- European defence stocks are declining as investors reassess political risk and the uncertainty surrounding government procurement programmes.

- Germany's cancellation of the F126 frigate programme demonstrates that larger defence budgets do not guarantee the execution of every major contract.

- The long-term trend of rising defence spending across Europe remains intact, but investors are paying closer attention to order book quality and the credibility of companies' growth outlooks.

- European defence stocks are declining as investors reassess political risk and the uncertainty surrounding government procurement programmes.

- Germany's cancellation of the F126 frigate programme demonstrates that larger defence budgets do not guarantee the execution of every major contract.

- The long-term trend of rising defence spending across Europe remains intact, but investors are paying closer attention to order book quality and the credibility of companies' growth outlooks.

European defence companies are facing heavy selling pressure after the German government decided to cancel the F126 frigate programme. Shares of Germany's Rheinmetall, Hensoldt and Renk have fallen sharply, dragging the broader European defence sector lower as investors reassess the risks surrounding Europe's rearmament cycle and its long-term outlook. Berlin's decision demonstrates that even amid rapidly rising defence budgets, public procurement remains highly political, subject to shifting military priorities and vulnerable to changes in government strategy.

It is worth noting that defence stocks have already been under pressure for some time, with the sector's powerful upward momentum seemingly fading after several years of exceptional gains. Following the preliminary US-Iran agreement, another – and potentially much more significant – black swan event for the industry could be developments in the war in Ukraine. After more than four years of conflict and continued battlefield stalemate, both Russia and Ukraine may eventually be pushed towards negotiations by growing economic and political pressures.

The ongoing correction across the defence sector illustrates that investing in defence is far more complex than simply buying companies benefiting from higher military spending. Individual procurement programmes can be delayed, renegotiated or even cancelled if governments conclude that other defence priorities offer a better return on investment. The key question now is whether, if the conflict in Eastern Europe eventually subsides, European governments will remain sufficiently committed to honouring their long-term defence investment pledges.

The market was reminded who the customer really is

Regardless of the sector's long-term outlook and the fact that geopolitical tensions remain elevated globally, the immediate catalyst for the sell-off was Berlin's decision to abandon the programme for six F126 frigates, a contract estimated to be worth more than €12 billion. Instead of proceeding with the delayed and increasingly expensive project, Germany opted to purchase eight smaller MEKO A-200 frigates from TKMS, citing cost overruns, delays and the need to strengthen naval capabilities more quickly.

For investors, this served as an important reminder that even during periods of record defence spending, procurement decisions remain heavily influenced by politics, changing military priorities and project execution risks. This is one of the defining characteristics of the defence industry. Governments are effectively the only customers, and they can rapidly shift spending priorities between armoured vehicles, ammunition, air defence systems, drones, cybersecurity or space technologies.

A correction after an extraordinary rally

Only a few months ago, European defence companies were among the biggest winners of the continent's multi-year equity rally. Rheinmetall, Leonardo, Saab, BAE Systems, Thales and Hensoldt all benefited from an unprecedented surge in military orders following Russia's invasion of Ukraine and NATO countries' steadily rising defence budgets.

However, such an extraordinary rally also pushed investor expectations to very demanding levels. As a result, any information raising doubts about project execution, contract timing or future revenue growth has started triggering disproportionately large market reactions.

Analysts point out that Rheinmetall's market capitalisation declined by more than €10 billion following the F126 announcement, even though the economic value of the cancelled contract was considerably smaller. This suggests that the current correction is not merely about the loss of a single project but rather reflects a broader reassessment of future growth expectations.

Does this mean Europe is about to reduce defence spending? At this stage, there is little evidence supporting such a scenario. Nevertheless, investors may increasingly price in this possibility given the changing political landscape in countries such as Italy, the United Kingdom and even Germany.

