Today's European session has been characterized by stabilization. Major indices are posting modest gains, but without any signs of euphoria. Investors are attempting to recover from the earlier deterioration in sentiment on Wall Street and from rising geopolitical tensions surrounding the Middle East and the Strait of Hormuz.

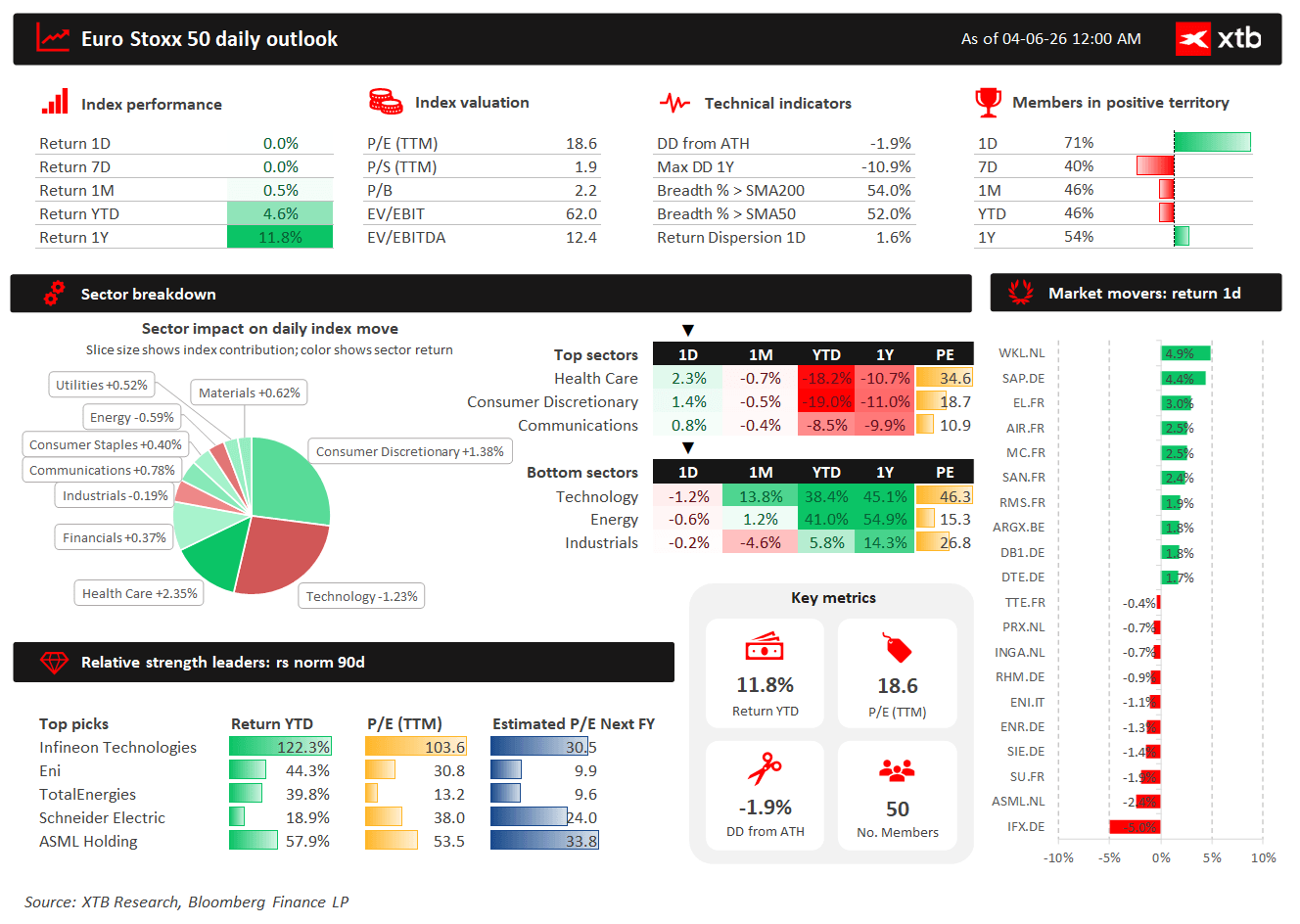

The key takeaway from the Euro Stoxx 50 is that the index itself remains essentially flat, but market breadth looks encouraging — as many as 71% of constituents are trading higher. The main challenge, however, has been weakness among several large technology stocks, particularly Infineon and ASML, which weighed on the broader index.

Major European Indices

- STOXX 600 gains around 0.2%, indicating a moderate improvement in risk appetite across Europe.

- DAX is up 0.9%. The German market continues to be weighed down by weak construction-sector data.

- FRA40 gains 1.3%, supported by stronger performance from luxury, consumer, and retail-related stocks.

