-

European Stagflation: Germany has drastically cut its 2026 GDP forecast from 1.0% to just 0.5% while inflation expectations remain elevated. Combined with the ongoing energy crisis and the threat of jet fuel shortages, the Eurozone is facing a high risk of stagflation.

-

The Euro’s Safe Haven Limitation: ECB Chief Economist Philip Lane has acknowledged that the Euro cannot currently rival the US Dollar as a global safe haven. The lack of a unified "safe asset" (comparable to US Treasuries) and political fragmentation remain significant structural barriers.

-

Cautious ECB Policy: Despite inflationary pressures, the ECB is expected to hold rates steady in April. However, markets are pricing in nearly two hikes by the end of the year, contingent on TTF gas price spikes and the duration of the Middle East conflict.

-

USD Dominance (EURUSD): The currency pair remains under downward short-term pressure due to a clear growth divergence between a resilient US economy and a stagnating Europe. Speculative positioning reflects this, as investors continue to favor the greenback amid heightened geopolitical uncertainty.

-

European Stagflation: Germany has drastically cut its 2026 GDP forecast from 1.0% to just 0.5% while inflation expectations remain elevated. Combined with the ongoing energy crisis and the threat of jet fuel shortages, the Eurozone is facing a high risk of stagflation.

-

The Euro’s Safe Haven Limitation: ECB Chief Economist Philip Lane has acknowledged that the Euro cannot currently rival the US Dollar as a global safe haven. The lack of a unified "safe asset" (comparable to US Treasuries) and political fragmentation remain significant structural barriers.

-

Cautious ECB Policy: Despite inflationary pressures, the ECB is expected to hold rates steady in April. However, markets are pricing in nearly two hikes by the end of the year, contingent on TTF gas price spikes and the duration of the Middle East conflict.

-

USD Dominance (EURUSD): The currency pair remains under downward short-term pressure due to a clear growth divergence between a resilient US economy and a stagnating Europe. Speculative positioning reflects this, as investors continue to favor the greenback amid heightened geopolitical uncertainty.

The situation in the Eurozone, particularly in its "engine," Germany, is deteriorating rapidly in the face of the ongoing conflict with Iran. It is worth noting that Germany, like other European countries, relies heavily on energy imports; therefore, a continued impasse regarding the closure of the Strait of Hormuz worsens the long-term outlook for the Euro.

-

Drastic GDP Forecast Cuts: The German Ministry of Economy has slashed its GDP growth forecast for 2026 by half – from 1.0% to just 0.5%. The outlook for 2027 has also been revised downward to 0.9%.

-

Inflationary Pressure: Despite the economic slowdown, inflation in Germany is expected to rise to 2.7% in 2026 and 2.8% in 2027. The Bundesbank warns that the "real pain" associated with the Middle East crisis is still ahead, and Europe could face a jet fuel shortage within the next six weeks.

-

Trade Risks: While Donald Trump has limited authority to impose broad tariffs, the potential for sector-specific tariffs remains, which could heavily impact the crucial German economy.

ECB Interest Rate Outlook: Caution and a Lack of Alternatives

Statements from European Central Bank policymakers indicate a difficult balancing act between fighting inflation and supporting economic growth.

-

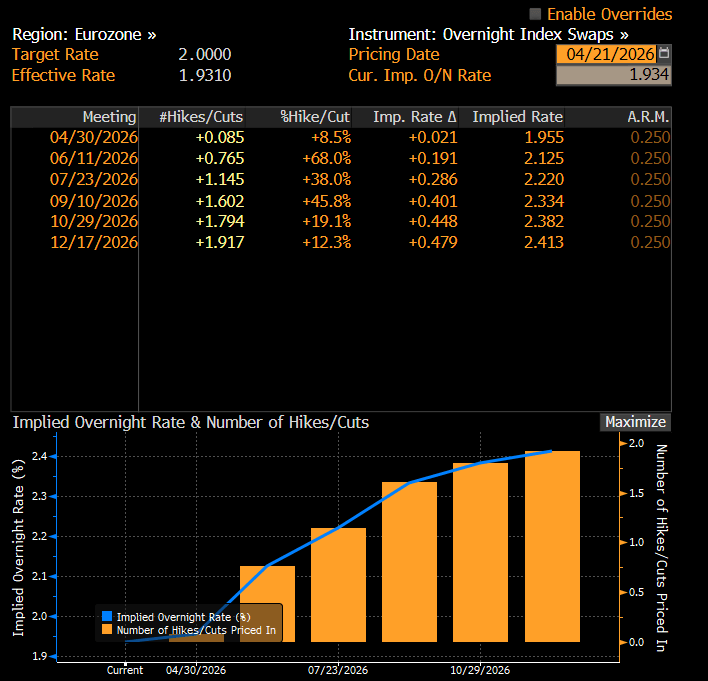

No April Hike: The ECB’s Gediminas Simkus clearly stated that the bank should not raise interest rates at the April meeting. The current deposit rate of 2.00% is considered appropriate given stable core inflation, despite spikes in headline inflation caused by energy prices.

