Over the past month, the EURUSD pair has fallen by 2.5%, reaching the 1.135 level. A number of factors have contributed to the dollar's strengthening. The most significant was last week's FOMC meeting, which led to a substantial increase in market expectations regarding interest rate hikes across the Atlantic. The sell-off in the equity market, driven by the semiconductor sector, and the release of relatively decent PMI data for June were also significant factors.

At 14:30, we await perhaps the most important macroeconomic reading of the week – US PCE inflation for May.

Why is this of such significance to the markets?

- As the situation in the Middle East has calmed somewhat, investors can once again focus fully on key macroeconomic releases.

Groundbreaking information still holds significant potential to trigger high volatility in the markets. However, the bar for such "breakthroughs" is set much higher than in the first weeks of the conflict. The market expects concrete actions and is meticulously tracking whether traffic in the Strait of Hormuz will indeed be restored to a state approaching normality.

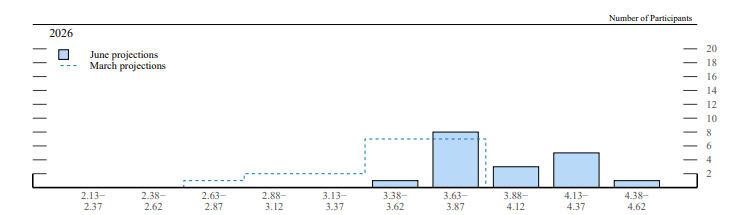

- Following the last FOMC meeting, expectations for interest rate hikes have risen sharply.

The Dot Plot accompanying the latest decision showed that as many as half of the policymakers consider an interest rate hike before the end of the year to be the most rational course of action from the perspective of current needs. Every third member of the committee projects two or more hikes.

Chart 1: Change in the FOMC Dot Plot [June vs. March] (2026)

Source: FOMC, 25.06.2026

The market currently prices in approximately 40 bps of interest rate hikes before the end of the year (less than two full moves up). This represents a very significant change compared to the pre-meeting situation, when not even one hike was fully priced in.

This may be the last month in which very high oil prices will be reflected to such a large extent in the headline inflation index. Therefore, if the core reading does not show a clear spillover of inflation into other sectors, investors will receive a serious signal to limit bets on interest rate hikes.

- The PCE measure – although delayed – is preferred by the Fed when making decisions regarding monetary policy.

The reading is published with more than a two-week delay relative to the CPI measure. Nevertheless, it is of immense value to the markets. It is on the basis of PCE data that decisions regarding the adjustment of interest rate levels are made.

Additionally, along with the PCE inflation data, reports will be released regarding:

- Q1 GDP (revision),

- durable goods orders in May,

- consumer income and spending in May,

- the number of new jobless claims.

What are the market expectations?

The consensus assumes:

- an increase in the headline measure to 4.1% year-on-year (3.8% in April);

- an increase in the headline measure to 0.4% month-on-month (0.4% in April);

- an increase in the core measure to 3.4% year-on-year (3.3% in April);

- an increase in the core measure to 0.3% month-on-month (0.2% in April).

Markets will focus primarily on the core measure, which excludes the most volatile components – food and energy – providing a more reliable picture of deeply entrenched price pressure. A decline in this could condition the FOMC's reduced inclination to tighten monetary policy. Currently, the market prices in approximately 45% probability of two interest rate hikes before the end of the year – in the event of a core measure reading significantly lower than the consensus, we can expect a dovish repricing in this regard, and consequently – a weakening of the dollar.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

US Open: AMD and SpaceX failed to impress, but the broader market remains resilient

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.