Today marks the most important event related to the ECB economic symposium in Sintra, Portugal. Today, a panel discussion featured the new Fed chief, who has recently become known for his more hawkish side, although he remains a significant puzzle for the markets. His remarks today, coupled with slightly weaker US data, are not only weakening the dollar but also restoring hope for investors in the gold market, which is not only breaking back above $4,000 but even testing the $4,100 per ounce level.

Key takeaways from Kevin Warsh's speech

- The death of "forward guidance": Warsh definitively breaks with the tradition of his predecessors. The Fed will not provide the market with clear signals regarding future interest rate moves. Investors must look at hard data. Warsh strongly supported ECB chief Christine Lagarde on this issue.

- Uncompromising fight against inflation: Warsh stated bluntly: “We want to achieve price stability.” He added that if anyone thought the Fed would accept inflation above 2%, they would be disappointed. He still considers prices too high. This issue, however, remains quite hawkish.

- Slight optimism and decline in inflation expectations: The Fed chief noted that during the first four weeks of his tenure, inflation expectations and risks associated with inflation have fallen. He also emphasized that bond yields and market volatility have moved lower. This gives hope to investors in the gold market.

- "Family fight" in July: He announced that at the next FOMC meeting (in 4 weeks), there will be a sharp discussion. He refused to speculate whether the current spike in inflation caused by the conflict with Iran is transitory.

- Fed Balance Sheet Reduction (QT): He confirmed his well-known hawkish stance, wanting the Fed's balance sheet to be smaller because, in his view, a balance sheet that is too large "borders on fiscal policy" and works mainly by inflating asset prices. However, changes will be introduced carefully and transparently. This, in turn, is slightly negative news for the indices.

- Fed Independence Untouched: He assured that despite recent Supreme Court rulings (including after the Cook case), the Fed will remain fully independent and will strictly adhere to its mandate.

- Technological optimism (AI): He considers the US to be the main beneficiary of the AI revolution. While the tech boom boosts inflation in the short term (demand for components), in the long term, higher productivity could change the rules of the game for monetary policy.

Is Warsh Toning Down Sentiment?

One could state in a typically analytical way: both yes and no. Warsh plays the role of an "objective judge," which the markets receive with relief. After his first June meeting, Wall Street feared Warsh would be an extreme hawk, ready to sharply raise rates in response to the conflict with Iran. In Sintra, Warsh did not toughen his rhetoric. Although he reiterates that the goal is 2% inflation, he simultaneously sent several reassuring signals to the markets:

- He admitted that inflation pressure and expectations have slightly fallen over the last month.

- He noted falling bond yields with satisfaction.

- By moving away from forward guidance, he removed market fear that the Fed would announce a series of rate hikes "in advance."

This means markets no longer feel the immediate threat of an instant hawkish strike, which, combined with the latest macro data, gave an impulse for a weaker dollar and a rise in risk-on assets.

EURUSD returns to 1.14, and gold explodes to $4,100?

Parallel to Warsh's speech, key data from US manufacturing (ISM Manufacturing) hit the market, which perfectly explains these major moves:

- Weaker ISM and a collapse in prices: The headline ISM manufacturing index fell to 53.3 (forecast 53.9), and new orders also came in weaker. Most importantly, the ISM Prices Paid index saw a massive drop to 73 (previously as high as 82.1, forecast 77.5).

- EURUSD Reaction (move to 1.14): Since the US price sub-index is falling sharply, and Warsh himself says inflation risks are diminishing, investors conclude that the Fed won't need to panic-hike rates. US bond yields are falling, which automatically hits the dollar (USD) and drives the EURUSD exchange rate up.

- Spectacular return of gold to $4,100: Gold received an ideal fuel cocktail today:

- Geopolitics: The ongoing conflict with Iran and uncertainty (Vance's and White House comments mentioned in dispatches about chances for a deal, but with risk still looming) maintain demand for "safe havens."

- Weaker dollar and lower yields: Since the ISM data cools Fed's hawkish ambitions and Warsh is not threatening hikes, the opportunity cost of holding gold falls.

- Lack of forward guidance: Since the Fed is giving up on guiding the market by the hand, uncertainty about the future increases – and gold loves uncertainty. The return to the $4,100 area is a technical and fundamental display of strength for this metal in the era of the new Fed chief.