-

Door Open for 2026: However, Simkus does not rule out a hike later this year, citing structural risks such as rising defense spending and supply chain disruptions.

-

Euro’s Weakness as a Safe Haven: ECB Chief Economist Philip Lane admitted that the Euro is currently unable to replace the Dollar as a global safe haven. Lane points to the lack of unified European "safe assets" (similar to U.S. Treasuries) and the political fragmentation of the Eurozone as primary barriers.

The market currently does not price in a significant chance of an April hike. Nevertheless, if inflation becomes a tangible problem, the prospect of a hike this year remains strong. Furthermore, the market is pricing in nearly two hikes by the end of the year. The first is possible in June or July, though the central bank will likely wait for the conflict to conclude or react to a sharp rise in TTF gas prices, which is a key factor for EURUSD. Source: Bloomberg Finance

The market currently does not price in a significant chance of an April hike. Nevertheless, if inflation becomes a tangible problem, the prospect of a hike this year remains strong. Furthermore, the market is pricing in nearly two hikes by the end of the year. The first is possible in June or July, though the central bank will likely wait for the conflict to conclude or react to a sharp rise in TTF gas prices, which is a key factor for EURUSD. Source: Bloomberg Finance

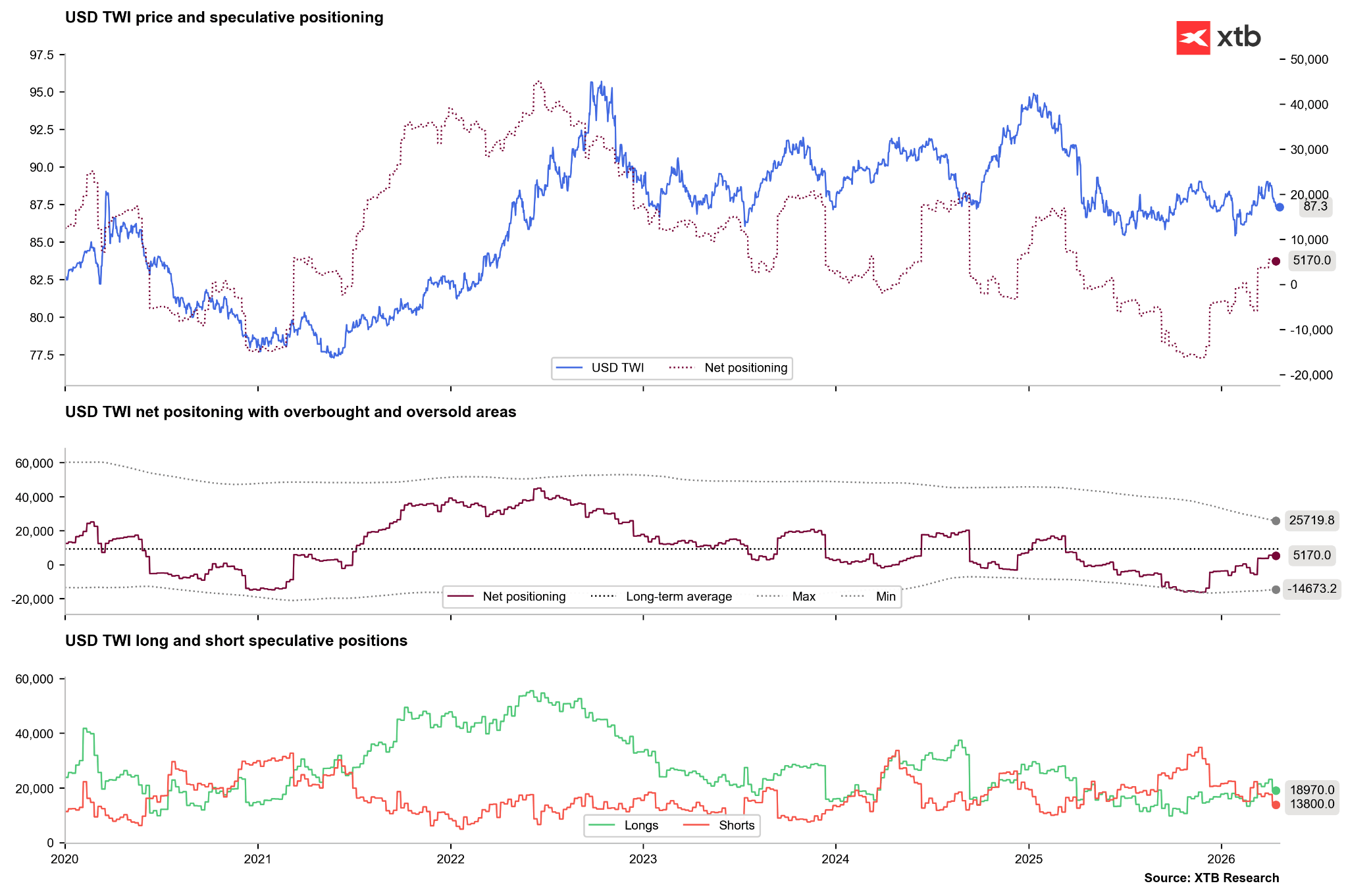

EURUSD Analysis: The Dollar Remains King

The EURUSD pair is under clear downward pressure, resulting from a combination of fundamental and geopolitical factors.

-

Growth Divergence: While the U.S. shows relative resilience, Europe (led by Germany) is sinking into stagnation. Investors prefer the Dollar due to the depth and liquidity of the U.S. bond market, as noted by Philip Lane.

-

Risk Factors: Potential U.S. tariffs and a prolonged energy crisis in Europe (with oil risks above $100 and TTF gas above €60) continue to favor the Dollar.

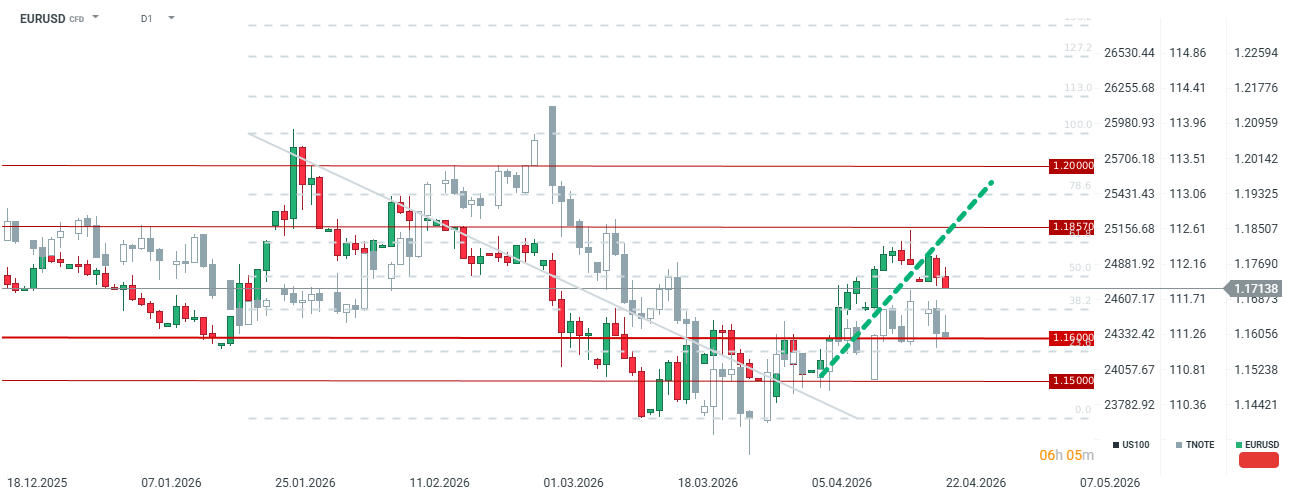

EURUSD is retreating significantly, hitting its lowest levels since April 13. The pair is breaking below its upward trendline, signaling that the market still sees substantial risk stemming from the Middle East conflict. Although EURUSD appears relatively well-valued based on yield spreads, speculative investors have recently begun to favor the U.S. currency, selling off the Euro. This situation could reverse once energy prices begin to decline and investors start rotating out of U.S. assets in search of other opportunities, especially considering the massive risks associated with U.S. debt and the upcoming midterm elections.