Despite the recent correction, the long-term fundamentals remain robust. NATO members have agreed to gradually increase defence and security-related spending to 5% of GDP by 2035, with 3.5% allocated to conventional military expenditure and an additional 1.5% dedicated to infrastructure, logistics, cybersecurity and broader national resilience.

At the same time, Europe still faces several structural investment needs, including:

-

rebuilding ammunition stockpiles depleted through military support for Ukraine,

-

modernising outdated military equipment,

-

expanding domestic defence manufacturing capacity,

-

increasing investment in air defence, unmanned systems and space technologies.

This suggests that overall defence spending is likely to remain elevated for many years, even if the composition of that spending changes significantly over time.

What does this mean for investors? Painful charts for Rheinmetall and Hensoldt

From an investment perspective, revenue diversification is becoming increasingly important. Companies with exposure across multiple defence segments—from armoured vehicles and ammunition to radar systems, military electronics, drones and advanced defence technologies—are generally less vulnerable to individual procurement decisions.

Despite the current sell-off, most analysts continue to believe that Europe's rearmament cycle will extend well into the next decade. Recent developments should be viewed primarily as a reminder of the political nature of defence procurement rather than as evidence that Europe's defence spending boom has come to an end.

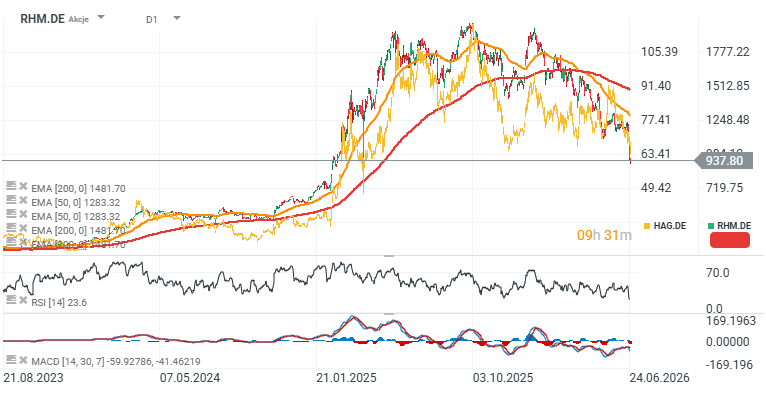

Looking at the share price performance of Germany's two major defence contractors, Rheinmetall and Hensoldt, both companies have now fallen by more than 50% from their respective highs. The sharp reversal has pushed their share prices back to levels last seen in spring 2025, highlighting just how dramatically investor sentiment toward the sector has shifted.

