Friday’s EURUSD session is driven by expectations for further signals regarding the future path of monetary policy on both sides of the Atlantic. Markets are closely monitoring today’s final inflation reading from the euro area, as well as recent comments from Federal Reserve officials, who are attempting to limit expectations of an early start to the rate-cutting cycle.

The current situation in the major currency pair is particularly interesting because lower inflation no longer automatically translates into a weaker dollar. Recent US data showed a more significant-than-expected cooling in price pressures, but the Fed is increasingly signaling that it does not intend to declare victory over inflation prematurely.

On the other side of the market, the euro continues to receive support from expectations that the European Central Bank will still need to remain cautious. Inflation in the euro area remains above the ECB’s target, while the risk of renewed energy price increases linked to geopolitical tensions further complicates the outlook for monetary policy.

EURUSD is therefore currently caught between two opposing narratives, with markets trying to determine whether the Fed will shift its stance more quickly or whether the ECB will be forced to maintain a restrictive policy stance for longer.

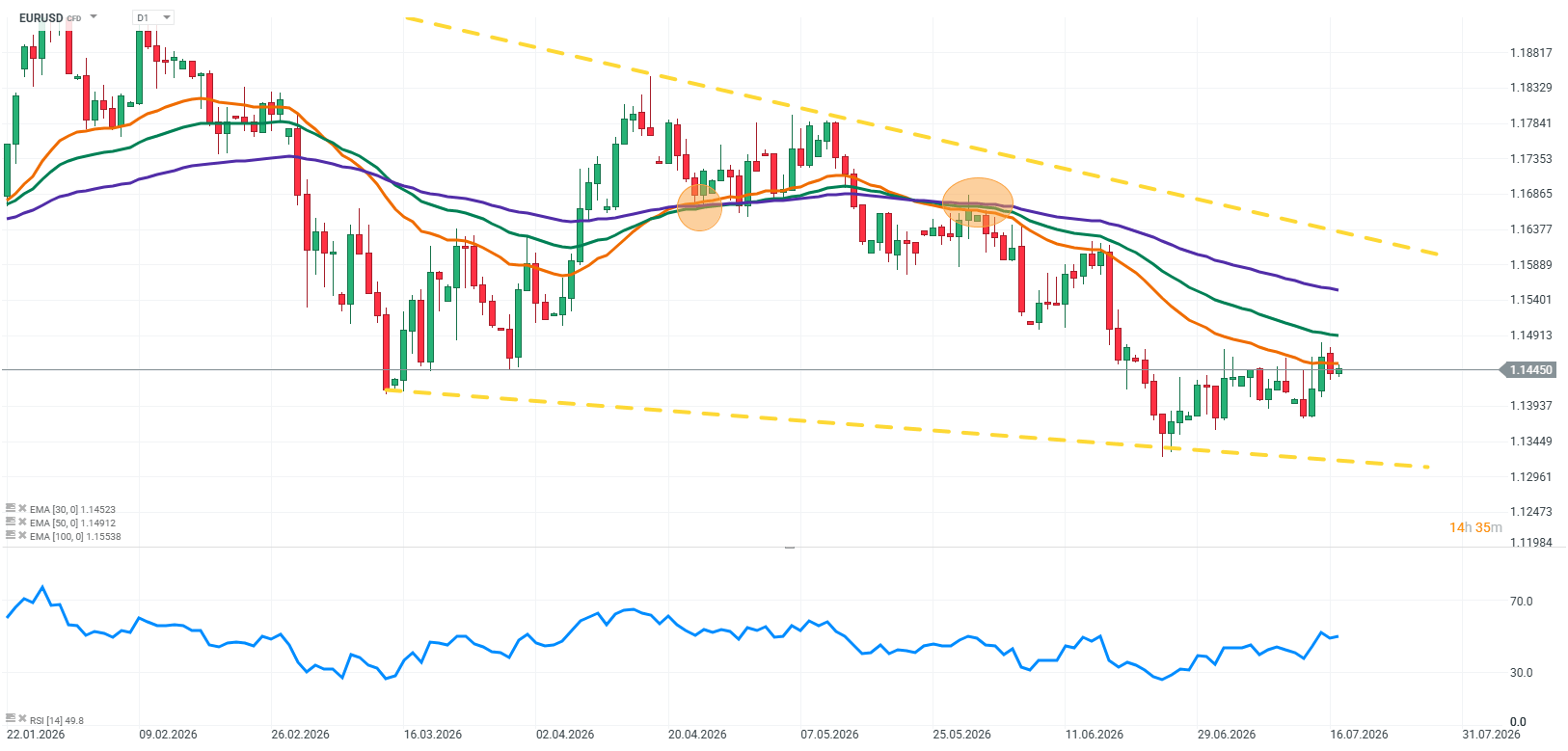

Source: xStation5

Factors currently shaping EURUSD

1. Eurozone inflation: markets await a signal for the ECB

The key event on the European side remains today’s release of the final HICP inflation reading for the euro area. Markets are no longer focused solely on the inflation figure itself, but rather on what the data could mean for the future policy path of the European Central Bank.