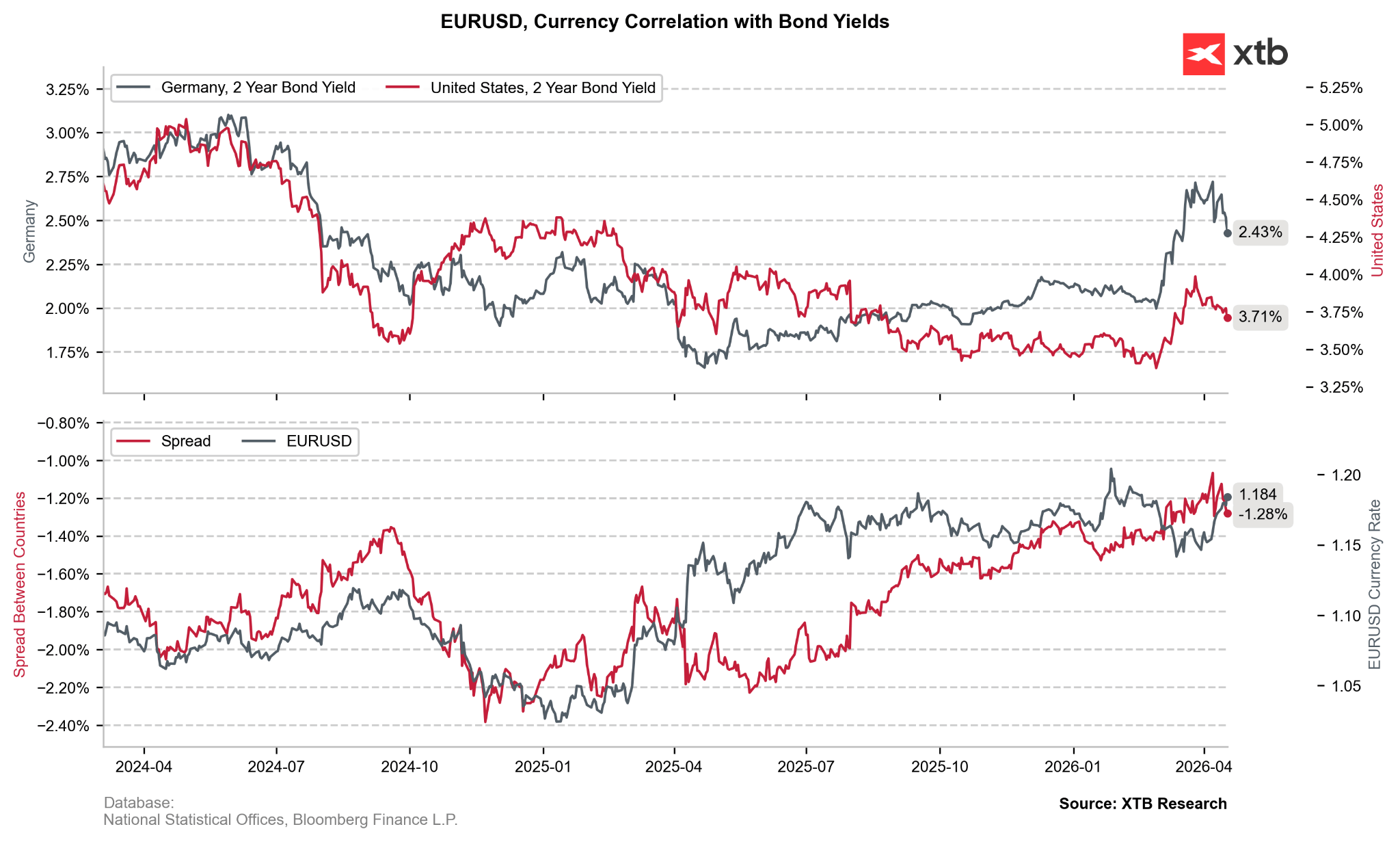

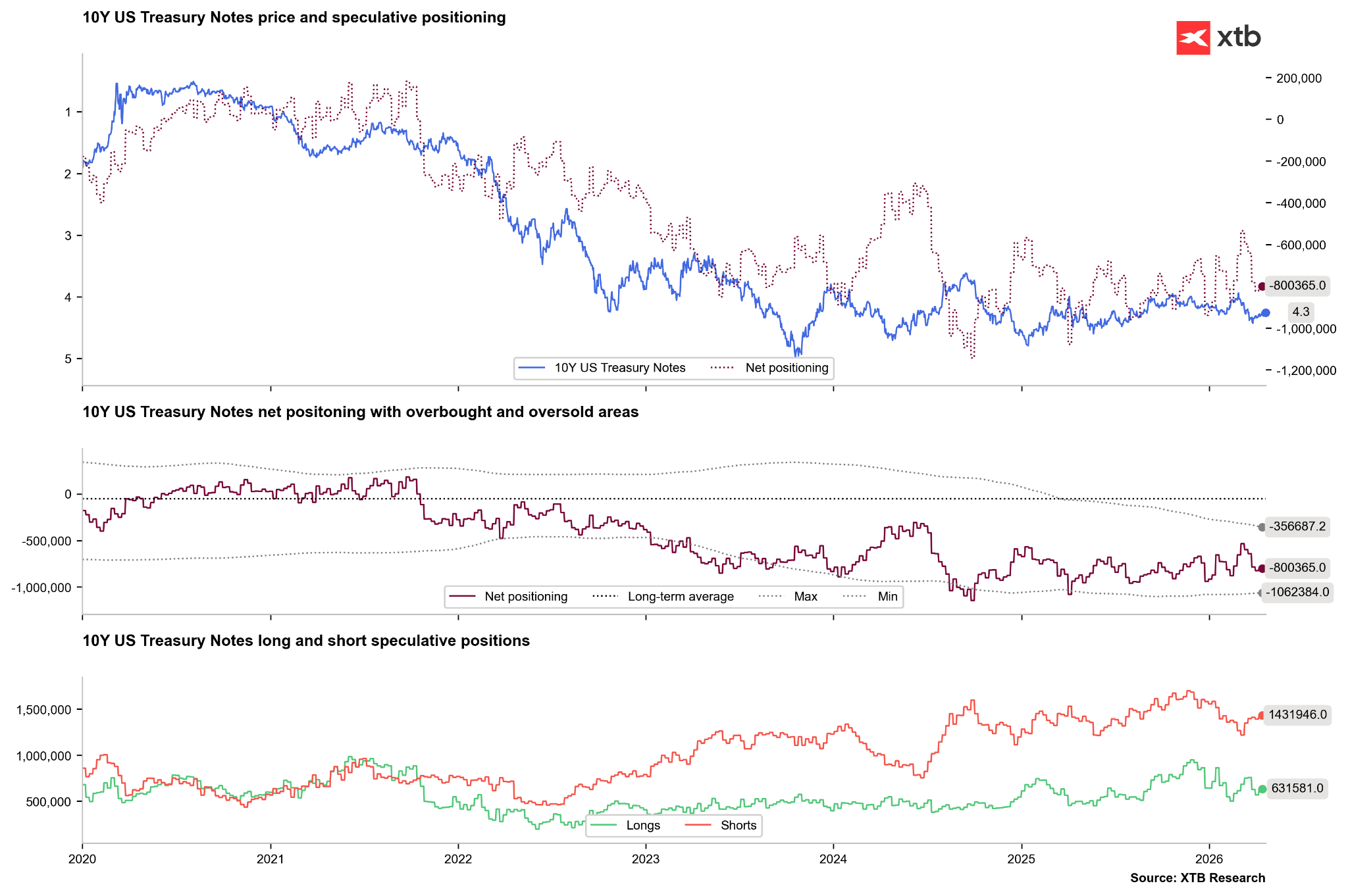

German bond yields have fallen significantly recently, even despite expectations of potential ECB rate hikes. Nevertheless, EURUSD remains fairly valued relative to yield spreads.