- UK100 has recovered its initial losses and is now trading slightly higher, supported by banks and real estate-related companies.

EU50: Index Near Flat, but Most Stocks Are Rising

- Euro Stoxx 50 is up 0.5% on the day, with the majority of components remaining in positive territory.

- 71% of constituents are advancing, suggesting that buying activity has been fairly broad-based.

- However, the broader market picture remains weaker over longer timeframes, with the proportion of stocks in positive territory standing at approximately 40% over 7 days, 46% over 1 month, and 46% year-to-date.

- The index remains only about 1.9% below its all-time high.

- Valuations remain moderately elevated, with TTM P/E: 18.6; P/S: 1.9; P/B: 2.2; EV/EBITDA: 12.4

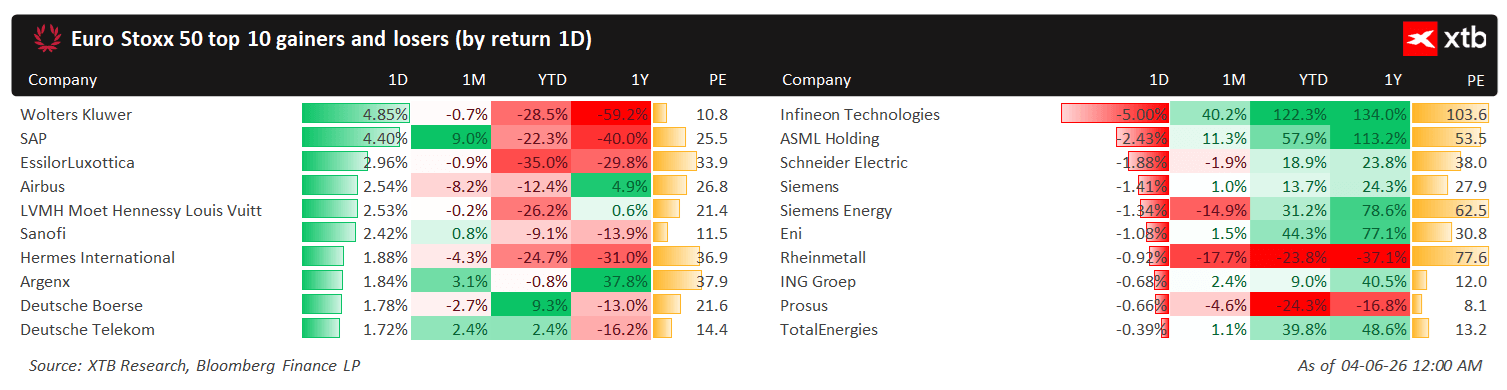

- Health Care (+2.3%) was the strongest sector in the Euro Stoxx 50 and made the largest positive contribution to the index's daily performance. Within healthcare, notable gainers included Sanofi +2.42%, EssilorLuxottica +2.96%, argenx +1.84%, Bayer +1.35%

- Technology (-1.2%) was the largest drag on the index despite a strong performance from SAP. Weakness in technology was concentrated in semiconductors: Infineon -5.0%, ASML -2.4%.

Top Performers in the Euro Stoxx 50

- Wolters Kluwer +4.85% — the strongest stock in the index, benefiting from demand for defensive quality and stable business models.

- SAP +4.40% — a very strong session for German software, partially offsetting weakness elsewhere in European technology.

- EssilorLuxottica +2.96% — strong performance from the consumer-healthcare segment, supporting the French market.

- Airbus +2.54% — a positive contribution from industrials, despite mixed performance across the broader sector.

- LVMH +2.53% — a rebound in luxury goods that also supported the CAC 40.

- Sanofi +2.42% — a strong day for healthcare, the best-performing sector within the Euro Stoxx 50.

- Hermès +1.88% — another luxury name attracting strong demand.

- Deutsche Börse +1.78% and Deutsche Telekom +1.72% also contributed positively to market breadth.

Geopolitics and Oil

- The main factor supporting sentiment was news of a conditional ceasefire between Israel and Lebanon.

- Markets interpreted this as a partial reduction in regional escalation risks, particularly after earlier concerns regarding shipping security through the Strait of Hormuz.

- Brent crude prices fell toward the $92–95 per barrel range, although they remain elevated compared with levels seen before the escalation.

Macro: weak retail sales

- Eurozone retail sales declined by 0.4% month-over-month in April, slightly weaker than the consensus expectation of a 0.3% decline.

- However, March data were revised sharply higher, which helped soften the negative implications of the April reading.

- On an annual basis, retail sales increased 1.0% year-over-year, significantly above market expectations of 0.3%, providing a more encouraging signal for consumer demand across the euro area.

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Hormuz Deal Moves Closer

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.