Source: xStation5

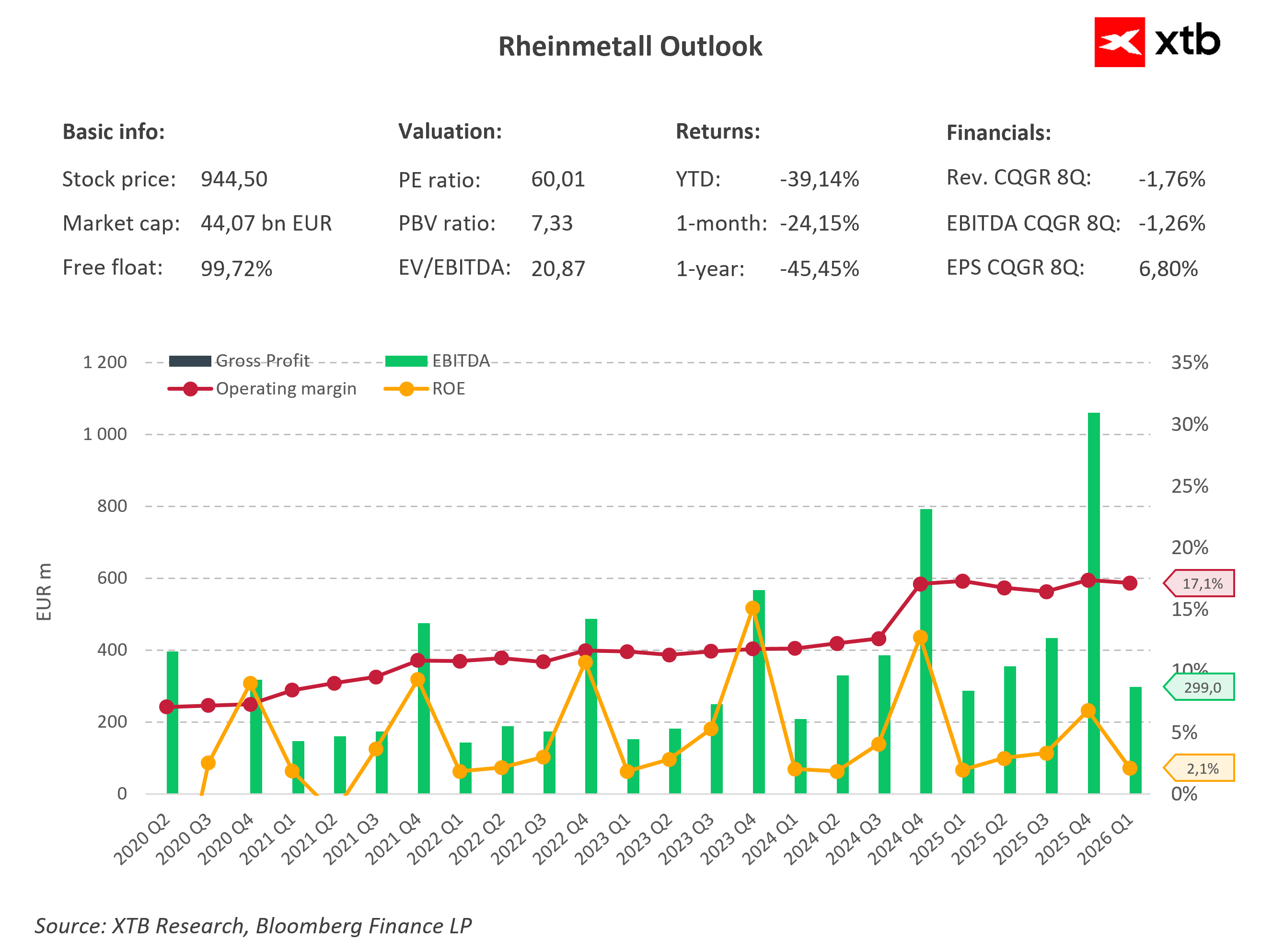

Rheinmetall continues to deliver strong operating profitability, with its operating margin reaching approximately 17.1% despite the ongoing correction in the share price. Quarterly EBITDA remains volatile but has posted several record readings in recent quarters, reflecting the growing scale of contract execution. At the same time, the stock has declined by more than 39% year-to-date and over 45% over the past year, while its valuation remains demanding with a P/E ratio of around 60. Overall, the chart highlights the growing disconnect between the company's solid operating fundamentals and deteriorating investor sentiment.