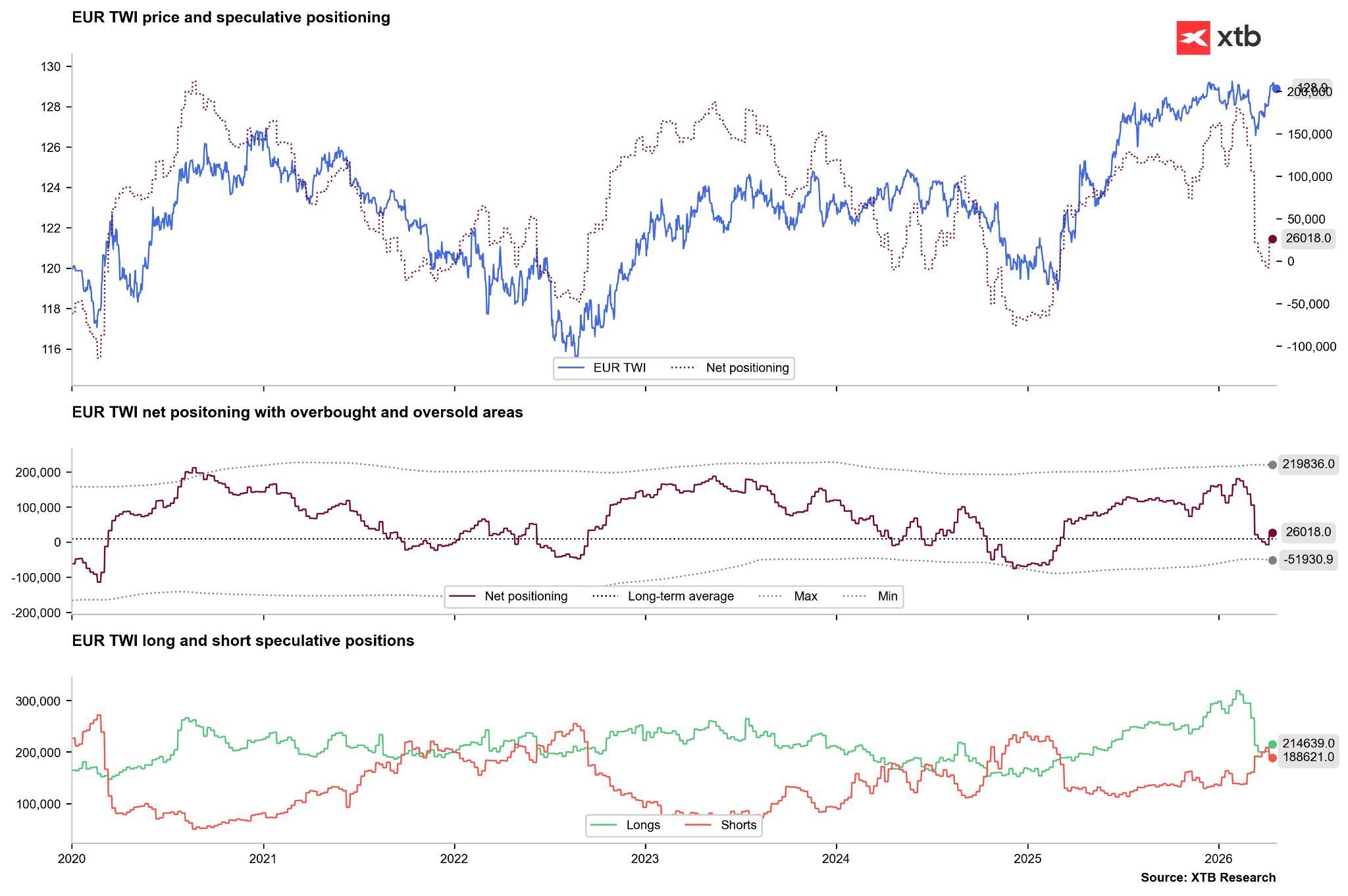

Investors aggressively offloaded long Euro positions in recent weeks, though the last 2-3 weeks saw a shift back toward positive net positioning. We could potentially see a repeat of the 2022 scenario, where after an initial sell-off, investors began closing short positions as energy price risks faded.

On the other hand, the market remains somewhat more convinced by the Dollar, though this is primarily driven by the covering of short positions, which pushed net positioning into positive territory. If long positions were to rebound in the coming weeks to levels not seen since early 2025, it could signal the development of a broader upward trend.

Simultaneously, U.S. bonds are facing renewed selling pressure, though not as severe as in late 2024 or 2025. A key factor regarding U.S. debt could be the new leadership under Kevin Warsh. During his Senate Banking Committee hearing, Warsh indicated he would not be "Trump's puppet" but expressed dissatisfaction with the Fed's current predefined policy. He also intends to move away from the Fed's preferred inflation metric, PCE. While Warsh did not signal immediate cuts, any such signals amid elevated inflation could trigger a sharp bond sell-off, which might not necessarily be positive for the Dollar.

Summary

The Euro faces clear internal challenges and a high dependency on terms of trade, which are strictly linked to commodity prices. Although the U.S. economy outperforms the Eurozone, EURUSD has not plunged as sharply as it did in 2022. If global conditions stabilize, the Euro—despite its weaknesses—could behave as it did in 2022/2023, albeit starting from significantly higher levels. Conversely, if the war drags on, the Dollar has every chance to remain "king" for many months to come.

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

Daily Summary: A sell-off with a spin-off

Iran Escalation: What to Watch and What to Expect

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.