The central bank approaches today's decision in a clear "wait-and-see" mode, having engaged in a distinct rate-cutting cycle since June 2024. The ECB has lowered interest rates eight times, likely concluding this cycle or pausing to assess various factors before any potential further reductions later this year. Key concerns for European monetary policymakers at this juncture include the ongoing trade war, the future trajectory of inflation amid uncertainties surrounding economic recovery, and the situation in the oil and gas markets. The decision will be announced at 01:15 PM BST and the conference after the decision with the Christine Lagarde will be held 30 minutes later.

Macroeconomic and Geopolitical Backdrop to the Meeting:

-

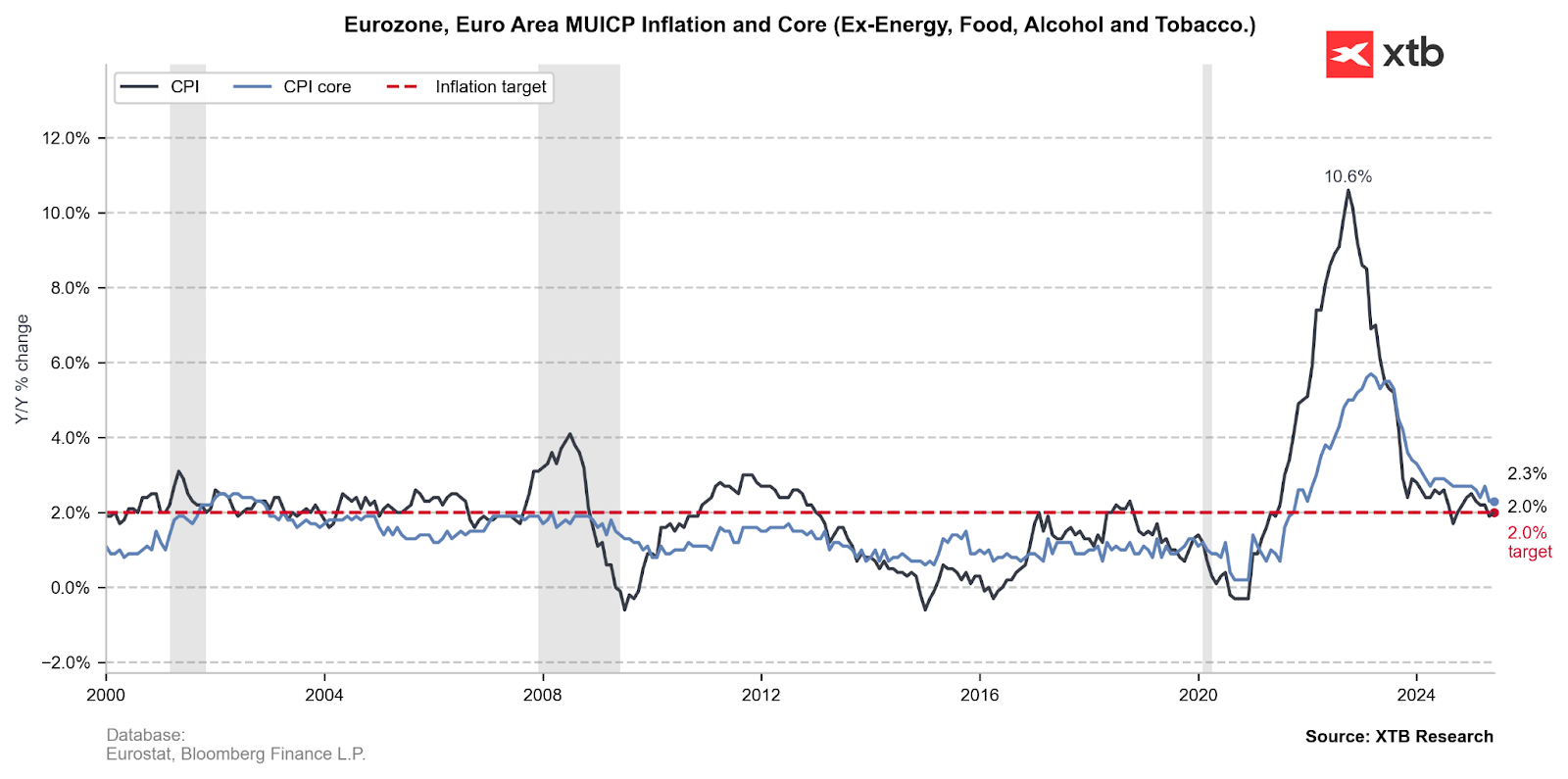

CPI inflation has stabilized at 2.0% year-on-year (y/y), while core inflation remains elevated at 2.3% y/y, although this is its lowest level since January 2022.