Inflation in the euro area has declined from its previous peaks, but this does not mean the ECB’s problem has been fully resolved. Price pressures remain above the central bank’s target, while investors continue to closely monitor the resilience of core inflation and services inflation.

The key question is not only whether inflation is falling, but whether the pace of disinflation will be sufficient for the ECB to begin easing monetary policy. If today’s release shows that price pressures remain more persistent than expected, markets may reduce expectations for future rate cuts, which could provide support for the euro.

On the other hand, clearer signs of further inflation moderation could increase pressure on the single currency, as investors would begin pricing in greater room for future monetary easing by the ECB.

Another important factor remains the energy market. If tensions in the Middle East lead to further increases in oil prices, inflationary pressures in Europe could rise again, limiting the central bank’s ability to adjust policy.

2. Fed attempts to regain control over the rate-cut narrative

The most important factor for the dollar remains the communication coming from the Federal Reserve. Recent US inflation data was significantly weaker than expected, initially strengthening market expectations that the Fed could begin cutting interest rates sooner.

Lower inflation should naturally provide the central bank with more room to ease policy. However, the Fed appears determined to prevent markets from moving too quickly toward a dovish interpretation.

Kevin Warsh has emphasized that the Federal Reserve cannot accept a situation in which inflation remains persistently above target. His comments suggest that some policymakers continue to worry about easing policy too early. Even stronger signals came from Dallas Fed President Lorie Logan, who argued that current interest rates may not be sufficiently restrictive and that further increases could still be justified.

This does not necessarily mean that the Fed will actually deliver another rate hike. The more important message for markets is that the central bank is in no rush to cut rates.

This is currently the key mechanism supporting the dollar. Several months ago, weaker inflation almost automatically translated into pressure on the USD. Today, markets are focusing much more on the Fed’s reaction function.

If investors conclude that inflation is declining but the Fed intends to keep rates elevated for longer, the dollar could remain supported.

