- The consensus assumes the headline inflation rate to reach its highest level since 2023.

- However, the focus is primarily on the core measure.

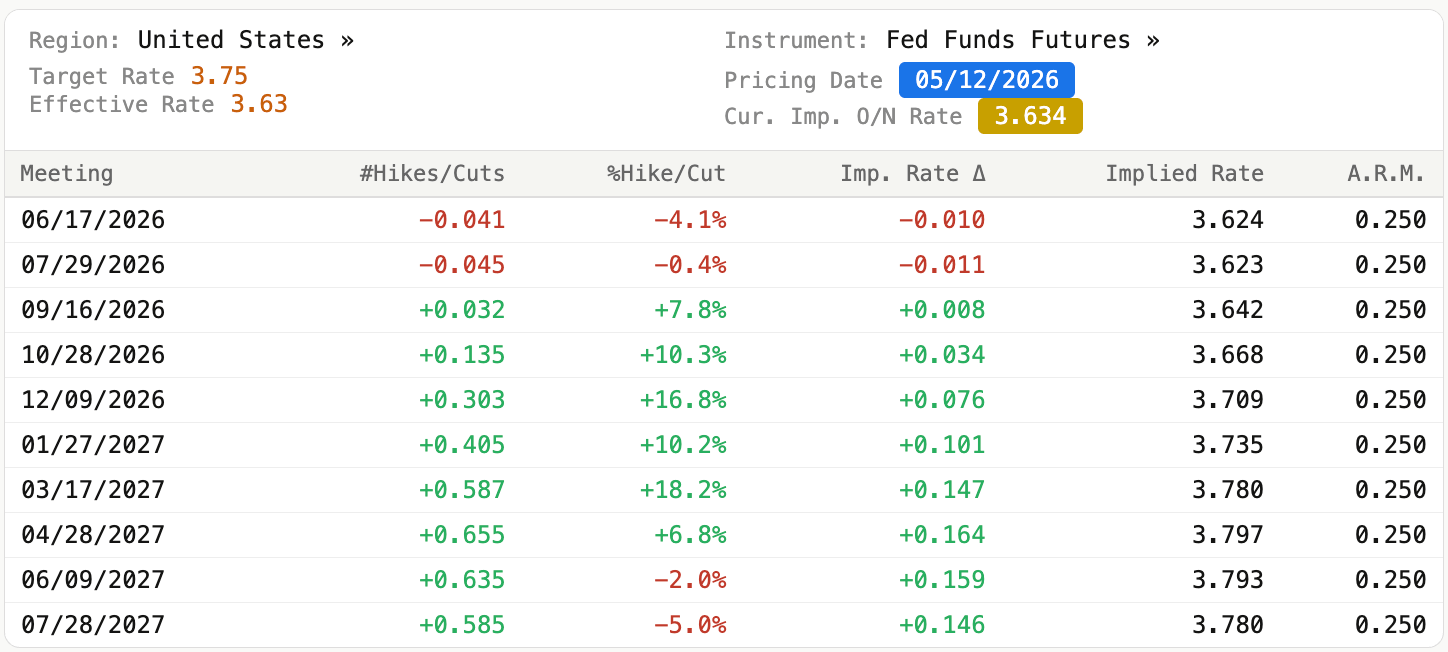

- The market assigns a probability of around 30% to a US interest rate hike before the end of the year.

- The dollar is strengthening as investors move away from risk.

- The consensus assumes the headline inflation rate to reach its highest level since 2023.

- However, the focus is primarily on the core measure.

- The market assigns a probability of around 30% to a US interest rate hike before the end of the year.

- The dollar is strengthening as investors move away from risk.

The April US CPI inflation reading is scheduled for release later today (13:30). The consensus is for a significant increase in the headline figure (to around 3.7%, the highest level since September 2023) and a modest rise in the core one (to 2.7%).

Markets will focus primarily on the latter, which excludes the most volatile components – food and energy – providing a more reliable picture of deep-rooted price pressures. An increase in this measure could make the FOMC more inclined to tighten monetary policy. At present, the market is pricing in an approximately 30% probability of an interest rate hike before the end of the year – should the core measure come in significantly above the consensus, we can expect a hawkish repricing, and consequently a stronger dollar.