-

Energy deflation is accelerating. The energy sub-index of CPI inflation registered -2.7% y/y in the latest June reading, while services inflation remains distinctly elevated at 3.3% y/y.

-

Wage growth has decelerated for the second consecutive quarter, indicating further potential for core inflation to decline. Simultaneously, ECB surveys suggest that sticky services prices may be masking a weakening of overall cost pressures.

-

High tariffs on the European Union could prompt the ECB to implement further rate cuts, particularly if extremely high tariff rates are imposed on pharmaceutical products.

-

Bloomberg's SHOK model indicates that a 25% tariff on pharmaceutical products could lead to a 0.3 percentage point reduction in euro area GDP. It is worth noting that President Donald Trump has threatened tariffs as high as 200% in the longer term.

-

Currently, the baseline scenario still assumes an increase in tariffs on European products to 30% from the current 10%. On the other hand, a 15% rate is also being discussed. European producers' hopes are tied to an agreement between the US and Japan, which stands at precisely 15%.

Inflation has stabilised at 2.0%, but the risk of deflation has emerged, especially if we were to face a greater risk of trade war. Only strong reciprocal actions from the EU could impact inflation upwards. Source: Bloomberg Finance LP, XTB

ECB to Maintain Neutral Stance, but Cuts May Still Emerge

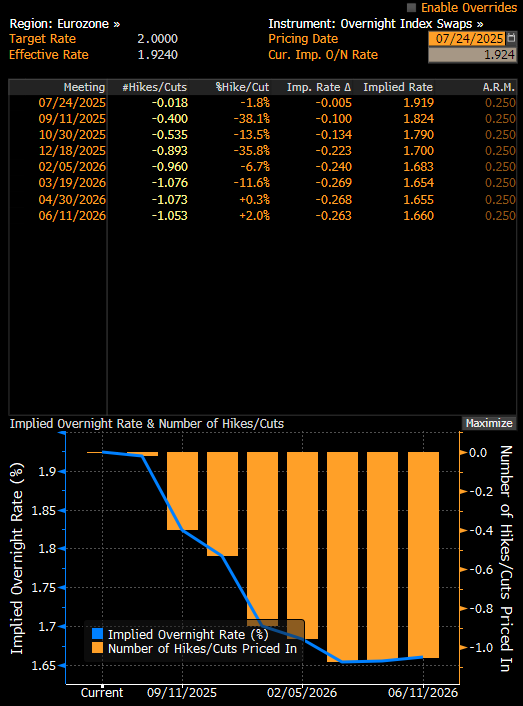

The latest communication from Christine Lagarde clearly indicated that interest rate cuts in the euro area have likely concluded. Conversely, ECB's de Guindos and Lane have stated that the bank's priority is to prevent the entrenchment of deflation, which could hint at a possible return to cuts. However, the market currently does not price in high odds of a September cut, but it does allow for the possibility of cuts towards the end of the year.

Probabilities for further interest rate cuts in the euro area. As can be seen, less than one full cut is priced in for the end of this year. Source: Bloomberg Finance LP, XTB