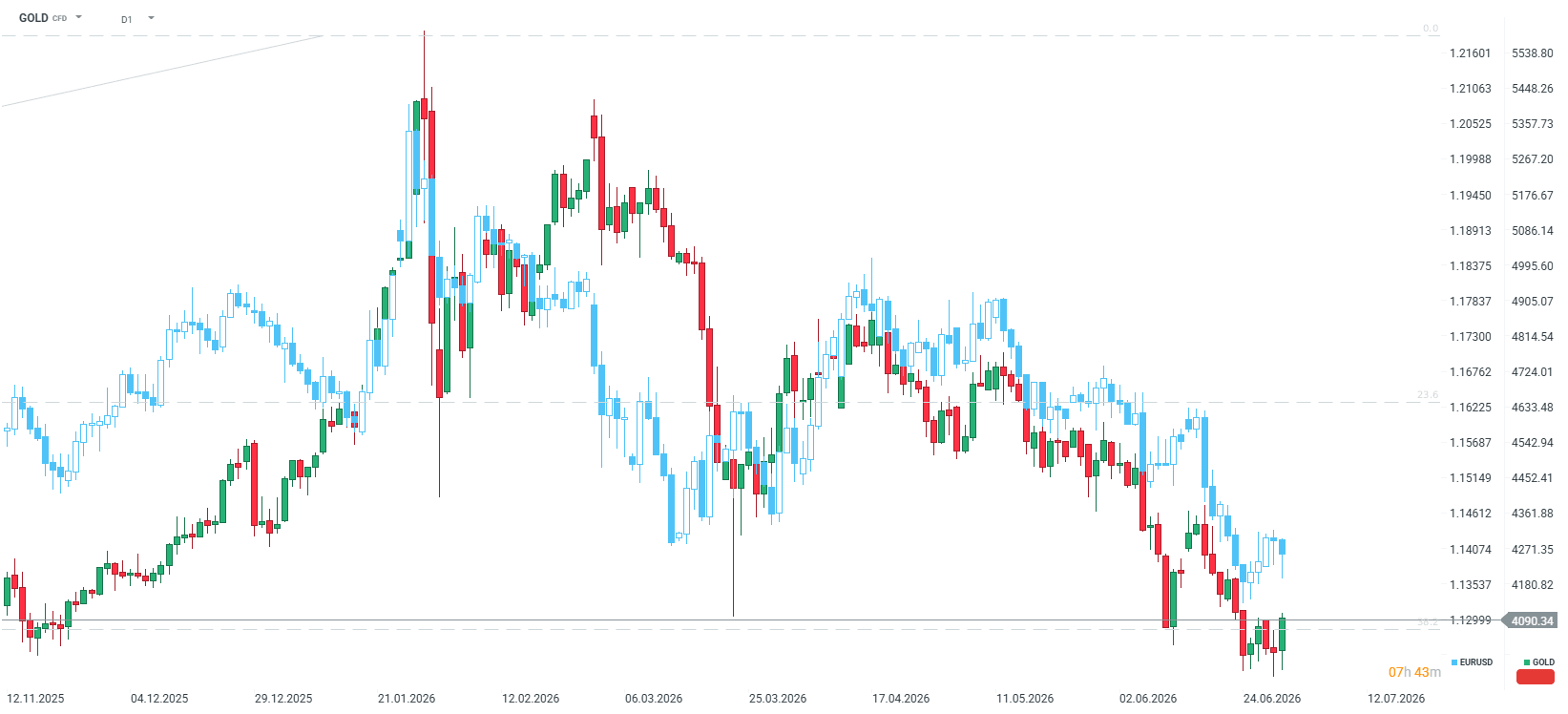

Gold started today's session with a drop below $4,000, but for several days we have observed that this is becoming increasingly strong support. Today, gold returns above the 38.2 retracement. It is worth noting that in November 2025, the $4,000 level was tested several times. If expectations for hikes are indeed decreasing (there is still a pricing of more than 1 hike by the end of this year), gold has a chance for a rebound. EURUSD is also rebounding but remains below the 1.14 level. Source: xStation5

Gold started today's session with a drop below $4,000, but for several days we have observed that this is becoming increasingly strong support. Today, gold returns above the 38.2 retracement. It is worth noting that in November 2025, the $4,000 level was tested several times. If expectations for hikes are indeed decreasing (there is still a pricing of more than 1 hike by the end of this year), gold has a chance for a rebound. EURUSD is also rebounding but remains below the 1.14 level. Source: xStation5

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.