Today's U.S. consumer price inflation (CPI) report, which will be released at 1:30 PM BST, will be the most important macro reading of the week, shedding more light on whether the really very solid U.S. data seen recently will translate into a higher inflation reading and put more pressure on easing 'dovish' communication from the Fed. Wall Street is trading near historic highs ahead of the report, and bulls were not spooked by a strengthening dollar and 10-year yields, which rose to 4.09%, bouncing nearly 46 bps from September lows.

A report far above forecasts could seriously strengthen the dollar and lead to another wave of rising yields, entitling at most one rate cut this year. In contrast, a CPI below, or in line with, forecasts could reassure the market that the Fed will not be forced to change its communications (at least at this stage), and that price pressures in the economy are subsiding. Will the Fed be forced to back off from its announcement of an 'aggressive cycle' of cuts?

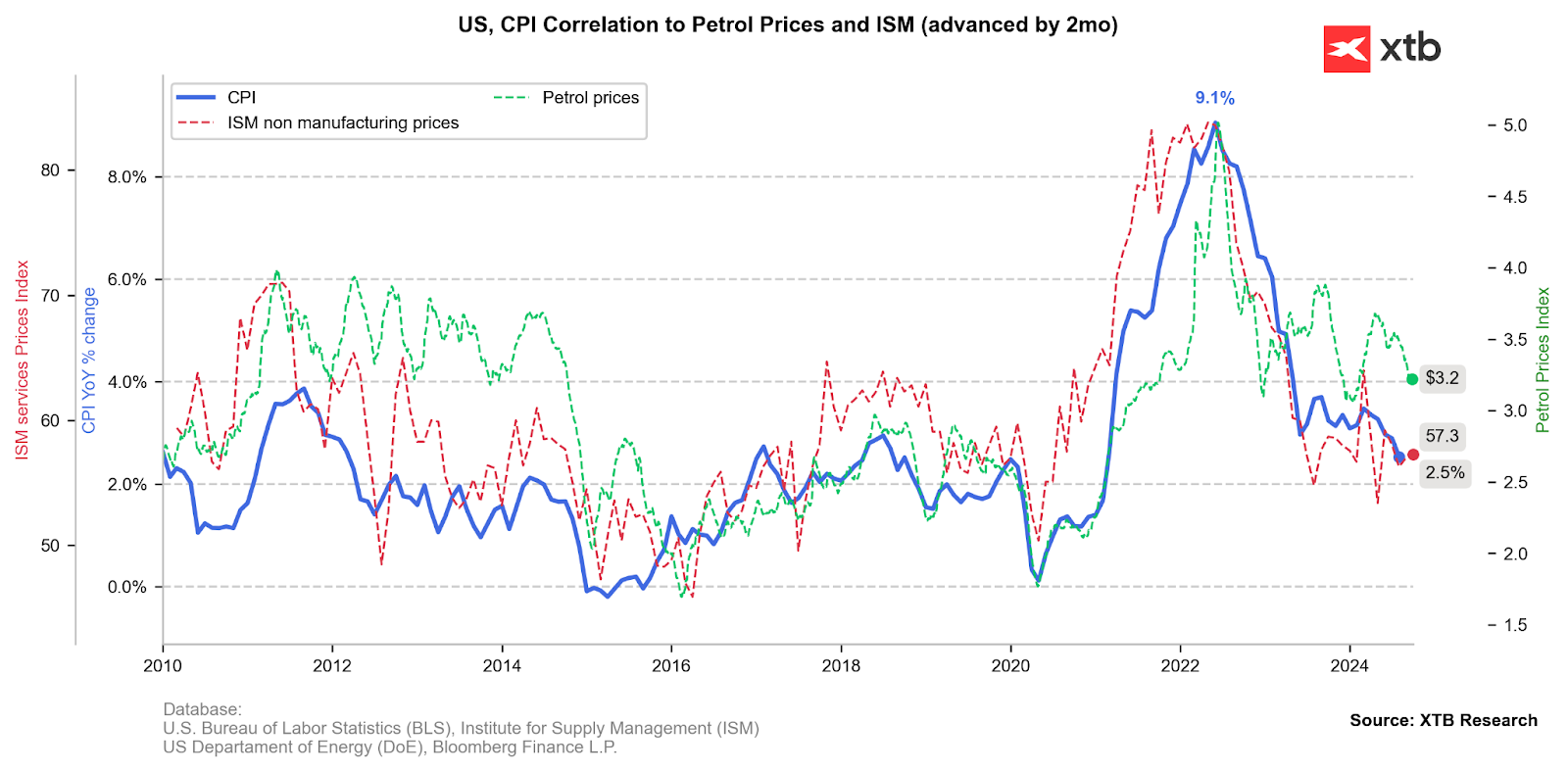

What to expect from today's report?

- CPI inflation is expected to fall to 2.3% y/y from the previous level of 2.5% y/y. Lower energy costs are expected to be primarily responsible for the decline

- On a monthly basis, the reading is expected to be 0.1% m/m, against a previous increase of 0.2% m/m

- Core inflation, which is more crucial from the Fed's perspective, is expected to remain at 3.2% y/y, in line with the previous reading

- On a monthly basis, growth is expected to be 0.2% m/m, slightly lower than the previous reading of 0.3% m/m. Growth of 0.2% m/m is consistent with reaching the inflation target within the forecast timeframe

- It is worth noting that the decline in car prices has clearly slowed recently, so the impact of their prices is likely to be marginal. In recent readings, car and parts prices have had a significant impact on curbing inflation

- Rental inflation and increased hotel prices will continue to be one of the main drivers for inflation

- Higher wages are also one factor that points to core inflation remaining high

Fuel prices have fallen noticeably, which is likely to lead to lower inflation. The price sub-index from the service sector remained relatively unchanged in recent readings. Source: Bloomberg Finance LP, XTB

The decline in car prices has clearly slowed. Although disinflation on an annual basis is evident, a monthly increase in prices is not out of the question. This points to continued pressure on underlying prices. Source: Bloomberg Finance LP, XTB

Rent inflation has rebounded recently, although the 18-month advance indicator in the form of Case Shiller prices indicated that rent inflation should continue to decline for several more months. Rent inflation is one of the main factors for overall and core inflation. Source: Bloomberg Finance LP, XTB

Why is inflation important to the Fed?

Recent statements by Fed members suggest that despite the recent rise in oil prices and strong labor market data, the consensus at the Federal Reserve is that price pressures are nonetheless under control and still on track for the 2% target.

- On the other hand, yesterday's minutes showed that the decision to cut 50 bps in September was not obvious, making a potentially higher-than-forecast report likely in the markets' view to almost rule out the prospect of cuts of more than 25 bps this year.

- Still stronger data from the labor market, wages, or GDP are not a 'guarantor' of higher inflation, as consumers' preferred capital allocation may have changed (rebuilding of still relatively low household savings, following the inflation wave)

EURUSD (D1 interval)

The pair weakened and fell below the key long-term support at the EMA200 level, near 1.095. On the other hand, however, the RSI shows a record oversold level, and in recent quarters the Eurodollar has repeatedly slipped below the 200-session exponential average, in response to market indecision. However, the double-peak formation looks worrying about the pair, especially in the context of recent weak publications from the eurozone.

Source: xStation5

Economic calendar: Strong reading from the UK labour market, German ZEW in focus

Morning wrap: Indices Look for a Rebound Amid the U.S.-Iran Conflict (21.07.2026)

Daily Summary: China Shows Its Teeth on AI; The U.K. Sees a Government Revolution 🏛️

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.