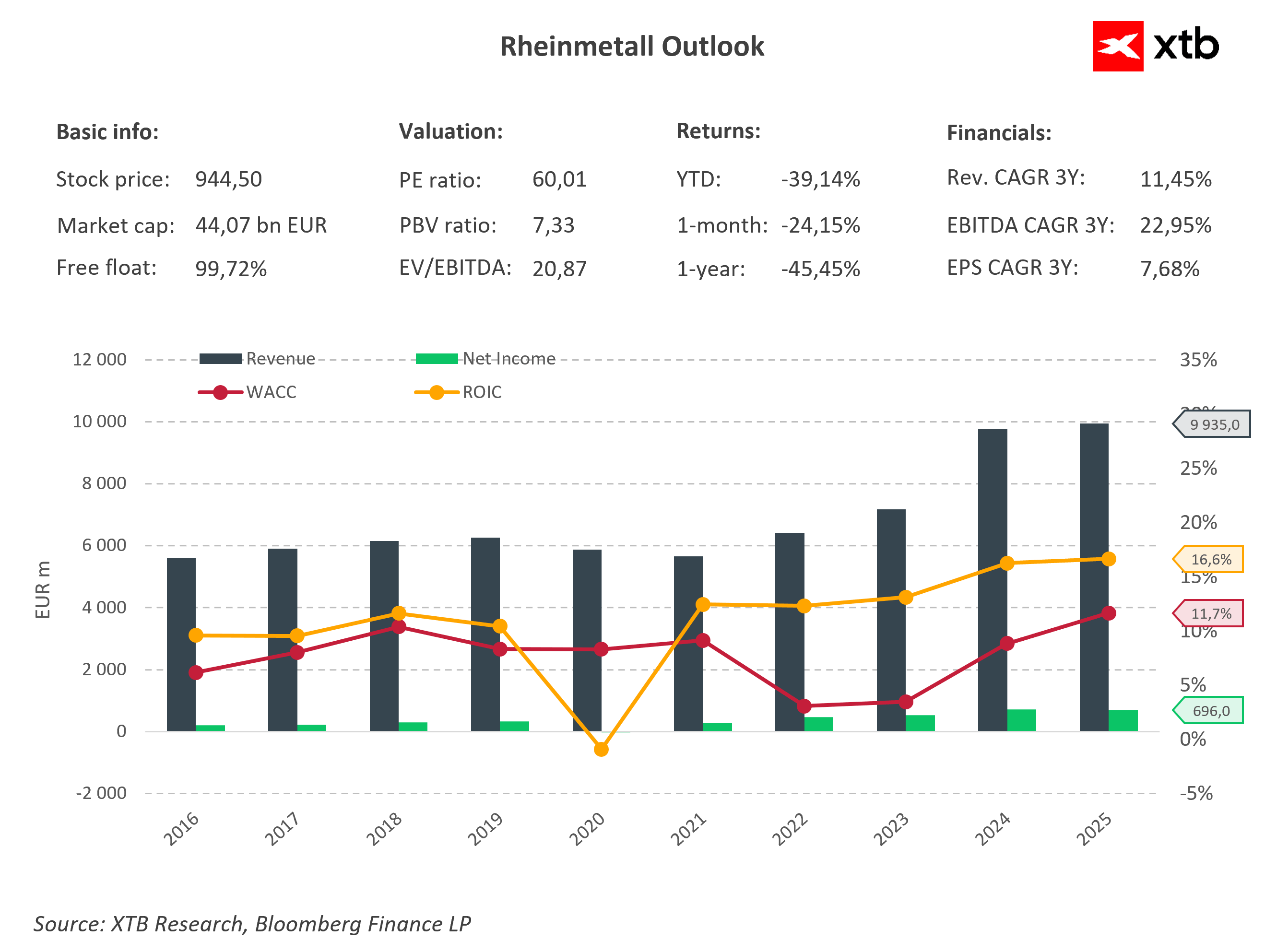

Source: XTB Research

Rheinmetall's revenue has nearly doubled since 2020, reaching almost EUR 10 billion in 2025, while net income increased to approximately EUR 696 million. At the same time, ROIC has improved to around 16.6%, remaining comfortably above the company's 11.7% WACC, indicating that Rheinmetall continues to create shareholder value. Despite these robust financial fundamentals, the stock remains in a deep correction following its previous record rally. This suggests that investors are currently focusing more on the risk of slower future order growth than on the company's strong historical financial performance.

Source: XTB Research

Eryk Szmyd Financial Markets Analyst, XTB

AMD Did Everything Right… But Only Right

SpaceX Shares Drop 6% After Earnings 🚩 Is Space No Longer Enough for Wall Street?

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.