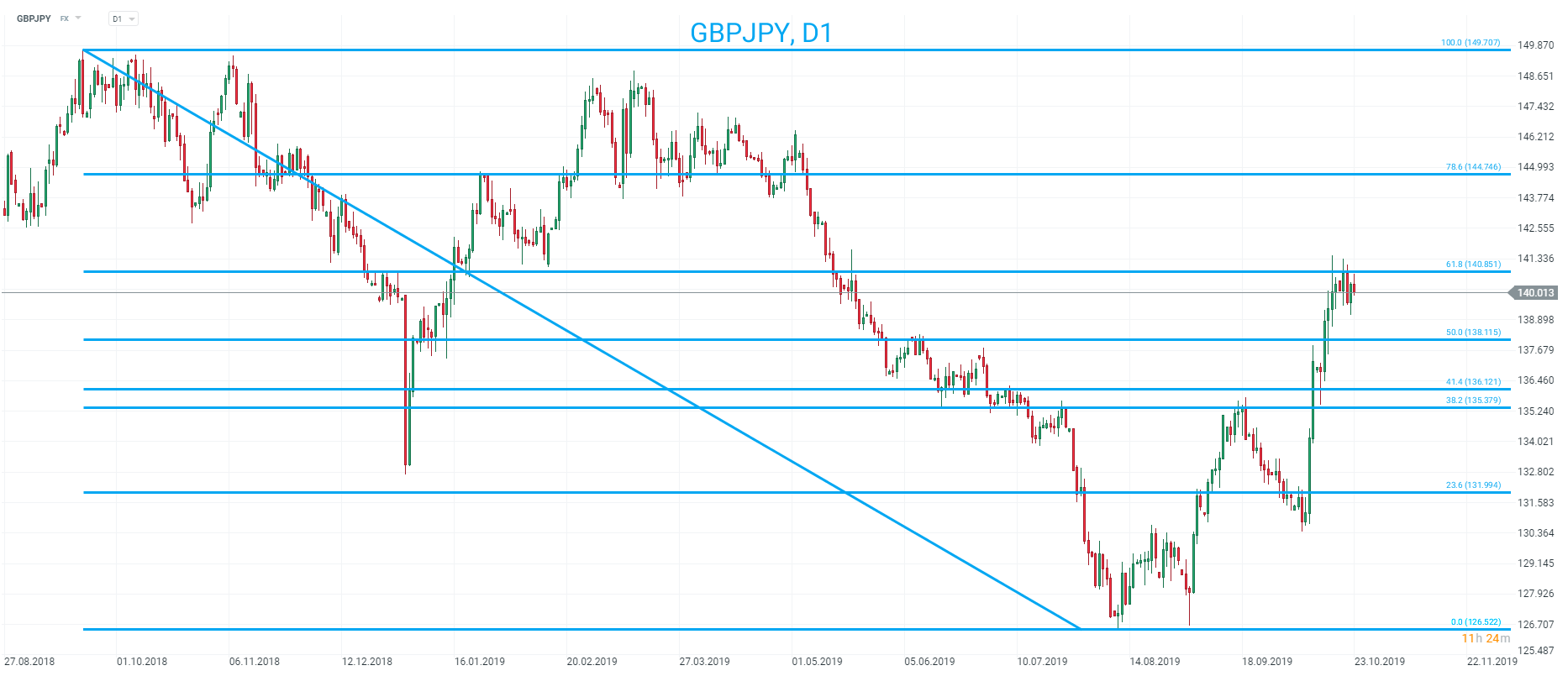

GBPJPY has soared of late on hopes that the latest Brexit deal would pass with gains of around 900 pips in the past couple weeks. Price is now probing the 61.8% fib retracement of the larger decline which began just over a year ago in late September 2018. Source: xStation

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

Not so hawkish words, dovish dodges. EURUSD at 1.1450 during Kevin Warsh's Q&A

BREAKING: Fed Keeps Rates Unchanged Amid Regional Dissents and Warsh's Pause

🟡Gold tests $4000 ahead of the Fed decision

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.