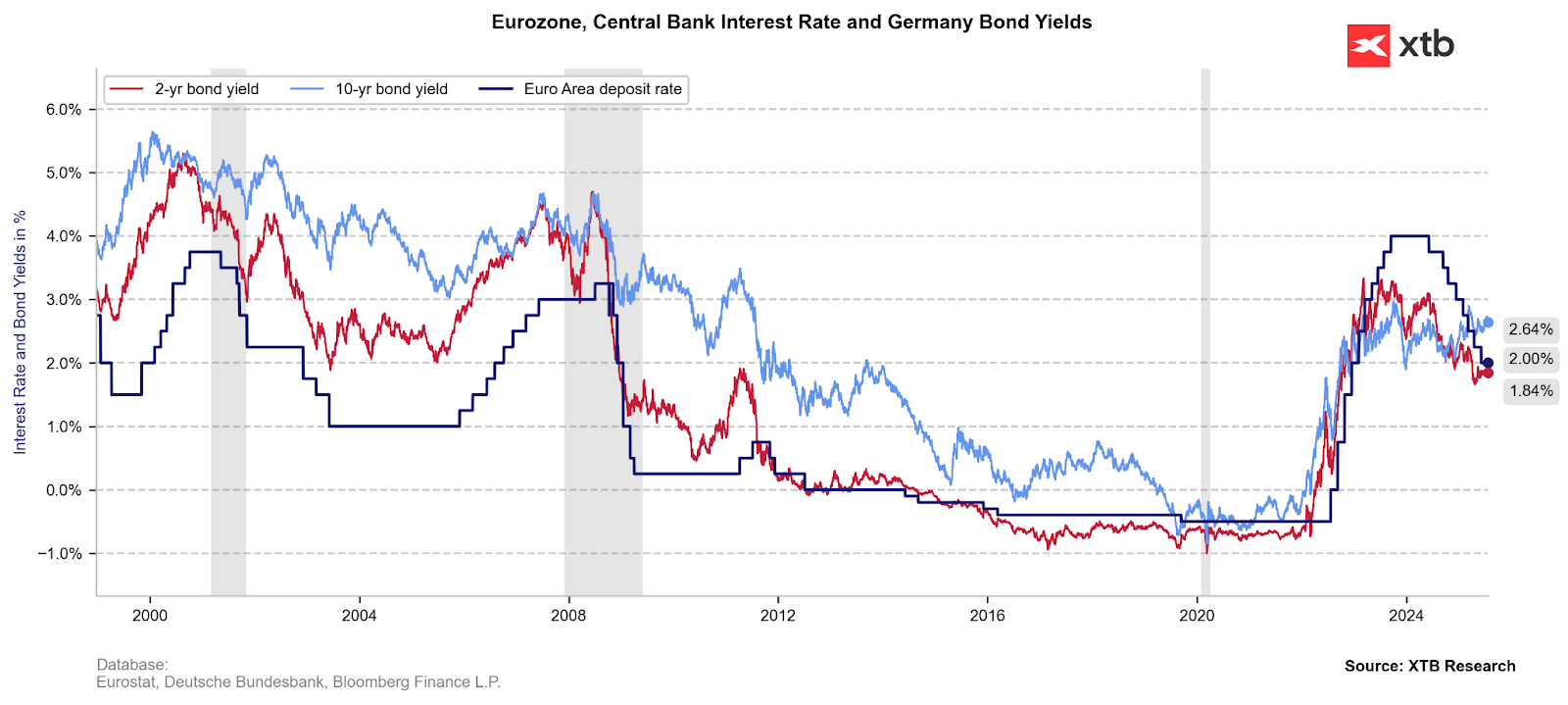

A premium has emerged on 10-year yields relative to the current interest rate level, which appears to be a normal situation. However, it is worth noting that in the past, the spread between yields and the deposit facility rate was wider, implying that cuts from the current level are still possible. Source: Bloomberg Finance LP, XTB

What's Next for EURUSD?

Should there be any signal of potential rate cuts today, the euro could come under pressure. Furthermore, a more intensified trade war, meaning tariffs above 20%, could lead to deflation and push the ECB towards faster and larger cuts. Nevertheless, a trade agreement between the US and the EU that results in limited tariffs could lead to further stabilisation in EURUSD or even drive it higher towards the 1.20 level, considering the relatively strong positive sentiment of speculators towards the euro.