Figure 1: Market-implied FOMC interest rate projection (2026 - 2027)

Source: Bloomberg, 12/05/2026

Source: Bloomberg, 12/05/2026

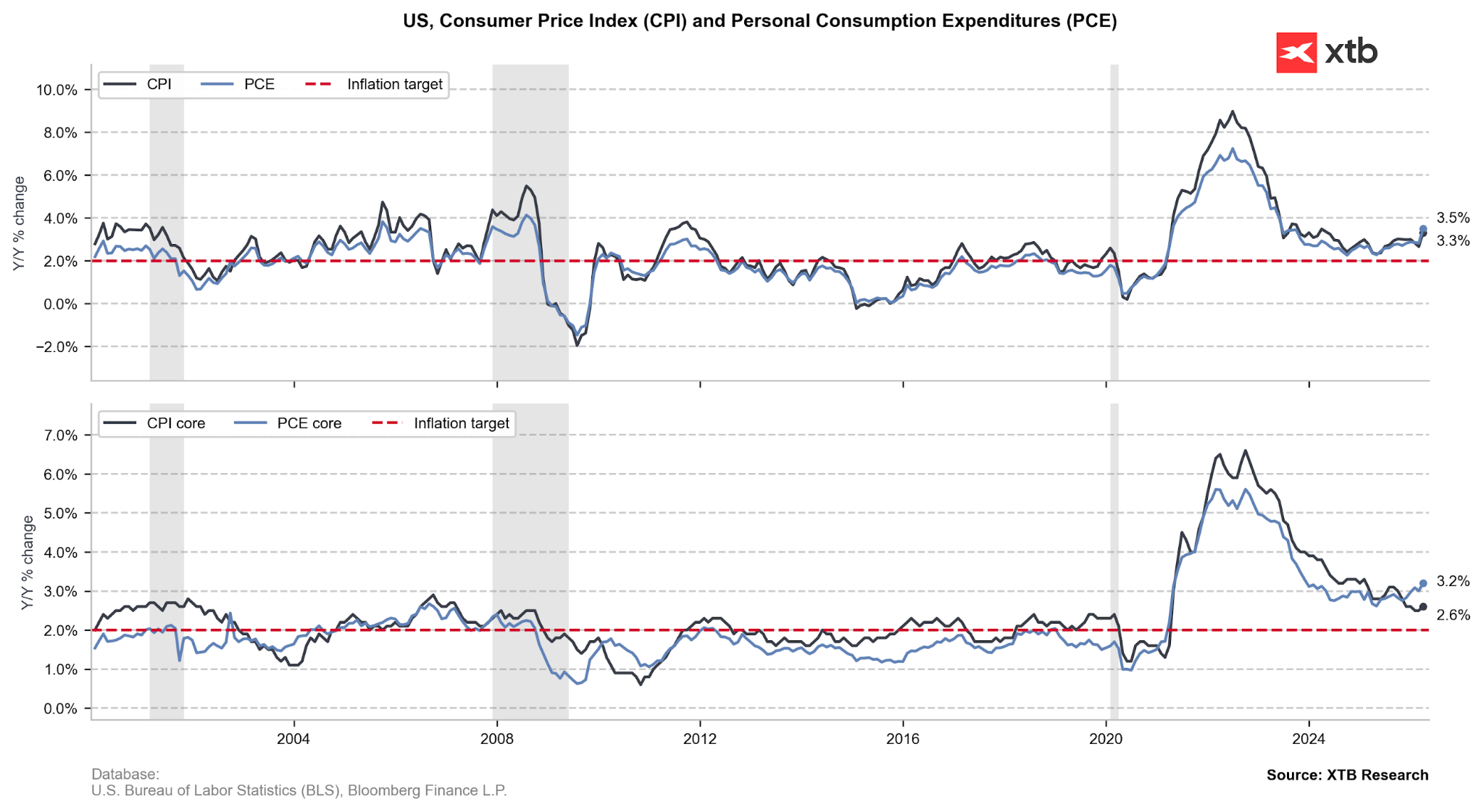

It should be borne in mind, however, that the average consumer perceives inflationary pressure not in core terms but in nominal terms, with a disproportionately large emphasis on fuel and food prices. A rise in the headline measure above the expected level (3.7%) should therefore also serve as a bullish signal for the dollar. Although this in itself should not constitute an argument for raising interest rates, as it is by nature largely regarded as temporary, it may contribute to a rise in inflation expectations, which will certainly be very important for the Committee. This could, in turn, lead to higher wage growth and consumption in the future, creating the so-called second-round effects.

