Although the Fed cut rates at its December meeting, the decision was seen as hawkish. The Fed reduced expectations for future cuts, indicating that rates will only be cut twice in 2025. At the same time, however, it is important to note the current situation in the US ahead of Trump's inauguration. The President-elect indicated in a recent speech that interest rates are too high. In turn, Michael Barr, the Fed's vice chairman for supervision, resigned from his seat on the Board of Governors, which could theoretically open the way for a less stringent regulatory approach.

Hawkish cut in December 2024

The Fed decided to cut in December, and only Beth Hammack of the Cleveland Fed decided to vote to keep rates unchanged. On the other hand, the dot-plot for 2024 itself suggested as many as 4 votes for maintaining. In view of this, it can be expected that 3 members influenced by the discussions decided to follow the consensus. Nevertheless, the Fed members themselves see a limited number of reductions this year, which ultimately influenced the rather pronounced rise in yields in recent weeks. The Fed has also quite clearly raised inflation expectations for 2025, suggesting less willingness to cut. Still, the Fed does not know exactly how tariffs might affect inflation, as Trump's future policies remain unknown.

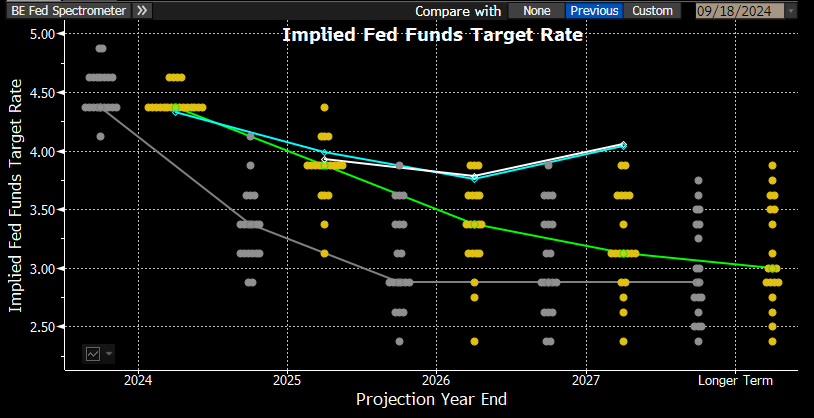

The Fed has clearly raised expectations for interest rates in 2025. In turn, the implied path by interest rate contracts suggests that cuts will end sooner than expected. The rise in long-term yields in recent weeks has been very large indeed. Source: Bloomberg FInance LP, XTB

What then can be expected from the minutes?

- Most likely, the majority of members will express concern about the rebound in inflation

- A large portion of members may indicate that inflation has become uncertain due to Trump's policy uncertainty

- Uncertainty will most likely prompt FOMC members to take a more cautious approach

Uncertainty supports the dollar

- There is fairly mixed news coming out of the US media and sources. The Washington Post reported that Trump's team would take a slightly softer tariffs course.

- However, Trump quickly 'dismissed' the validity of this information, and today's CNN reports pave the way for the opposite scenario, in which Trump is considering imposing a state of emergency to allow him to introduce a new tariff policy, quickly after January 20

- Markets don't like uncertainty, so the lack of clear signals and transparency about future White House policy is putting pressure on risky assets, especially technology stocks, and favouring the US dollar

- Yields on 10-year U.S. Treasury bonds are hovering around 4.7%, further 'weighing down' stock market sentiment and supporting the dollar, against other currencies

- The Fed's Christopher Waller signaled that the short-term as well as long-term impact of higher tariffs on inflation and the economy is uncertain. He also signaled that he does not expect drastic increases in tariffs

- Waller conveyed that inflation is invariably on track to reach the 2% target and expects further rate cuts in 2025

- The Fed may postpone decisions on rate cuts until the second half of the year, when the impact and Trump's new trade policy will be much clearer

EURUSD (H1, D1)

Demand for 'safe haven' assets, combined with weak macro data from the European economy, is weighing on sentiment for the EURUSD pair, where the difference in yields and the strength of the two economies could drive the pair to parity in 2025. Yields on 10-year bonds have recently risen to 4.7%, a level already higher than short-term interest rates. From the perspective of the last month, the term curve has changed its shape and now long-term yields are clearly higher than short-term rates. 10-year yields are already higher than current interest rates, even with the expectation of further cuts.

If the Fed minutes actually show that many members did not want to vote for cuts and the future approach will be more cautious, a further rise in yields cannot be ruled out, which could lead to a further bump on the EURUSD. At the same time, however, yields are already extremely high for the current monetary situation. More impetus will be needed for the EURUSD to fall towards parity. At the same time, in the event of an upward correction, the move should be limited by the downward trend line, which currently runs slightly above the 1.04 level.

Source: xStation5

The EURUSD pair is today again testing levels not seen since November 2022.

Source: xStation5

Breaking: US services remain strong, inflation pressures rise

GOLD eyes 4200 USD 🟡

US ADP employment below estimates! EURUSD extends gains 📈

Economic calendar: US macro data and big tech earnings🔎

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.