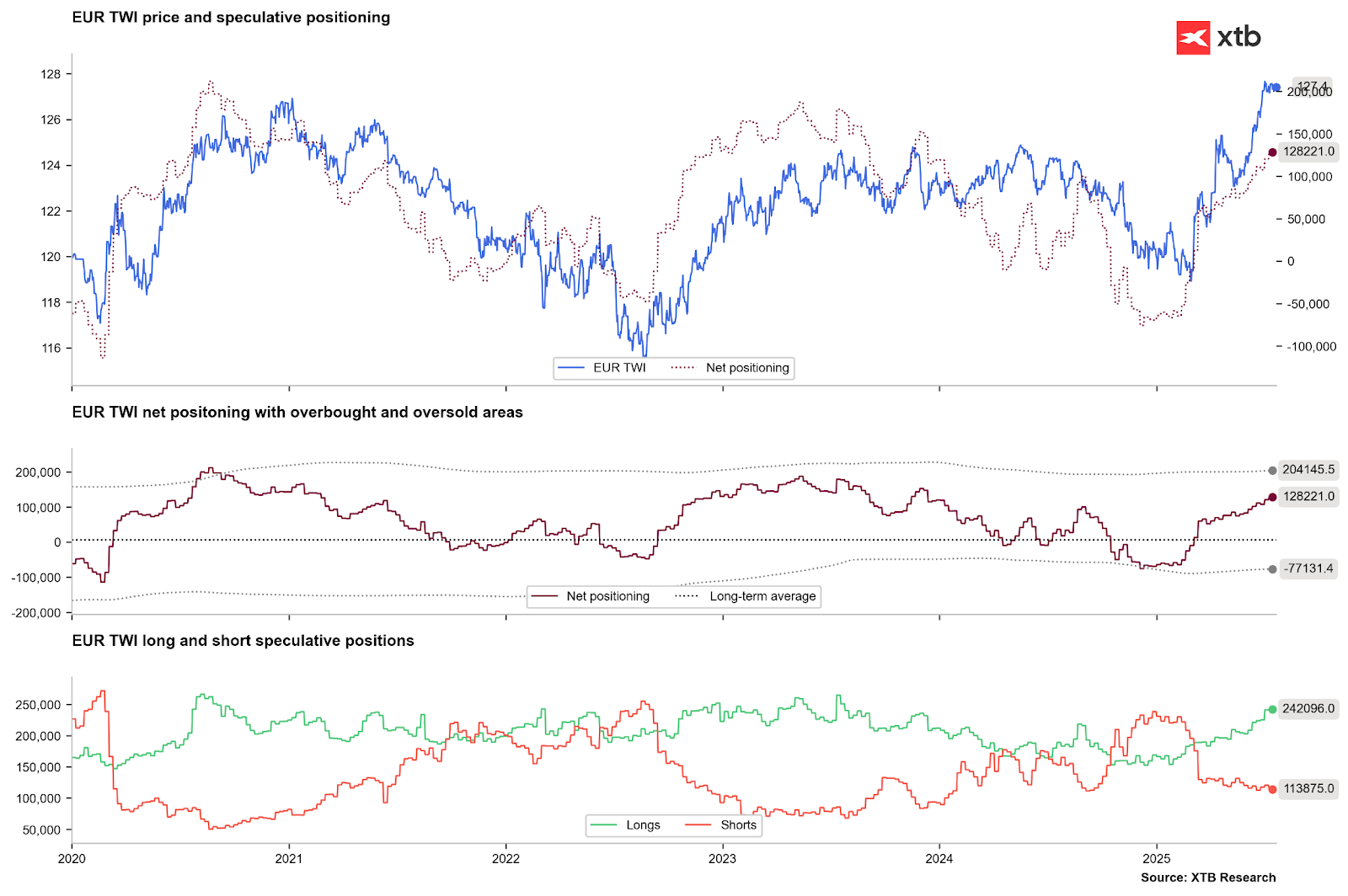

Speculators are the most optimistic about the euro since 2023. However, the EUR TWI (Trade Weighted Index) is already significantly higher than in the last 5 years. Source: Bloomberg Finance LP, XTB

EURUSD is losing ground today ahead of the ECB decision but remains very close to recent local peaks. However, if dovish signals emerge from today's decision, a decline towards the potential neckline of a Head and Shoulders formation, around the 1.16 level, could be possible. The potential target of such a formation is around 1.1250. Nevertheless, an attempt to breach the recent local highs from early July cannot be ruled out today, which would potentially open the path towards 1.20.

Morning Wrap: Oil Rises Again (07.08.2026)

Wheat extends correction, falls to its lowest level since July 10 🚩 Drought, El Niño and the Black Sea in focus

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.