Figure 2: US CPI and PCE inflation (2000 - 2026)

Source: XTB Research, 12/05/2026

Source: XTB Research, 12/05/2026

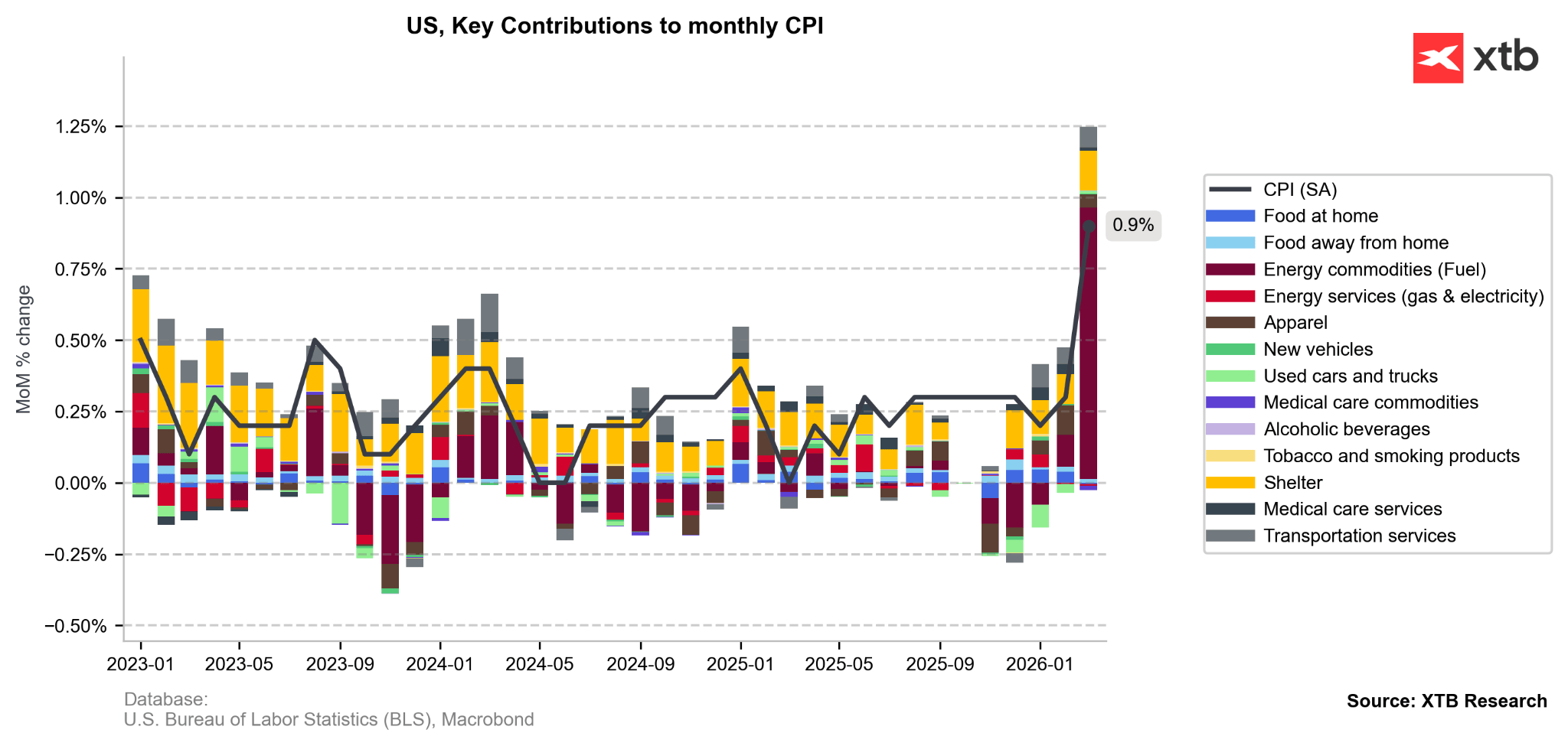

Last month, most of the increase in the index on a monthly basis was driven by airfares, which rose sharply due to significantly higher fuel prices – these account for 20–30% of operating costs and over half of variable costs. Memory cards and CPUs should also be on the agenda, as their production costs have risen significantly due to the ongoing conflict between the US and Iran. Furthermore, due to methodological adjustments, we should see a notable increase in rental costs, which have been consistently underestimated in recent months due to disruptions resulting from the longest government shutdown in history. A modest rise in core inflation (around 0.3% MoM) is therefore already priced in by the markets and should not cause any major concern.

Figure 3: Key contributions to MoM US CPI Inflation change (2023 - 2026)

Source: XTB Research, 12/05/2026

Source: XTB Research, 12/05/2026

The dollar is strengthening ahead of the release – though it is difficult to attribute this to the speculation surrounding April’s inflation figures. The US currency is supported by a risk-off sentiment stemming from the deadlock in negotiations between the US and Iran. We are seeing a renewed rise in energy commodity prices and hawkish repricing of interest rates in the major economies. This environment favours safe-haven currencies and the currencies of net energy exporters – with the dollar falling into both of these categories.

Figure 4: EUR/USD (04/05 - 12/05)

Source: xStation, 12/05/2026

Source: xStation, 12/05/2026

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.