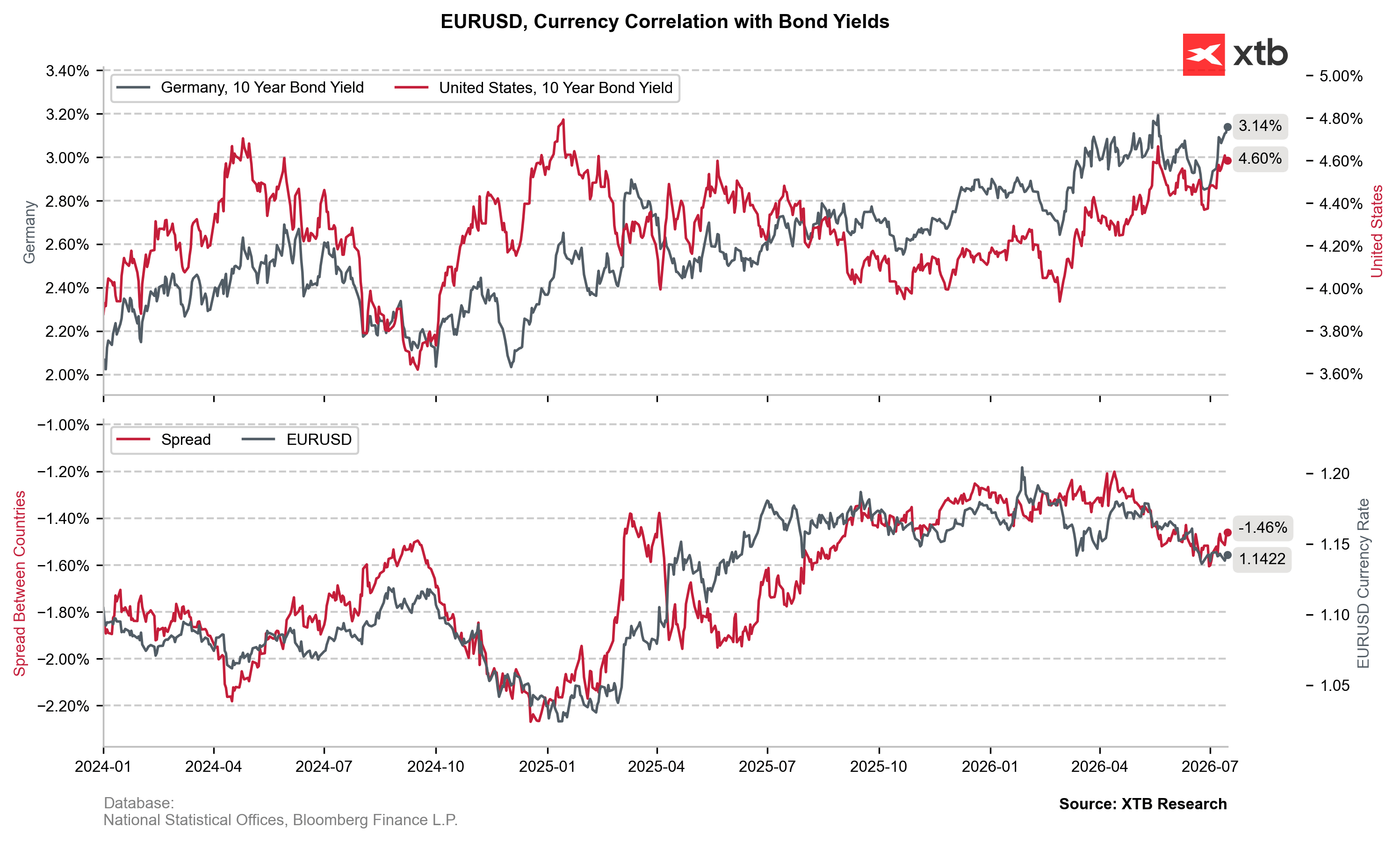

3. The key hidden factor: real interest rates and US bond yields

One element that often remains in the background of EURUSD discussions is real interest rates and the bond market. For the dollar, it is not only the level of inflation that matters, but rather the relationship between inflation trends and expectations regarding Fed policy.

If inflation in the US continues to decline, but the Federal Reserve remains cautious and delays rate cuts, real interest rates could remain attractive for investors.

Such a scenario would mean lower inflation, but also relatively high bond yields and limited expectations for rapid monetary easing. This is precisely why recent weaker inflation data has not triggered a sustained decline in the dollar.

Markets are increasingly recognizing that improving inflation data alone may not be enough to weaken the USD if the Fed maintains a cautious approach and keeps policy restrictive for an extended period.

4. Persian Gulf tensions and oil: the return of inflation risks

The final factor influencing EURUSD remains the geopolitical environment. Rising tensions in the Persian Gulf have once again increased the importance of the oil market and the risk of supply disruptions.

Higher energy prices can affect currencies through two main channels. The first is inflation. More expensive oil could slow further declines in consumer prices and reduce the room available for central banks to cut interest rates.

The second channel is risk aversion. During periods of heightened uncertainty, investors often move capital toward the US dollar as the world’s primary safe-haven currency.

For EURUSD, this creates an additional complication. Higher oil prices could simultaneously increase expectations for more restrictive policies from both the ECB and the Fed, while also supporting the dollar through stronger demand for defensive assets.

EURUSD: markets await the answer to who can maintain restrictive policy for longer

The current situation in the major currency pair reflects a clash between several competing narratives. The Fed is trying to convince markets that lower inflation does not automatically mean the immediate start of a rate-cutting cycle.

The ECB is observing a moderation in price pressures, but still has to deal with inflation above target and the risk of renewed energy price increases. Geopolitical uncertainty further strengthens the role of the dollar as a safe-haven asset.

The most important reaction channel remains bond yields and expectations regarding the future path of interest rates.

If markets conclude that the Fed will maintain a restrictive stance for longer than previously expected, the dollar could remain supported even as inflation continues to decline. Conversely, stronger confidence that the US disinflation process is sustainable and will allow the Fed to begin easing policy could once again increase pressure on the greenback.

Key takeaways

- Today’s final euro area inflation reading will be an important signal for expectations regarding the ECB’s future policy path.

- Inflation in Europe is declining, but it remains a challenge for the central bank, particularly due to persistent price pressures in the services sector.

- Recent weaker US inflation data has increased expectations for Fed rate cuts, but policymakers are attempting to prevent markets from pricing in an overly rapid easing cycle.

- Kevin Warsh and other Fed officials continue to emphasize that the fight against inflation is not yet complete.

- Real interest rates and bond yields remain among the most important drivers for the dollar.

- Developments in the Persian Gulf could once again increase inflationary pressure through energy markets while also supporting the dollar through higher risk aversion.

- EURUSD therefore remains at a point where the key question is not only which economy is performing better, but which central bank will have stronger reasons to maintain restrictive monetary policy for longer.

Wheat extends correction, falls to its lowest level since July 10 🚩 Drought, El Niño and the Black Sea in focus

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.